$10.1 Billion In 90 Days. The Greeks Are Cornering The Tanker Market Before Posidonia Even Opens.

Greek Shipowners Placed 102 Vessel Orders In Q1 2026, 63 Of Them Tankers. The Largest Single Quarter In Greek Shipping History. Posidonia Opens June 1.

⚓ The Gosships Team

Gosships Intelligence Is Published At Gosships.com

For Sponsorship And Partnership Inquiries Contact intelligence@gosships.com

|⚓ About Us | 🛢️ Deep Water Reports | 📋 SwiftAction Training |

🏅 Founding Black Gold Membership (*53 Slots Left)

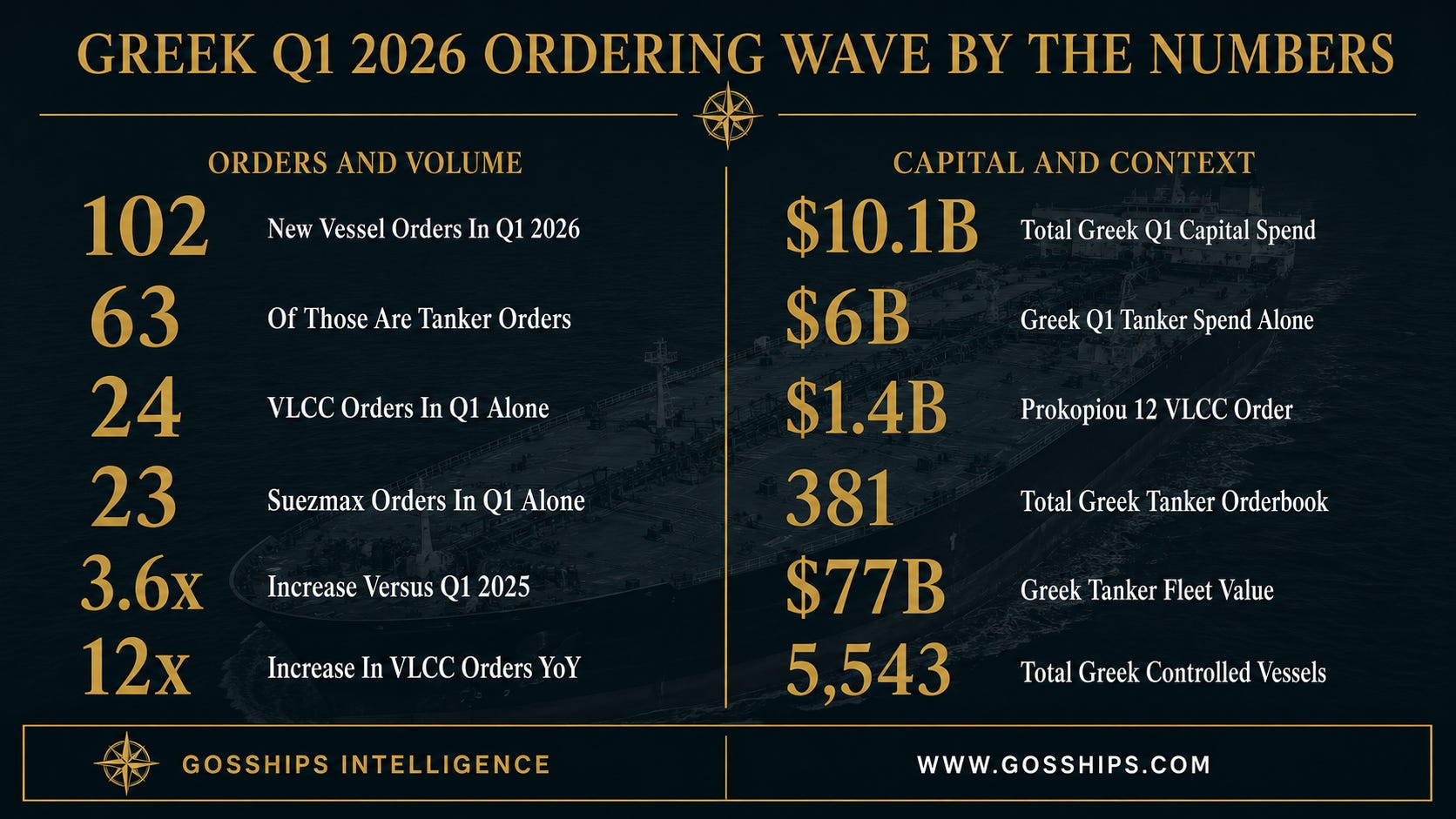

Greek shipowners just did something that has not happened in the history of the data. In the first 90 days of 2026, while the world’s attention was locked on the Iran war and the closed Strait of Hormuz, Greek principals placed 102 newbuilding orders worth approximately $10.1 billion at Asian shipyards, per Xclusiv Shipbrokers data published in early May. That is a 3.6 times increase in volume versus the 28 vessels Greeks ordered in Q1 2025, and the most capital-intensive quarter on record in the Xclusiv dataset. Tankers were 63 of those 102 orders, worth approximately $6 billion. Inside that tanker number, 24 were VLCC or ULCC class and 23 were Suezmax, meaning 75% of Greek tanker spend in Q1 went into the two largest crude classes per Xclusiv and Hellenic Shipping News. The total Greek tanker orderbook has now surged to 381 vessels at end-Q1 2026, up from 286 a year earlier.

By Gosships analysis, this is not a fleet renewal. This is a positioning trade. Greek principals have looked at the same set of facts the rest of the market is looking at, the closed strait, the sanctions fragmentation, the Russian shadow fleet sideline, the IMO Net-Zero Framework postponement, the tightening yard slots out to 2029, and they have placed the largest single-quarter bet in the history of Greek shipping that the structure of the post-2026 crude tanker market is going to look very different from what is priced in today. Posidonia 2026 opens at the Athens Metropolitan Expo Center on Monday June 1. The world’s top shipyards are flying in to present to the same Greek principals who already spent $10.1 billion 90 days before the show.

📋 In this issue:

🛢️ The Story

📊 By The Numbers

🔍 Why It Matters

👀 What to Watch

🚨 Gosships Signal

📊 Get The Deep Water Report

→ Global Tanker Market Outlook Q2 2026

📋 Competency-Based Maritime Training

→ SwiftAction

📌 Gosships Data Card

→ Total Greek Q1 2026 Newbuild Orders: 102 Vessels Worth $10.1 Billion Per Xclusiv Shipbrokers

→ Greek Q1 Tanker Orders Alone: 63 Vessels Worth $6 Billion Per Xclusiv

→ Greek Q1 VLCC + Suezmax Orders: 24 VLCC + 23 Suezmax = 75% Of Tanker Spend

→ Year Over Year Volume Increase: 3.6 Times Versus Q1 2025 (102 Vs 28) Per Xclusiv

→ Greek Q1 VLCC Orders: 24 In Q1 2026 Versus 2 In Q1 2025 Per Xclusiv

→ Greek Share Of Global Q1 Suezmax Orders: 23 Out Of 41 Per Xclusiv Via GreekReporter

→ Greek Tanker Orderbook End Q1 2026: 381 Vessels (Up From 286 Year Earlier) Per Xclusiv

→ Total Greek-Controlled Fleet: 5,543 Vessels Per Posidonia / UGS

→ Greek Share Of Global Tonnage: 21% Per UGS

→ Greek Tanker Fleet Value: $77 Billion (Most Valuable Globally) Per VesselsValue

→ Global Q1 Orderbook: 191 Million CGT, 17 Year High Per BIMCO

→ Global Q1 Total Newbuilding Orders: 422 Vessels Per Xclusiv

→ 2025 Greek Activity: 250 Newbuild Orders Plus 260 Second Hand Deals Per Cass Technava

→ Posidonia 2026 Dates: June 1-5 At Athens Metropolitan Expo

→ Expected Posidonia Attendance: 40,000+ Professionals From 140 Countries

🛢️ The Story

The Greeks have always been the most patient capital in shipping. They tend to buy when others are selling and order when others are deferring. What just happened in Q1 2026 broke that pattern in a way the data has not seen before.

Per Xclusiv Shipbrokers data published in their early May weekly report and republished by Hellenic Shipping News, Cyprus Mail, GreekReporter, Newmoney, and The Sea Nation, Greek principals placed 102 newbuilding orders in Q1 2026 across all four sectors at a combined value of approximately $10.1 billion. That is a 3.6 times increase from the 28 vessels Greeks ordered in Q1 2025. Xclusiv described it as “the most capital-intensive quarter on record in this dataset” and “a strategic repositioning by Greek principals at a pace and scale not seen in recent cycles.”

The tanker sector did most of the heavy lifting. Greeks placed 63 tanker newbuild orders in Q1 2026 worth approximately $6 billion, more than double the previous peak of 48 tankers in Q2 2024 per Xclusiv. The concentration at the large end of the size spectrum is what makes the number consequential. Of those 63 tankers, 24 were VLCC or ULCC class and 23 were Suezmax. Together that is 47 large crude carriers, or 75% of all Greek tanker orders, worth a combined value exceeding $5.1 billion per Xclusiv via Hellenic Shipping News. Xclusiv concluded its weekly report with the strongest editorial line on the data: “Taken together, Q1 2026 marks a decisive inflection point: the capital deployed by Greek owners is unprecedented in scale, overwhelmingly directed at large vessels.”

For context on how unusual that scale is, in Q1 2025 Greek owners placed just 2 VLCC orders and 9 Suezmax orders in total. The jump from 2 VLCCs to 24 is a 12 times increase in a single year. At the global level, total VLCC and ULCC orders rose to 64 in Q1 2026 from just 3 in Q1 2025 per Cyprus Mail citing Xclusiv. Greeks placed 24 of the 64. Greeks also secured 23 out of 41 total global Suezmax orders, effectively dominating the segment per GreekReporter citing Xclusiv.

The total Greek tanker orderbook has surged to 381 vessels at end-Q1 2026, up from 310 in Q4 2025 and 286 one year earlier per Xclusiv. That trajectory is what tells the structural story. Greek principals are not running an opportunistic trade. They are reconfiguring the ownership base of the global large crude tanker fleet, and they are doing it before Posidonia 2026 opens.

The breadth of the Greek Q1 ordering wave extends beyond tankers. Per GreekReporter citing Xclusiv, Greek owners returned to large-scale dry bulk for the first time in years, placing 6 Capesize and 6 Newcastlemax orders in segments where they had no presence in 2025. Greek owners also placed 9 large LNG carrier orders to capitalize on the growing role of liquefied natural gas in the global energy mix. The Greek product tanker segment saw a notable return with 12 MR2 orders following zero MR2 activity in 2025. The strategic reach is total. Greeks bought into every major segment Q1 2026, but the tanker concentration is what tells the structural story.

Greek Q1 ordering activity is also visible at the macro level. Per Lloyd’s List, since the start of the year almost 200 tankers above 40,000 dwt have been ordered globally, with the crude tanker sector accounting for around 40% of all newbuilding activity. The Suezmax segment led the surge globally with 52 new ships, with Greeks placing 23 of them. The VLCC segment accounted for 41 new ships, with Greeks placing 24. In both segments, Greek principals are over half of the global ordering activity.

The named deals are public record. George Prokopiou is leading the market with an order for 12 VLCCs valued at approximately $1.4 billion, to be built in China and delivered from 2028, per Greek City Times. Athens-based Monte Nero Management, linked to shipowner Panagis Zissimatos, entered the VLCC segment with a 2-ship order at Hengli Heavy Industry at an estimated $119 million per unit, per Splash247. Byron Vassiliadis of Venergy Group is reportedly close to a deal for 4 Suezmax tankers worth more than $320 million, marking his expansion into the tanker market per Greek City Times. Navios placed an order for 4 VLCCs of 310,000 dwt at Wuhu Shipyard per Splash247. Laskaridis placed 2 VLCCs at Hengli Heavy Industries Dalian per Lloyd’s List. Capital Maritime & Trading placed 1 scrubber-fitted VLCC at Hengli, while Dynacom Tankers Management signed up for 4 VLCCs at the same builder per Lloyd’s List. Zodiac Maritime, headquartered in London but with deep Greek connections, placed a 3-ship Suezmax order at Samsung Heavy Industries with construction at the Petrovietnam-controlled PVSM shipyard per Lloyd’s List.

What makes these orders different from a normal tanker upcycle is the why. Per Xclusiv analyst Eirini Diamantara quoted by Lloyd’s List, the rebound is driven by fleet demographics, sanctions-fragmented effective fleet capacity, and tightening yard availability through 2028. “Out of the 689 active suezmaxes, some 20% are 20 years of age or more while within the VLCC segment 183 units, or around 20% of the fleet, fall into the same age category,” Diamantara said. She added that “nearly half of the suezmax and VLCC fleet aged 17 years or above is currently affected by US, UK or EU restrictions, substantially shrinking the pool of commercially tradeable ships.”

That is the structural setup. The headline global VLCC fleet looks adequate. The actual commercially tradeable fleet, the vessels that are not sanctioned, not too old to charter, not stuck in the Gulf, is significantly smaller. Per Diamantara via Lloyd’s List, “as a result of sanctions, the effective trading fleet is significantly smaller than headline figures suggest, compelling owners to secure newbuilding slots early to maintain fleet competitiveness and trading flexibility.”

The yard math reinforces the Greek bet. Per Lloyd’s List, the VLCC orderbook has now surpassed 140 ships, representing around 15% of the existing fleet. Only 7 VLCC deliveries are expected globally in 2025. That rises sharply to 40 deliveries in 2026 and peaks at 58 ships scheduled in 2027. The Suezmax orderbook now equates to over 20% of the current fleet by number of ships. Per BIMCO via Splash247, the global shipping orderbook hit a 17-year high in Q1 2026 at 191 million compensated gross tonnes, equivalent to 17% of the global fleet, the highest ratio since 2011. 57% of contracting so far in 2026 is expected to be delivered after 2028. Yard slots are tightening. Greeks are locking them.

The Yuan Hua Hu transit of the Strait of Hormuz on Wednesday May 13, the Trump-Xi summit commitment on Thursday May 14 that the strait “must remain open,” and the same-day seizure of the Honduras-flagged Hui Chuan off Fujairah per UKMTO Warning 057/26 all happened after Greeks had already placed $10.1 billion in Q1 orders. The Greeks did not need this week’s events to validate their thesis. Their thesis was already placed. This week’s events were confirmation.

The Greek tanker fleet is already the most valuable in the world. Per Veson Nautical’s January 2026 fleet value ranking, the Greek tanker fleet is valued at $77 billion, $21 billion ahead of China’s $56 billion tanker fleet despite China owning more tankers by count. Greek specialization in the larger vessel segments is what drives the value gap. The Q1 2026 ordering wave will widen that gap further.

The Posidonia 2026 conference programme has already begun. Marine Insurance Greece ran May 6-7, with sessions covering sanctions, the rise of the “dark fleet”, US policy shifts and war risk dynamics per Posidonia Exhibitions. The RightShip Conference ran May 7. The Naftemporiki Shipping Conference under the title “Shipping Between Global Powers: Where Geopolitics, Energy & Climate Shape the Future” opens at Four Seasons Astir Palace Hotel Athens on Wednesday May 20. The main Posidonia exhibition runs Monday June 1 through Friday June 5 at Athens Metropolitan Expo. The Capital Link Maritime Leaders Summit opens June 1 in partnership with DNV, marking 20 years of convening top-tier shipowners, financiers, and policymakers per Posidonia Exhibitions. The TradeWinds Shipowners Forum runs June 2 under the theme “Resilience in the face of disruption.” The HELMEPA International Conference runs June 3.

Theodore Vokos, Managing Director of Posidonia Exhibitions, said the urgency of the issues facing shipping today is reflected in the conference programme. “Posidonia has always been more than an exhibition. It is a platform where the industry comes together to address real-world challenges and shape its future direction,” Vokos said per Container News and Maritimes. “This year’s conference programme reflects the urgency of the issues facing shipping today, particularly the impact of geopolitics, energy transition and technological change. The discussions taking place, even before the exhibition officially opens, highlight how critical collaboration and dialogue have become for the industry.” Vokos concluded with the strongest line on the 2026 setup: “Across all events, a clear narrative emerges: shipping is no longer operating at the margins of global developments, it is at their core.”

📊 By The Numbers

→ $10.1 Billion Total Greek Q1 2026 Newbuild Spend Per Xclusiv

→ $6 Billion Greek Q1 2026 Tanker Spend Alone Per Xclusiv

→ 102 Greek Q1 2026 Vessel Orders Versus 28 In Q1 2025 Per Xclusiv

→ 63 Greek Q1 2026 Tanker Orders Versus 13 A Year Earlier Per Cyprus Mail

→ 24 Greek Q1 2026 VLCC Orders Versus 2 In Q1 2025 Per Xclusiv

→ 23 Greek Q1 2026 Suezmax Orders Out Of 41 Global Per GreekReporter

→ 381 Total Greek Tanker Orderbook End Q1 2026 Per Xclusiv

→ 5,543 Total Greek Controlled Vessels Per UGS

→ 21% Greek Share Of Global Tonnage Per UGS

→ $77 Billion Greek Tanker Fleet Value (Most Valuable Globally) Per Veson Nautical

→ 17 Year High Global Orderbook At 191 Million CGT Per BIMCO

→ 140 VLCC Global Orderbook (15% Of Existing Fleet) Per Lloyd’s List

→ 20% Of Existing VLCC Fleet Aged 17 Plus Per Xclusiv

→ Half Of Older VLCC + Suezmax Fleet Sanctioned Per Xclusiv Via Lloyd’s List

→ 40,000+ Professionals Expected At Posidonia 2026 Per Posidonia Events

🔍 Why It Matters

By Gosships analysis, this is the most consequential single-quarter ordering wave in the history of Greek shipping, and the timing relative to Posidonia 2026 is not accidental. The Greeks placed their bet before the world’s top shipyards arrived in Athens to negotiate the next round. They are buying tankers like they already know how this ends.