Shipping's First Carbon Price Faces a Make-or-Break Vote in December. The U.S. Wants It Dead.

After surviving a U.S. push to kill it in April, the IMO's $100-to-$380-a-ton carbon levy faces a decisive vote on December 4, 2026

⚓ The Gosships Team

Gosships Intelligence Is Published At Gosships.com

For Sponsorship And Partnership Inquiries Contact intelligence@gosships.com

|⚓ About Us | 🛢️ Exclusive Report | 📋 SwiftAction Training |

🏅Black Gold Membership (*53 Slots Left)

A laden supertanker burns roughly 60 to 90 tonnes of fuel a day at sea, and from 2028 the world wants to start charging for the carbon in it. The United States has tried twice to stop that plan. Twice it has survived. In April the framework lived through a five-day fight in London and was declared back on track, and the decisive adoption vote is now six months away, in December 2026. The entire tanker market is already trading on the outcome.

📋 In This Issue:

🛢️ The Story

📊 By The Numbers

🔍 Why It Matters

👀 What To Watch

🚨 Gosships Signal

🔔 Not Yet Subscribed? Gosships Intelligence Delivers Oil Shipping Intelligence. Subscribe Here!

📊 Order Our Exclusive Report

→ Global Tanker Market Outlook Q3 2026 Edition

📋 Competency-Based Maritime Training

→ SwiftAction

📌 Gosships Data Card

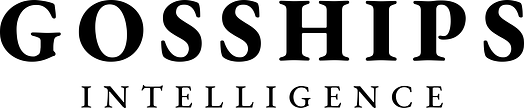

→ April 2025: The IMO Approves The Net-Zero Framework As Draft Legal Text At MEPC 83

→ October 2025: A Saudi Motion Backed By U.S. Pressure Adjourns The Adoption Vote, 57 To 49

→ April 2026: The Framework Survives Five Days Of Debate At MEPC 84 And Is Declared Back On Track

→ September And November 2026: Two Intersessional Working Group Meetings To Rebuild Consensus

→ December 2026: A Resumed Extraordinary Session, Penciled For December 4, Is The Next Chance To Adopt

→ 2028: Mandatory Carbon-Intensity Targets And Pricing Would Take Effect If Adopted

🛢️ The Story

The first global carbon price on shipping has now survived two attempts to kill it, and the second one tells the market more than the first. In October 2025 the United States and Saudi Arabia froze its adoption. In April 2026 the framework went through a five-day fight at the IMO and came out the other side intact. The question is no longer whether it is dead. The question is what it does to the tanker market when it lands, and that answer now points at December.

The instrument is the IMO Net-Zero Framework, a set of amendments to the MARPOL pollution treaty approved as draft legal text at the International Maritime Organization’s MEPC 83 session in April 2025. It does two things at once. It sets a declining limit on the greenhouse-gas intensity of marine fuel, measured well to wake, with targets that begin in 2028 and tighten every year through 2035. And it attaches a price to missing those limits. Ships that exceed the tighter Direct Compliance Target would buy remedial units at $100 per tonne of CO2 equivalent, and ships that breach the looser Base Target would pay $380 per tonne, with both prices fixed for the 2028 to 2030 window, according to a legal analysis by King & Spalding. The proceeds flow into a new IMO Net-Zero Fund that rewards cleaner ships and bankrolls fuel infrastructure.

The framework reaches almost the entire blue-water fleet. It covers every ship above 5,000 gross tonnes, a class that together accounts for more than 85 percent of the industry’s carbon output, and in practice that means every VLCC, Suezmax and Aframax afloat. The IMO estimates the fund would raise on the order of $10 billion a year, and the European Commission has put the figure higher, at $11 billion to $13 billion annually. For a single ship, the early bite is concrete: Ship & Bunker reported that owners can expect to pay roughly $76 in compliance cost for every tonne of very low sulfur fuel oil burned in 2028.

None of this is hypothetical, because Europe already charges a version of it. Since January 2024 the European Union has folded shipping into its Emissions Trading System, requiring owners to surrender carbon allowances for voyages that touch EU ports, whatever flag the ship flies. That scheme reaches full strength in 2026, covers the same vessels above 5,000 gross tonnes, and at current allowance prices an industry group estimated it adds around $400,000 to the cost of running a tanker in 2024, climbing to roughly $1.1 million per tanker in 2026. The IMO framework would not invent a carbon price for shipping. It would take the regional one Europe already collects and make it global.

That is what makes it historic, and that is what Washington has spent a year trying to stop. At the extraordinary session in London from October 14 to 17, 2025, the session never reached a clean vote on the measure. Saudi Arabia moved to adjourn for a year. The motion carried 57 to 49, with 21 abstentions, and adoption was pushed back. President Trump branded the measure a “Global Green New Scam Tax on Shipping” and said the United States would not adhere to it in any way, shape or form. Secretary of State Marco Rubio called the delay a win that spared consumers a “massive UN tax hike.” Ahead of the vote, the administration warned supporters they could face tariffs, port levies and visa restrictions, according to reporting by Reccessary and others. Delegations from developing nations described the lobbying as “bullying.”

Then, in April 2026, the framework refused to die. Over five days at MEPC 84 in London, with the United States, other fossil-fuel producers and parts of the industry pushing to strip out the carbon-pricing mechanism or scrap the framework entirely, support held. The measure emerged intact, the committee set a new path to adoption, and IMO Secretary-General Arsenio Dominguez told delegates, “We are back on track, but we have to rebuild trust.” To get there, members agreed to two intersessional working group meetings, in September and November, before MEPC 85 from November 30 to December 3, with a resumed extraordinary session penciled in for December 4. That December session is now the next formal chance to adopt the framework.

So the world’s first global carbon price did not die in October, and it did not die in April. It has a date, December 2026, and a fight still ahead of it. What that fight does to fuel bills, to newbuilding choices, and to the value of the ship a broker fixes tomorrow is the part that matters to this market, and it is below.

📊 By The Numbers

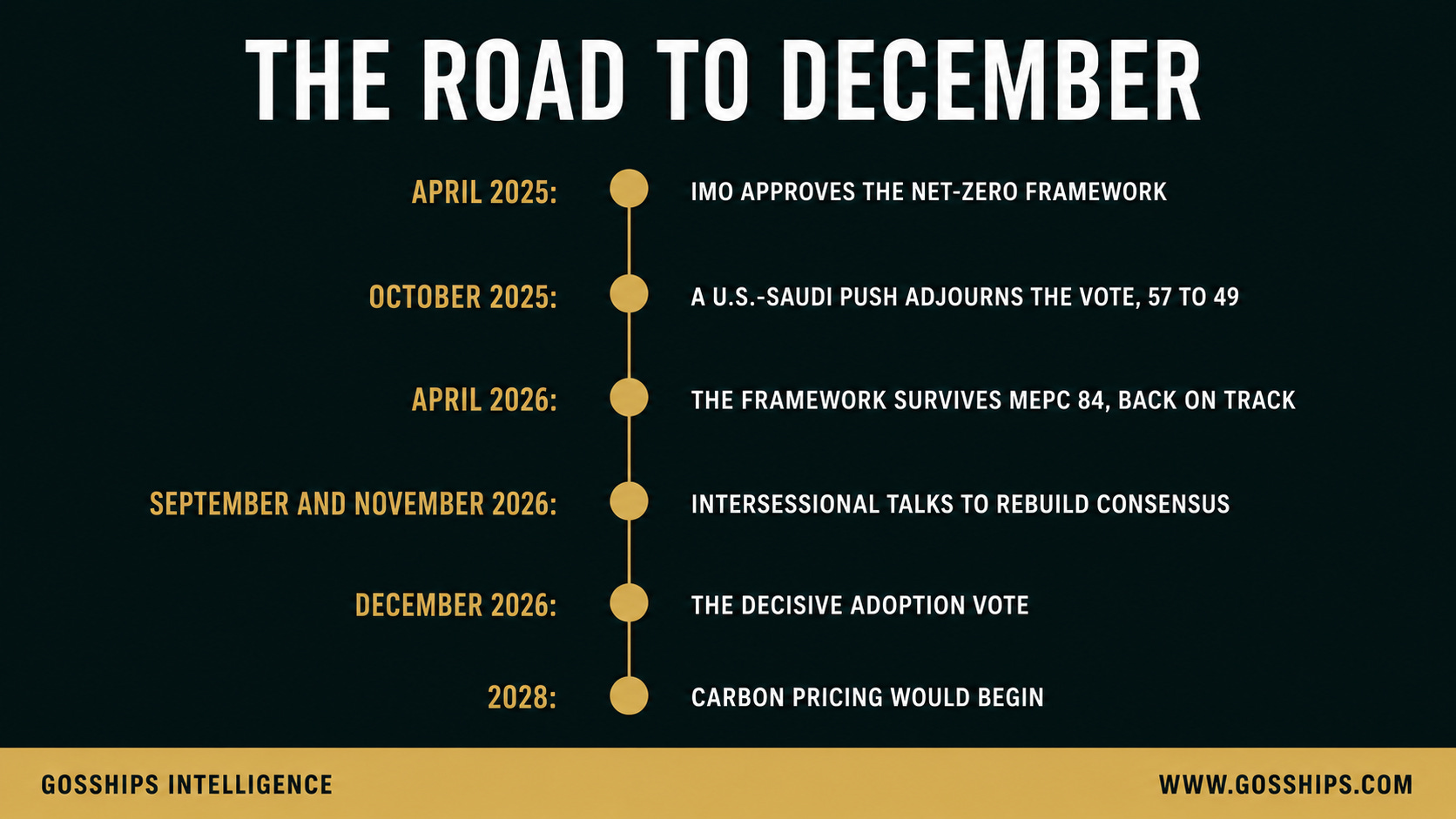

→ $100 To $380: The Remedial Unit Price Per Tonne Of CO2 Equivalent, Fixed For 2028 To 2030 (King & Spalding)

→ $76: The Estimated Extra Compliance Cost Per Tonne Of VLSFO Burned In 2028 (Ship & Bunker)

→ $10 Billion A Year: The IMO’s Projected Net-Zero Fund Revenue, With The EU Estimating $11 To $13 Billion (IMO; European Commission)

→ ~$1.1 Million: The Estimated EU ETS Carbon Cost Per Tanker In 2026, The Regional Price The IMO Rules Would Make Global (Industry Estimate)

→ 5,000 GT: The Ship Size Threshold The Rules Cover, Roughly 85% Of Shipping Emissions

→ 57 To 49: The October 2025 Vote To Adjourn, With 21 Abstentions

→ December 2026: The Resumed Extraordinary Session, Penciled For December 4, Where Adoption Is Now Targeted

→ 2028: When Mandatory Targets And Pricing Would Begin If Adopted

What the carbon price does to a single VLCC’s voyage economics, why the record newbuilding orderbook is really a wager on the December vote, and the second-order effect that could push rates higher rather than lower.

🔍 Why It Matters