Sinokor Is Charging $20 Per Barrel to Ship Oil. Last Year It Was $2.50. They Control 40% of Available Tankers. Nobody Can Do Anything About It.

MSC confirmed behind the buying spree. 150 supertankers under one roof. Charterers have no alternatives. Brokers are calling it unprecedented. The question nobody is asking publicly: is this legal?

|⚓About Us |🛢️Deep Water Reports |📋SwiftAction Training |

🏅Founding Gold Anchor Membership (*53 Slots Left)

It cost $2.50 per barrel to ship crude oil from the Middle East to China on a VLCC last year.

On March 2, Sinokor quoted 700 Worldscale points for the same route.

That is roughly $20 per barrel. An eightfold increase.

This is not a war premium. War premiums affect everyone equally. This is one company, backed by the world’s largest shipping empire, controlling enough of the available tanker fleet to set the price.

Bloomberg reported the figure. Shipbrokers confirmed it. And Fearnleys, one of the most respected brokerages in the tanker market, said the quiet part out loud: “The front end of the position list is shrinking by the hour, leaving charterers with few other alternatives to choose from but the South Korean giant.”

One competitor estimated that Sinokor now controls approximately 150 vessels, or nearly 40% of unsanctioned ships available for immediate charter.

The freight market for the world’s largest crude oil tankers is no longer a market. It is a pricing desk with one operator behind it.

📋 In this issue:

🛢️ The Story

📊 By the Numbers

🔍 Why It Matters

👀 What to Watch

⚓ Gosships Signal

📊 GOSSHIPS DATA CARD

🛢️ The Story

Sinokor Merchant Marine has done something no single operator has ever done in the modern VLCC market: accumulated enough tonnage to dictate pricing on the world’s most important crude oil shipping route.

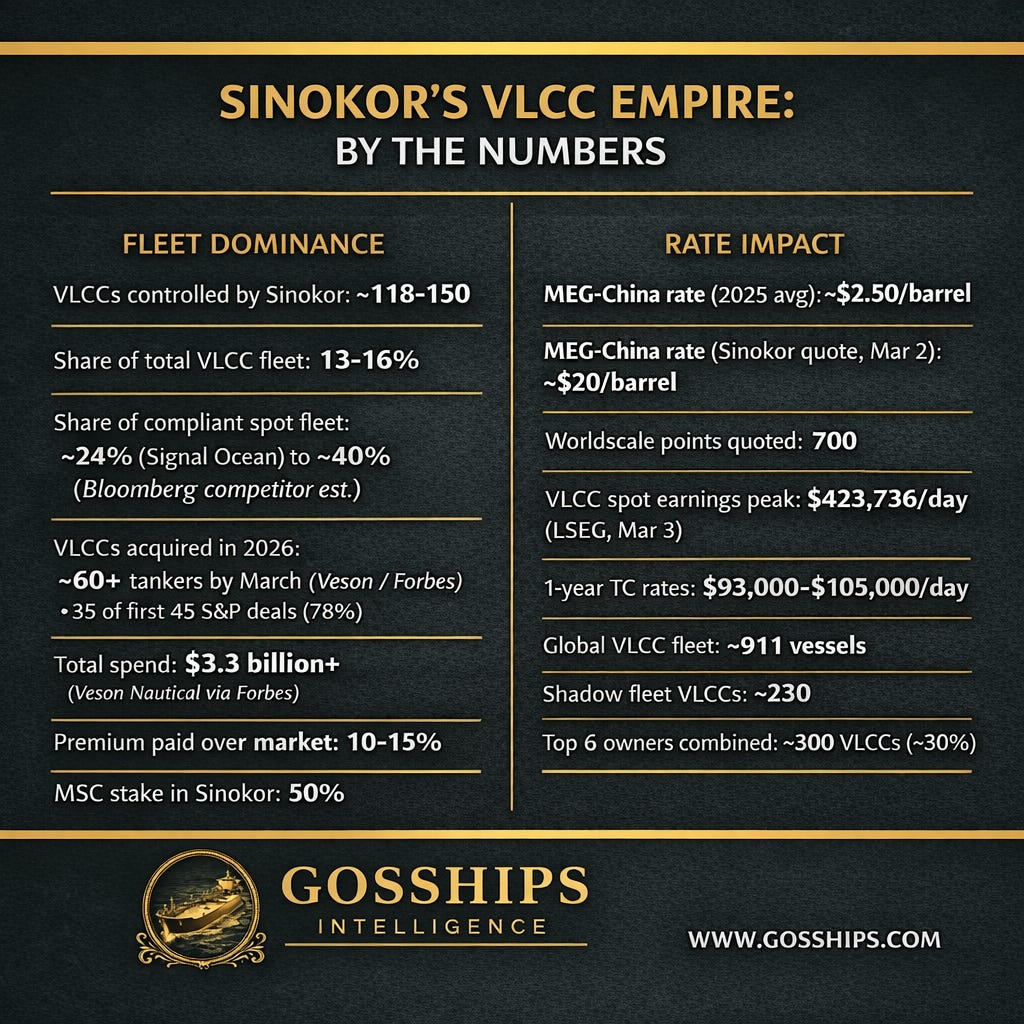

The story began in mid-December 2025 when brokers noticed an unusual spike in VLCC sale-and-purchase activity. By January 2026, the buyer behind the spree was identified: South Korea’s Sinokor, a mid-tier operator previously ranked 12th among global VLCC owners. In the opening weeks of the year alone, Sinokor acquired 35 out of 45 VLCCs sold globally, absorbing 78% of all transaction volume in the sector, according to Veson Nautical. By March, Forbes reported that $3.3 billion had changed hands for at least 60 tankers, citing Veson Nautical data. Sources put the total number of tankers acquired at 76, with other analyses believing it could be higher. The company focused on tonnage built between 2010 and 2016, paying 10 to 15% above prevailing market valuations to lock down sellers, according to Gibson Shipbrokers.

On March 19, public filings in Cyprus and Greece confirmed what the market had speculated for months. MSC Mediterranean Shipping Company, the world’s largest container shipping line controlled by Italian billionaire Gianluigi Aponte, is formally behind the expansion. MSC’s Luxembourg-registered entity SAS Shipping Agencies Services signed an investment framework agreement on February 2 to acquire a 50% stake in Sinokor, with founder Ga-Hyun Chung retaining the other half. The deal was notified to the Cypriot Competition Commission on February 25 and published by the Greek Competition Commission on March 13. The deal formalizes joint control. The world’s largest container shipping company and a Korean tanker operator now jointly control the largest VLCC fleet ever assembled under a single commercial platform.

The scale is staggering. BRS, the French shipbroker, estimated that when all acquisitions and charters are delivered, Sinokor will control 118 VLCCs through ownership or time charter. That represents 13% of the total active VLCC fleet and 16% of the mainstream non-sanctioned fleet. One competitor put the figure even higher: approximately 150 vessels, or close to 40% of unsanctioned ships available for immediate charter on the spot market, according to Bloomberg. Signal Ocean projected that Sinokor would independently control at least 24% of the global compliant VLCC spot fleet in 2026. BRS stated bluntly: “There has never before been a single VLCC operator with such a dominant market share of the active fleet.” Fearnleys called them the “kingpin” of the VLCC trades.

The pricing impact was immediate. On March 2, as the Iran war broke out and Hormuz traffic collapsed, Sinokor indicated to brokers that its going rate for the benchmark Middle East Gulf to China route was 700 Worldscale points, according to Bloomberg, citing people with knowledge of the matter. Two shipbrokers confirmed that 700 WS translates to roughly $20 per barrel for a cargo to eastern China. The 2025 average for the same route was approximately $2.50 per barrel. VLCC spot earnings on the MEG-China route exceeded $200,000 per day in late February, according to Fearnleys, and hit an all-time record of $423,736 per day on March 3, according to LSEG data.

Fearnleys’ weekly report laid out the dynamic in plain language. “The VLCC market has continued on an upward trajectory in the week gone by and Sinokor Maritime has begun to capitalize on their huge investment in the segment as daily earnings have moved beyond USD 200k/day,” the brokerage wrote. “The MEG dominates the demand, and the front end of the position list is shrinking by the hour, leaving charterers with few other alternatives to choose from but the South Korean giant.” The brokerage concluded: expect more of the same.

DHT Holdings, a New York-listed VLCC major, addressed the concentration in its latest earnings call without naming Sinokor. “A fundamental shift in fleet ownership is taking place with fleet consolidation by private actors gaining meaningful traction,” DHT said. “We expect the aggregators to soon control at least 25% of the compliant tramping VLCC fleet, a critical market share. This consolidation will likely shift the pricing dynamics and put pressure on timely availability of ships.”

SFL Corporation’s CEO Ole Hjertaker was more direct. “I think one very important underlying factor here on the tanker side, which I would call almost unprecedented in the market, at least in the history I have seen, is that you have one party or group of people who are working together who effectively control around a third of the available or traded tanker VLCC fleet out there,” Hjertaker said on the company’s earnings call, without mentioning names.

The top six VLCC owners now collectively control approximately 300 ships out of a global fleet of 911. That is roughly 30% of all supertankers, according to Allied Shipbroking. The six are: Sinokor (with MSC backing), China Merchants, COSCO, the Fredriksen Group (Frontline), Bahri, and the Angelicoussis Group. When you exclude the approximately 230 VLCCs serving in the shadow fleet, the concentration among mainstream compliant tonnage is even tighter. BRS calculated that the top 10 VLCC owners control 53% of the active mainstream fleet and 59% of mainstream tonnage younger than 20 years.

📊 By the Numbers

📰 Related Coverage:

MSC Buys 50% of Sinokor: The World’s Largest Shipping Company Just Took Control of the Tanker Market (March 2026)

What this means for antitrust, why the FMC has never seen anything like this, and whether one company can legally price a quarter of the world’s crude oil freight market is below.

🔍 Why It Matters

The VLCC spot market has never been this concentrated. And there is no regulatory framework to address it.