Europe Is Freezing Russia’s Oil Cap at $44 While the Market Pays $87. Is It Still a Cap?

The EU’s package keeps the cap at $44.10, blacklists 30 more shadow tankers, and for the first time targets the firms that fuel them.

⚓ The Gosships Team

Gosships Intelligence Is Published At Gosships.com

For Sponsorship And Partnership Inquiries Contact intelligence@gosships.com

|⚓ About Us | 🛢️ Exclusive Report | 📋 SwiftAction Training |

🏅Black Gold Membership (*53 Slots Left)

Russia’s oil is legally capped at $44.10 a barrel. It is selling for around $87. That gap is the entire reason the shadow fleet exists, and on June 9 the European Union moved to freeze the cap exactly where it is, locking in a number the market left behind months ago.

📋 In This Issue:

🛢️ The Story

📊 By The Numbers

🔍 Why It Matters

👀 What To Watch

🚨 Gosships Signal

🔔 Not Yet Subscribed? Gosships Intelligence Delivers Oil Shipping Intelligence. Subscribe Here!

📊 Order Our Exclusive Report

→ Global Tanker Market Outlook Q3 2026 Edition

📋 Competency-Based Maritime Training

→ SwiftAction

📌 Gosships Data Card

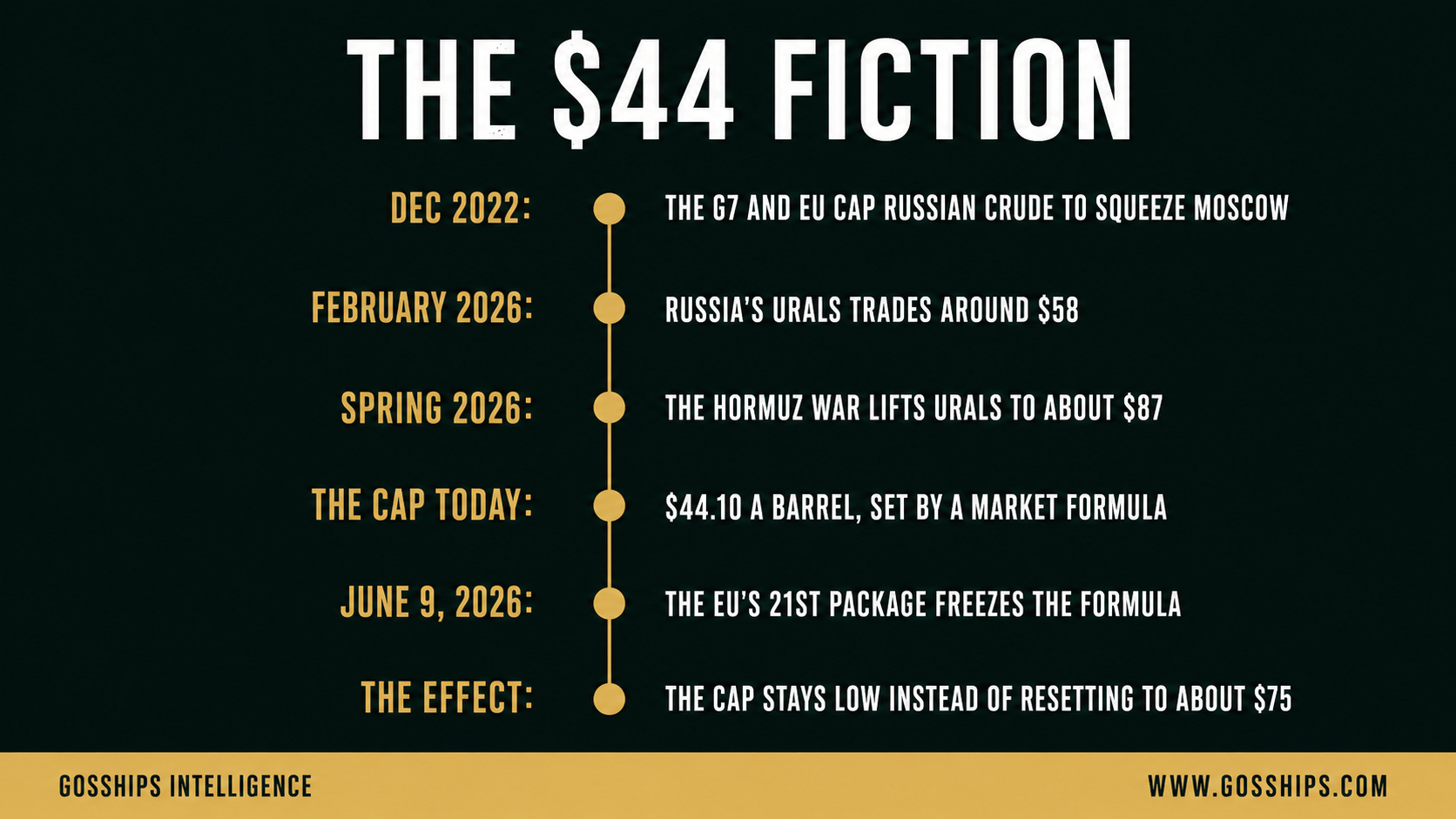

→ December 2022: The G7 And EU Introduce A Price Cap On Russian Seaborne Crude

→ February 2026: Russia’s Urals Grade Trades Around $58 A Barrel

→ Spring 2026: The War Around The Strait Of Hormuz Lifts Urals To About $87

→ The Cap Today: $44.10 A Barrel, Set By A Market-Linked Formula

→ June 9, 2026: The EU’s 21st Sanctions Package Proposes Freezing That Formula Until January

→ The Effect: The Cap Holds At $44.10 Instead Of Automatically Resetting Up To About $75

🛢️ The Story

A price cap only works if it bites. Russia’s stopped biting months ago, and on June 9 the European Union admitted it the only way it could: by freezing the number in place so it could not drift any further from reality.

The European Commission unveiled its 21st package of sanctions against Russia, and the headline measure for this market is the oil price cap. The cap on Russian seaborne crude currently sits at $44.10 a barrel, a level set by a formula that tracks the wider market. The problem is that the wider market has moved. The war around the Strait of Hormuz drove a war premium into global crude, lifted Russia’s Urals grade from roughly $58 a barrel in February to around $87 now, and under the cap’s own automatic mechanism that surge would have reset the ceiling upward, to somewhere near $75. A higher cap means more legal revenue for Moscow at the worst possible moment. So Brussels proposed suspending the adjustment until January, holding the cap at $44.10 rather than letting it climb.

Read that sequence twice, because it is the whole story. The instrument designed to limit Russia’s oil income is now being frozen to stop it from accidentally raising Russia’s oil income. The cap is no longer a lever. It is a line in the sand that the price has already washed over, and the EU is reduced to defending the line itself.

It was not always this hollow. The G7 and the European Union built the price cap at the end of 2022 as a blunt but clever weapon. Let Russia keep selling oil, because the world needed the barrels, but bar Western insurers, financiers and shipowners from touching any cargo sold above a fixed ceiling. For a while it worked, forcing Russian crude to trade at a steep discount to the global benchmark. Then two forces hollowed it out. Moscow assembled a shadow fleet of hundreds of aging tankers carrying non-Western insurance, which could move oil priced above the cap without ever asking a Western firm for help. And the war in the Gulf drove prices high enough that the cap’s own market-linked formula threatened to lift the ceiling toward the very prices it was built to suppress. The freeze is Brussels conceding the second problem so that it does not compound the first.

The package does more than freeze a number. The Commission proposed listing 30 additional vessels tied to Russia’s shadow fleet, bringing the bloc’s total of sanctioned ships past 660. More significant for the trade, the EU said it would, for the first time, target the businesses that service the shadow fleet rather than only the hulls themselves, naming bunkering and other operational support as new categories of exposure. That is a meaningful shift. Sanctioning a tanker takes one ship off the board. Sanctioning the firms that fuel, supply and enable a fleet of hundreds goes after the connective tissue that keeps the entire parallel system running.

None of this happens in a vacuum. The same war around Hormuz that pushed Urals to $87 has scrambled global crude flows, lifted freight to multi-year highs, and pulled a large slice of the world tanker fleet into sanctioned or gray trades. And the EU’s package lands inside a wider campaign that has escalated all year. Since December, the United States, Britain, France, Belgium, India and the EU have seized or detained more than a dozen shadow fleet tankers, leaving hundreds of millions of barrels of sanctioned crude stranded at sea. This month, U.S. prosecutors secured the first criminal guilty plea from a shadow fleet master in American history. In the VLCC class alone, analysts reckon that roughly a quarter of the fleet is now sanctioned or has carried sanctioned barrels. Brussels freezing the cap and naming the fleet’s fuel suppliers is the policy flank of the same offensive. Where the navies take the ships and the courts take the crews, the EU is going after the money and the logistics. The shadow fleet has never faced this many pressures at once, which is precisely why the ships that can still run sanctioned oil have become so valuable.

For shipowners, traders and the compliance desks that have to make sense of all of it, the question is not really about $44.10 versus $87. It is about what a permanently fictional cap, plus a new assault on the fleet’s suppliers, does to the two-tier market that the last three years have built. That is below.

📊 By The Numbers

→ $44.10: The Price Cap On Russian Seaborne Crude, Which The EU Now Proposes To Freeze (European Commission)

→ ~$87: Where Russia’s Urals Grade Is Trading, Up From About $58 In February

→ ~$75: Where The Cap Would Have Reset Under Its Own Formula Without The Freeze

→ 30: Additional Shadow Fleet Vessels Proposed For Listing In The 21st Package (European Commission)

→ 660+: Total Shadow Fleet Vessels Under EU Sanctions After The New Listings

→ First Time: The EU Moves To Sanction Firms That Service The Shadow Fleet, Including Bunkering

Why a frozen cap is quietly bullish for the dark fleet, what hitting the bunker suppliers actually does to sanctioned-oil logistics, and the read-through to compliant tanker rates. Read it below…

🔍 Why It Matters