Greek Owners Just Spent $10 Billion on Ships That Will Not Arrive Until 2028. They Are Betting on the Next Decade, Not This One.

Greek owners ordered 102 vessels in the first quarter, 63 of them tankers. The ships arrive in 2028 and after, which tells you what they expect.

⚓ The Gosships Team

Gosships Intelligence Is Published At Gosships.com

For Sponsorship And Partnership Inquiries Contact intelligence@gosships.com

|⚓ About Us | 🛢️ Deep Water Reports | 📋 SwiftAction Training |

🏅Black Gold Membership (*53 Slots Left)

The most important number at Posidonia this week is not on the exhibition floor. It is in the orderbook, and it says Greek owners are spending at a pace not seen since just before the last great shipping crash.

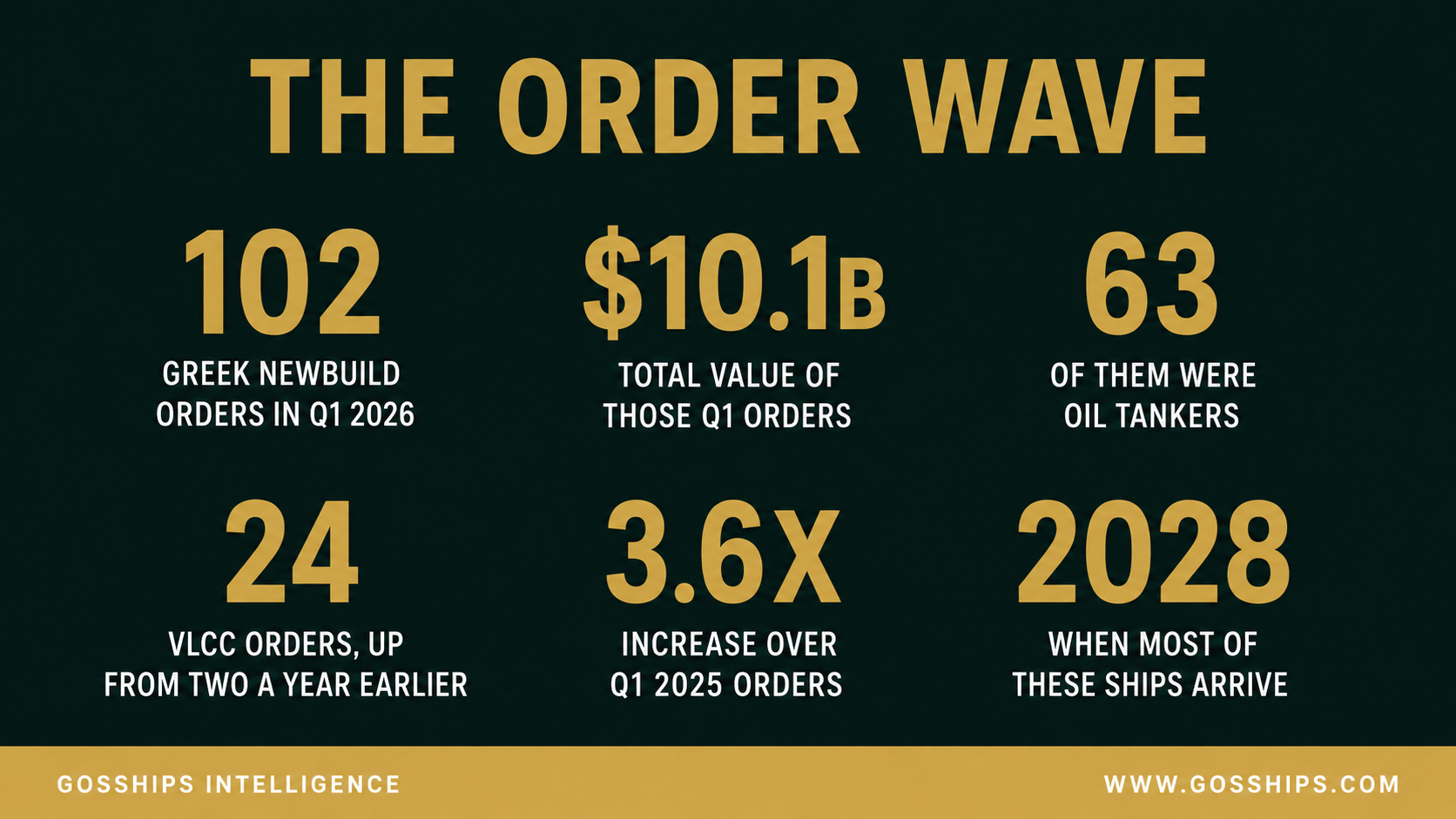

In the first quarter of 2026, Greek-interest owners placed 102 newbuilding orders worth roughly $10.1 billion, according to data from Xclusiv Shipbrokers cited across the Greek and international maritime press. That is about 3.6 times the number of ships they ordered in the same quarter a year earlier, and the brokerage called it the strongest three-month stretch in its records. The overwhelming majority of that money went into one thing: oil tankers, and especially the largest crude carriers afloat.

What makes the surge worth a closer look is not the size of the spending alone. It is the timing built into it. Almost none of these ships will touch the water before 2028. Greek owners are not buying capacity to cash in on today’s elevated freight rates. They are placing a multibillion-dollar bet on what the crude trade will look like years from now, and the shape of that bet is worth reading carefully.

📋 In this issue:

🛢️ The Story

📊 By The Numbers

🔍 Why It Matters

👀 What to Watch

🚨 Gosships Signal

📊 Get The Deep Water Report

→ Global Tanker Market Outlook Q2 2026

📋 Competency-Based Maritime Training

→ SwiftAction

📌 Gosships Data Card

→ The Orders: Greek-Interest Owners Placed 102 Newbuilding Orders in the First Quarter of 2026 Per Xclusiv Shipbrokers Via Cyprus Mail

→ The Value: Those Orders Were Worth About $10.1 Billion, the Brokerage’s Strongest Quarter on Record Per Xclusiv Shipbrokers Via Shipping Herald

→ The Tanker Share: 63 of the 102 Vessels Were Tankers, Worth Roughly $6 Billion Per Xclusiv Shipbrokers Via Cyprus Mail

→ The Big Crude: 24 VLCCs and 23 Suezmaxes Made Up About 75% of Greek Tanker Orders Per Xclusiv Shipbrokers Via Shipping Herald

→ The Jump: VLCC Orders Rose to 24 From Just Two in the First Quarter of 2025 Per GreekReporter Citing Xclusiv

→ The Orderbook: The Greek Tanker Orderbook Reached About 396 Vessels, Around 28% of the Global Total Per Xclusiv Shipbrokers Via Shipping Herald

🛢️ The Story

This is a story about a fleet betting on the next decade, not the next quarter.

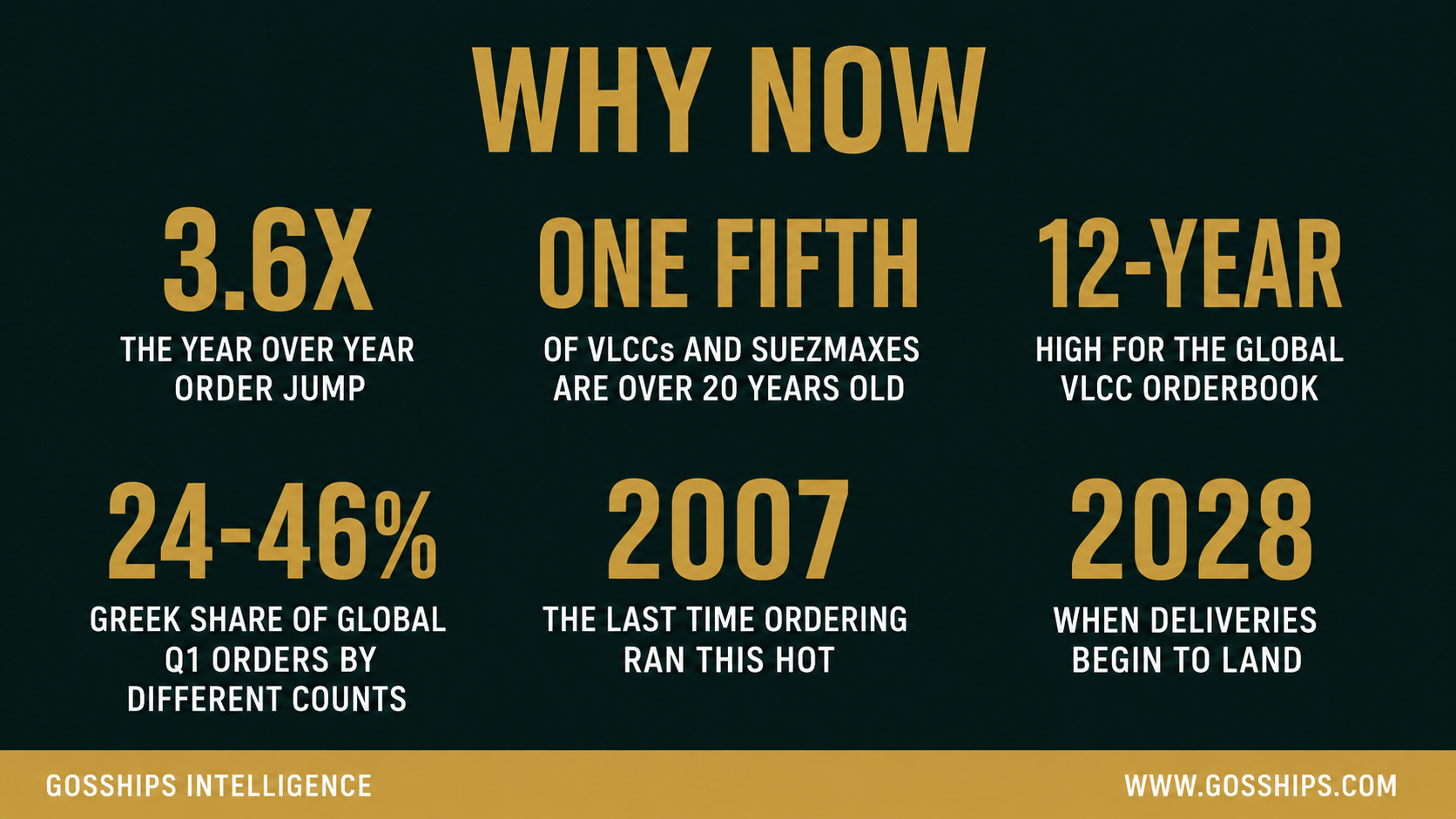

The scale. The headline figure from Xclusiv Shipbrokers is stark. Greek-interest owners ordered 102 newbuildings in the first quarter of 2026, against 28 in the same period of 2025, a roughly 3.6-fold jump and, by the brokerage’s account, its strongest quarter on record. Global contracting rose over the same period, but the Greek share of it was outsized: estimates of that share vary by how it is measured, from about 24 percent of global newbuilding activity by Xclusiv’s count reported by Riviera, to nearly half by other tallies in the Greek press. The total value, about $10.1 billion in three months, is the kind of number that gets analysts reaching for historical comparisons.

The tanker tilt. This was, above all, a bet on oil. Of the 102 vessels, 63 were tankers, worth roughly $6 billion, and the orders concentrated heavily in the biggest crude carriers. Greek owners booked 24 very large crude carriers and 23 suezmaxes in the quarter, and those two segments together made up about three quarters of all Greek tanker orders. The VLCC figure is the one that stops you: 24 of them, against just two in the first quarter of 2025. That is not a gradual build. It is a step change in a single year.

The delivery dates. Here is the detail that reframes everything. These ships are not arriving in time to ride the current market. Crude tanker deliveries from the recent ordering wave are scheduled largely from 2028 onward, with shipyard positions in Asia stretched well into that year and beyond. An owner who orders a VLCC today and takes delivery in 2028 is making a statement about 2028, not about this month’s rates. The capital is being committed to a forward view, which is what makes the surge a signal rather than a reaction.

The historical echo. The intensity has drawn comparisons that carry a note of caution. Xclusiv described the cycle as reminiscent of the bullish ordering that preceded the 2008 global financial crisis, and one trade outlet framed the activity as a return to 2007 levels. That comparison cuts both ways. It signals genuine conviction and deep pockets, but it also recalls a period when a wave of newbuildings arrived into a market that had turned, leaving owners with capacity they had ordered at the top. Whether 2026 rhymes with 2007 in that sense is exactly the open question, and it is one the owners are clearly willing to bet against.

The suezmax angle. While the VLCC jump grabs attention, the suezmax orders are their own signal. Greek principals booked 23 suezmaxes in the quarter, a large share of the global total for that segment, and analysts read it as deliberate rather than incidental. The suezmax is the flexible workhorse of the crude trade, large enough to be economic on long hauls yet able to serve routes and ports a VLCC cannot, and it has outperformed on earnings while offering optionality across both Atlantic and East-of-Suez markets. In a period when owners cannot be certain which routes will dominate by 2028, ordering a vessel that can profitably serve several is a hedge built into the steel itself.

The selling side. The ordering wave has a mirror image that is just as telling: Greek owners have been among the most active sellers of older tonnage even as they buy new. Aging vessels have changed hands at elevated secondhand values, in some cases with eight-year-old ships fetching prices at or above the cost of a comparable newbuilding. That two-sided activity, selling old ships near the top of the market while ordering modern ones for delivery years out, is the same disciplined pattern visible at the individual-owner level across the Greek fleet. It is not simply expansion; it is fleet renewal, funded in part by the high prices the old ships are commanding on the way out.

The reasoning. The case for ordering now, as analysts describe it, rests on a few reinforcing factors. The existing fleet is old: by Xclusiv’s estimate, roughly a fifth of the world’s VLCCs and suezmaxes are now more than 20 years old, which means a large block of tonnage will need replacing regardless of the rate cycle. Sanctions on Russian and other restricted trades have pulled a meaningful number of ships out of mainstream service, shrinking the effective trading fleet below what headline numbers suggest. And the lengthening of crude routes, as cargoes travel further to reach buyers, has reset the ton-mile math in tankers’ favor. Put together, the argument is that demand for modern, compliant, long-haul crude capacity will outlast the current geopolitical moment, and that the time to secure a shipyard slot is before everyone else reaches the same conclusion.

The shipyard squeeze. There is also a simpler, more mechanical reason the orders bunched into a single quarter. Shipyard capacity in Asia is finite, and as owners rushed to book slots, delivery positions stretched further out and prices firmed. That created a self-reinforcing urgency: the more owners ordered, the scarcer and more expensive the remaining berths became, and the stronger the incentive to commit before the window narrowed further. Early commitment, as one brokerage put it, became a matter of competitiveness rather than choice, because the owners who hesitated risked being left with later, costlier delivery dates that would leave their fleets older for longer.

For traders, brokers and owners watching from the sidelines, the question that follows is whether this is foresight or the familiar overshoot of a hot market. The full read is below.

📊 By The Numbers

→ The Aging Fleet: Roughly One Fifth of the World’s VLCCs and Suezmaxes Are More Than 20 Years Old Per Xclusiv’s Eirini Diamantara Via Neos Kosmos

→ The Orderbook High: The Global VLCC Orderbook Has Climbed to a 12-Year High Per Greek City Times

→ The Greek Share: Estimates of the Greek Share of Global Q1 Orders Range From About 24% Per Xclusiv Via Riviera to Nearly Half Per Other Greek Press Tallies

→ The Historical Echo: Xclusiv Compared the Intensity to the Pre-2008 Ordering Cycle Per Shipping Herald

→ The Triple: Greek Orders Rose 3.6 Times From 28 Vessels in Q1 2025 Per Xclusiv Shipbrokers Via Shipping Herald

→ The Sanctions Factor: Sanctions Have Shrunk the Effective Trading Fleet, Pushing Owners to Order Early Per Lloyd’s List

Found this useful? Share Gosships Intelligence with a colleague.

Why the delivery date matters more than the order count. What the 2007 comparison gets right and wrong. The single risk that could turn this bet against the owners who made it. Below.

🔍 Why It Matters

The order count is the headline. The delivery date is the story.