MSC, COSCO, HMM and Other Container Giants Are Quietly Building Crude Tanker Fleets. What's the Strategy?

Some, like COSCO and HMM, have run tankers for years and are expanding; MSC just bought in; others, like Maersk and CMA CGM, are staying with containers.

⚓ The Gosships Team

Gosships Intelligence Is Published At Gosships.com

For Sponsorship And Partnership Inquiries Contact intelligence@gosships.com

|⚓ About Us | 🛢️ Exclusive Report | 📋 SwiftAction Training |

🏅Black Gold Membership (*53 Slots Left)

The world’s largest container shipping company does not just move containers anymore, and it is far from the only one. From Geneva to Beijing to Seoul to Tokyo, the giants of container shipping are pouring money into crude oil tankers. MSC is entering the business for the first time, on a vast scale. Others, including COSCO, HMM and the Japanese owners behind ONE, have quietly run tanker fleets for years and are now growing them fast. A few of the biggest names are doing the opposite, doubling down on containers and logistics instead. The split is too deliberate to be a coincidence, which raises the obvious question: what are these container carriers really after?

📋 In this issue:

🛢️ The Story

📊 By The Numbers

🔍 Why It Matters

👀 What to Watch

🚨 Gosships Signal

🔔 Not Yet Subscribed? Gosships Intelligence Delivers Oil Shipping Intelligence. Subscribe Here!

📊 Order Our Exclusive Report

→ Global Tanker Market Outlook Q3 2026 Edition

📋 Competency-Based Maritime Training

→ SwiftAction

📌 Gosships Data Card

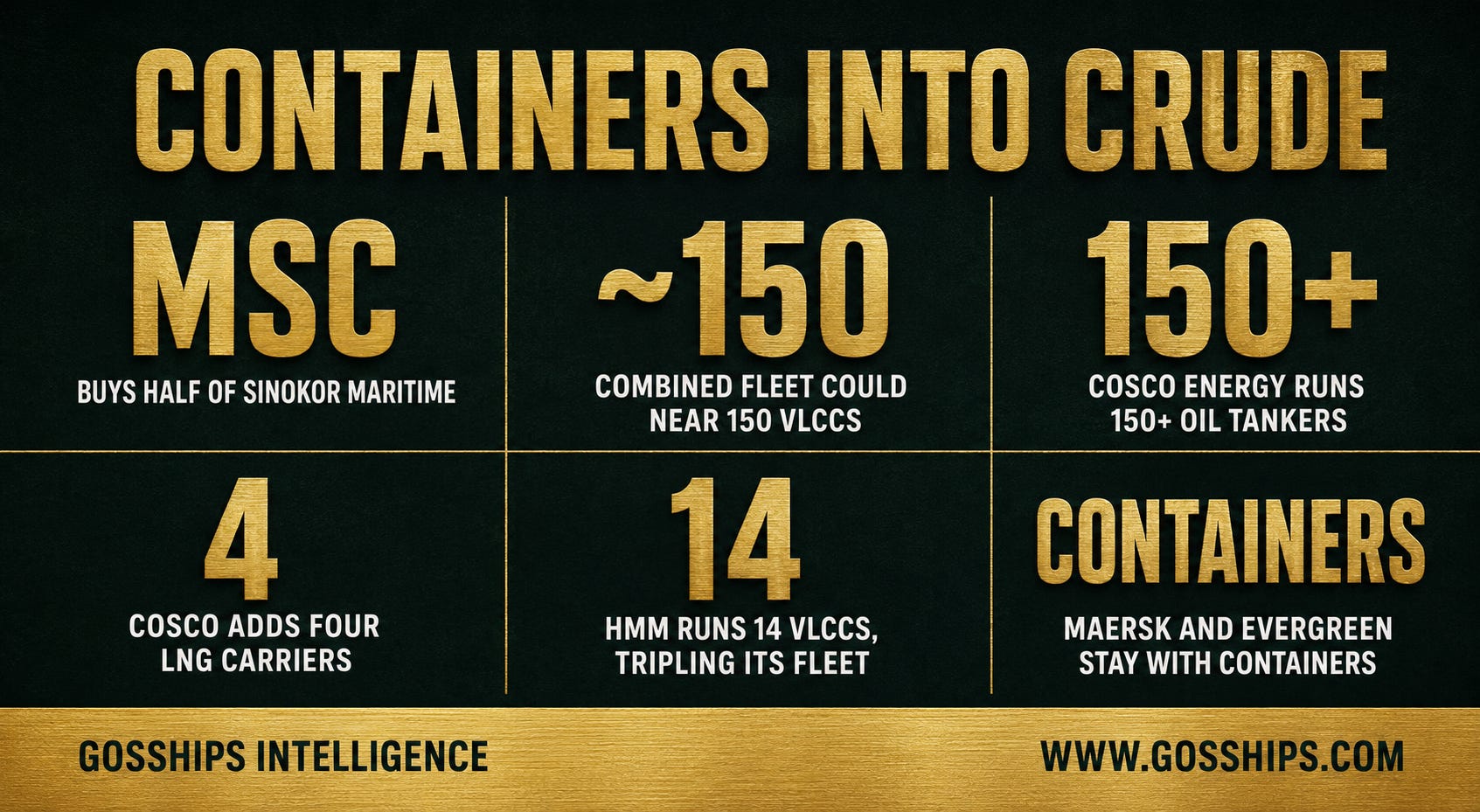

→ MSC Is Buying Half Of Sinokor Maritime Through A Luxembourg Subsidiary. Per Splash 247 And Lloyd’s List.

→ Bloomberg Estimates The Combined Fleet Could Reach About 150 VLCCs. Per Splash 247.

→ COSCO’s Energy Arm Runs More Than 150 Oil Tankers. Per Seatrade Maritime.

→ It Just Ordered 4 LNG Carriers Worth About $953 Million. Per Splash 247.

→ HMM Operates 14 VLCCs And Is Tripling Its Tanker And Bulk Fleet. Per Maritime Executive And Splash 247.

→ Maersk And Evergreen Are Doing The Opposite And Doubling Down On Containers. Per Maritime News.

🛢️ The Story

The move that gave it away:

For months, the tanker market watched a South Korean operator named Sinokor buy very large crude carriers at a pace nobody could explain, snapping up dozens of vessels and paying far above prevailing prices to pull tonnage off the market. In March, the buyer behind the money was confirmed. According to Splash 247 and Lloyd’s List, competition filings in Cyprus and Greece disclosed that MSC, the world’s largest container line, had agreed through its Luxembourg-registered subsidiary SAS Shipping Agencies Services to acquire a 50 percent stake in Sinokor Maritime, taking joint control of the company alongside founder Ga-Hyun Chung. Seatrade Maritime reported the framework agreement had been signed in early February. The scale is without precedent. Bloomberg, as reported by Splash 247, estimated the combined MSC and Sinokor fleet could eventually reach around 150 VLCCs, a figure that on Bloomberg’s math would represent close to 40 percent of the supertankers operating outside the sanctioned shadow fleet. Other houses are more conservative. Norwegian broker Fearnleys, cited by Splash, put Sinokor’s share at more than one in four compliant VLCCs and called the Korean owner the “kingpin” of the VLCC market, while BRS calculated roughly 118 vessels under ownership or charter. Signal Ocean described the buildup as “an unprecedented level of concentration for a single commercial entity.” Whatever the exact number, the direction is the same: the biggest name in containers is now one of the biggest names in crude.

MSC has not commented publicly, and Maritime Executive noted it is not the first time the group has used SAS to enter a new segment, having bought into car carrier Gram Car Carriers in 2024. Lloyd’s List, citing multiple industry sources, has linked MSC co-founder Gianluigi Aponte personally to the buildup, reporting that he set aside as much as $5 billion for the tanker push. The transaction still needs competition clearance, and until it closes the two parties are described as exercising joint control. What is no longer in doubt is the intent. The most valuable container franchise on earth looked at the cash it threw off during the container boom and chose to plant a large part of it in crude tankers, a market it had never owned at anything like this scale before.

The giant that was always both:

MSC’s move looks dramatic because it came from a pure container champion. COSCO needed no such conversion. The Chinese state-owned group runs the world’s fourth-largest container line, but it also controls one of the largest tanker fleets on the planet through its publicly listed energy arm, COSCO Shipping Energy Transportation. According to Seatrade Maritime, that arm operates more than 150 oil tankers, ranking as the world’s largest tanker operator, and Breakwave Advisors noted it stood as the single largest VLCC operator in 2024 before Sinokor’s surge. Far from slowing down, COSCO keeps ordering. Maritime News reported that at an extraordinary general meeting in late January, COSCO Shipping Energy approved a wave of shipbuilding contracts signed in December for methanol dual-fuel crude and product tankers across the Aframax, LR2, LR1 and MR classes. And just this week, Splash 247 reported the company ordered four 175,000 cubic metre LNG carriers at Jiangnan Shipyard for about $953 million, with the ships chartered to Shell for seven years on delivery. COSCO said the order would strengthen its LNG fleet and support its long-term growth strategy. The container giant and the tanker giant are, in COSCO’s case, the same company, and that company is spending heavily to grow the crude and gas side.

The challenger from Seoul:

South Korea’s HMM completes the picture. It is the world’s eighth-largest container carrier, yet according to Maritime Executive it already operates 14 VLCCs and seven product tankers. Splash 247 reported that HMM’s medium-term strategy, worth roughly $17.5 billion through 2030, calls for its tanker and dry bulk fleets to triple in size, and that its October order included two new VLCCs alongside a dozen container ships. The appetite has not cooled. Banchero Costa, cited by Hellenic Shipping News, reported this week that HMM is rumored to have ordered four more VLCCs at China’s Hengli yard. HMM is the clearest example of a container line that decided crude was a business it wanted to own outright rather than charter.

The Japanese houses behind ONE:

The pattern reaches Tokyo too. Ocean Network Express, the world’s sixth-largest container line, carries only containers itself, but it is jointly owned by three Japanese groups, NYK, Mitsui O.S.K. Lines and K Line, that each run large tanker and energy-shipping arms. They are not standing still. MOL took delivery of its first LNG dual-fuel VLCC, the Energia Viking, for Equinor and has ordered another for Idemitsu, according to Offshore Energy, while MarineLink reported that NYK contracted its first methanol dual-fuel VLCC, a crude carrier built by Nihon Shipyard, for long-term charter to Idemitsu Tanker. The companies behind one of the biggest names in containers are quietly modernizing and enlarging their crude fleets at the same time.

The lines betting the other way:

It is not universal, and that is half the story. Three of the five biggest container lines are staying out of crude. Maersk, long the symbol of global container shipping, sold its tanker arm to the founding family's holding company in 2017 and rebuilt the listed group around containers and integrated logistics. The Maersk-branded tanker business that remains sits outside that listed company and is a product-tanker operation, not a crude one. CMA CGM, the third-largest carrier, is pouring its capital into LNG and methanol-powered container ships and an Indian-flag fleet, not oil tankers. Hapag-Lloyd is concentrating on its liner network and its move to absorb ZIM, while Evergreen ordered 23 new container ships worth around $1.47 billion in January, according to Maritime News, a clear bet on containers. The divide is strategic. One camp is hedging into crude. The other is concentrating on the container and logistics chain it knows best, and the contrast itself signals how differently the biggest players read the next decade.

Why now:

The timing is not random. On the container side, a record newbuilding orderbook is the overhang. Alphaliner data puts the global container ship orderbook at roughly a third of the existing fleet, and as Red Sea security improves and diverted ships return to the Suez route, that returning capacity threatens to outrun trade growth and weigh on freight rates over the medium term, even though an early peak season has lifted spot rates sharply in recent weeks, with Drewry’s main index jumping 23 percent in a single week. On the tanker side, the pressure runs the other way. Clarksons data shows 10-year-old VLCCs changing hands around $110 million, up more than a fifth since the start of the year and the highest in a decade, while Signal Ocean tracks gains of more than 130 percent over five years, a surge driven by sanctions, the reshaping of crude trade routes and the disruption around the Strait of Hormuz. For a container group sitting on cash from the boom years, buying into crude does two things at once. It smooths earnings against the container cycle, and it lets the group reuse the crews, technical management and financing muscle it already has. For a refiner-facing operator like HMM, owning tankers also locks in the logistics of getting oil home. These container groups are not abandoning their core business. They are buying an insurance policy written in barrels.

The other side of the bet:

None of this is risk-free, and the timing cuts both ways. The container groups are buying crude tonnage at the most expensive levels in over a decade, and asset prices that climbed on war and disruption can fall just as fast when those conditions ease. If the Strait of Hormuz reopens to normal traffic and the sanctioned-trade premium fades, the same VLCCs bought near $110 million could be worth far less, leaving a container balance sheet exposed to a tanker downturn it does not fully control. Concentration carries its own hazard. A platform that dominates a quarter or more of the compliant fleet becomes a target for regulators and for charterers determined not to depend on a single counterparty. And running two very different shipping businesses at scale stretches management attention in a market where both containers and tankers tend to reward focus. The container lines are betting that diversification beats specialization. The owners going the other way are betting it does not.

For the full rate forecast and fleet supply outlook behind this shift, and what a handful of container groups controlling a large slice of the crude fleet means for everyone who charters a tanker, the analysis is below.

📊 By The Numbers

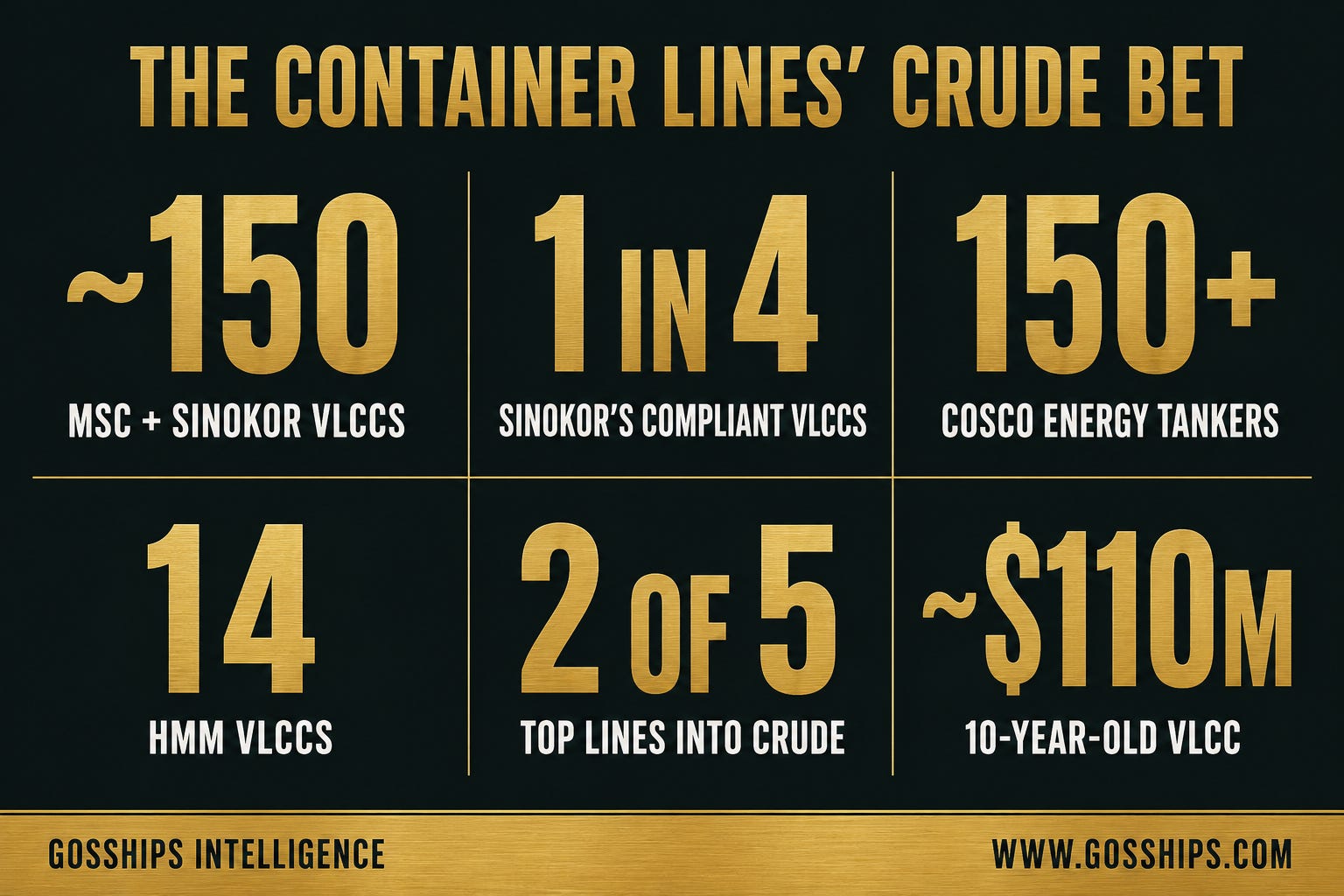

→ MSC Is The World’s Largest Container Line And Now Joint Owner Of The Biggest VLCC Fleet Ever Assembled. Per Bloomberg And Splash 247.

→ COSCO Ranks Fourth In Containers And Runs One Of The World’s Largest Tanker Fleets. Per Seatrade Maritime And Breakwave Advisors.

→ HMM Ranks Eighth And Operates Fourteen VLCCs And Seven Product Tankers. Per Maritime Executive.

→ Container Lines Face A Record Newbuild Orderbook Even As An Early Peak Season Lifts Spot Rates. Per Alphaliner And Drewry.

→ Ten-Year-Old VLCCs Are Changing Hands Around $110M, The Highest In A Decade. Per Clarksons.

→ Not Every Line Is Following. Maersk And Evergreen Are Betting On Containers. Per Maritime News.

Found this useful? Share Gosships Intelligence with a colleague.

When the companies that move the world’s manufactured goods start buying the ships that move the world’s oil, the question stops being who owns the tankers and becomes who controls them. What that concentration means for charterers, traders and compliance desks, and whether regulators will let it stand, is below.

🔍 Why It Matters

For VLCC owners and brokers:

A new class of buyer has entered the supertanker market, and it is not a traditional tanker owner. It is a set of