While Thousands Of Tankers Sit Trapped Off Iran, One Greek Family Just Made $89 Million In A Single Quarter. One Number Explains How They Did It.

Tsakos Energy Navigation posted its strongest first quarter in years and raised its dividend to a 10-year high. The number behind it is 98.3%.

⚓ The Gosships Team

Gosships Intelligence Is Published At Gosships.com

For Sponsorship And Partnership Inquiries Contact intelligence@gosships.com

|⚓ About Us | 🛢️ Deep Water Reports | 📋 SwiftAction Training |

🏅 Founding Black Gold Membership (*53 Slots Left)

In the first three months of 2026, a Greek family’s tanker company earned $89 million.

That is not revenue. That is profit, after expenses, after interest, after everything. It is 160% more than the company made in the same quarter a year earlier, and it came alongside the highest dividend the company has paid in more than a decade.

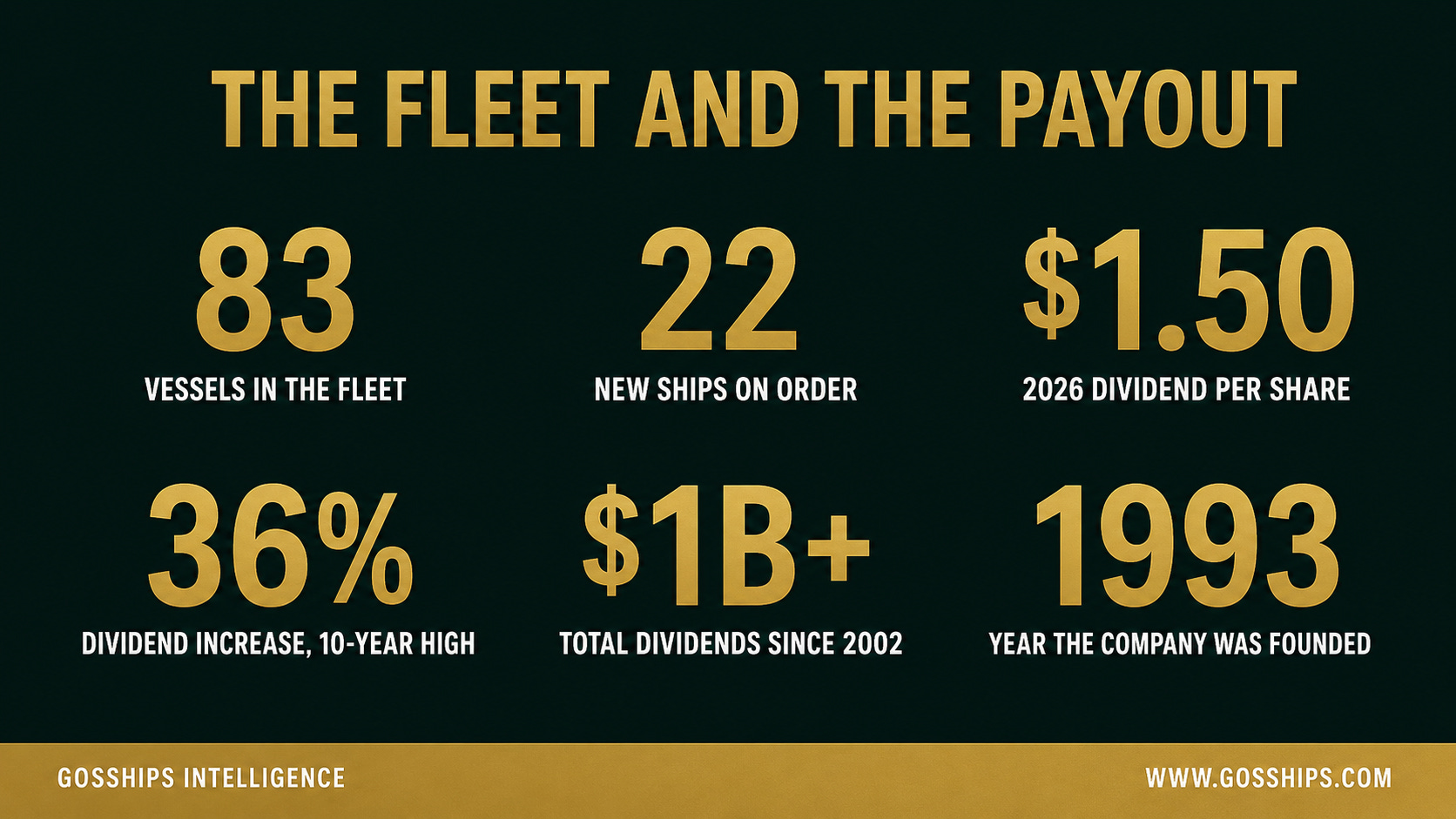

The company is Tsakos Energy Navigation, founded by the late Captain Panagiotis Tsakos in 1993 and still controlled by the Tsakos family. On May 21 it reported a first quarter that, even in a tanker market full of strong numbers, stands out.

There is one figure that explains how a fleet of tankers turns a geopolitical crisis into a record profit, and it is not the headline earnings number. It is 98.3%. Here is what that means, and why it matters for the whole market, sourced entirely from the company’s own earnings release and SEC filing.

📋 In this issue:

🛢️ The Story

📊 By The Numbers

🔍 Why It Matters

👀 What to Watch

🚨 Gosships Signal

📊 Get The Deep Water Report

→ Global Tanker Market Outlook Q2 2026

📋 Competency-Based Maritime Training

→ SwiftAction

📌 Gosships Data Card

→ Net Income: $89.0 Million For Q1 2026, Up 160% From $37.7 Million A Year Earlier Per TEN Q1 2026 Earnings Release

→ Gross Revenue: $253.0 Million, Up From $197.1 Million In Q1 2025 Per TEN

→ Earnings Per Share: $2.72, Up From $1.04 A Year Earlier Per TEN

→ Adjusted EBITDA: $154 Million, Up 55% From $99.3 Million Per TEN

→ Average Fleet Utilization: 98.3%, Up From 97.2% Per TEN

→ Time Charter Equivalent Earnings: $40,960 Per Vessel Per Day, Up From $30,741 Per TEN

🛢️ The Story

Tsakos Energy Navigation, which trades on the New York Stock Exchange under the ticker TEN, is one of the oldest publicly listed shipping companies in the world. It has been public since 2002, and this year marks its 33rd as a listed company. It owns and operates a diversified fleet of crude tankers, product tankers, specialized shuttle tankers, and an LNG carrier, and it is still run by the family of the man who founded it, the late Captain Panagiotis Tsakos.

The Headline Numbers.

For the quarter that ended March 31, 2026, TEN reported gross revenue of $253.0 million, up from $197.1 million in the same quarter of 2025. Operating income reached $110.0 million, nearly double the prior year. Net income attributable to the company was $89.0 million, equating to $2.72 per share, compared with $37.7 million and $1.04 per share a year earlier. The company described it as a 160% increase. Adjusted earnings before interest, taxes, depreciation, and amortization came in at $154 million, up 55%.

On the back of those results, the company declared a semi-annual dividend of $1.00 per share, bringing its total payout for 2026 to $1.50 per share, up from $1.10 in 2025. That is a 36% increase and, according to the company, its highest dividend in more than ten years. Since its NYSE listing in 2002, TEN says it has now distributed more than $1 billion in dividends.

The One Number.

The figure that does the real explanatory work is fleet utilization: 98.3%.

Utilization is the share of a fleet’s available days that are actually spent earning revenue rather than sitting idle, in repair, or waiting for a cargo. A tanker that is not moving cargo is a multi-million-dollar asset burning money. At 98.3%, up from 97.2% a year earlier, almost every vessel in the TEN fleet was earning almost every available day of the quarter.

Pair that with the rate those ships were earning. TEN’s time charter equivalent earnings, the standard measure of daily vessel income, reached $40,960 per vessel per day, up from $30,741 a year earlier. A fleet running at near-full utilization, at rates a third higher than last year, is the entire profit story in two numbers. The ships were almost never idle, and when they worked, they worked for much more.

Why The Market Is This Strong.

In its own commentary, TEN tied the strength to the geopolitical dislocation that has defined 2026. The company noted that with a significant share of the global tanker fleet stranded in the Persian Gulf behind the closed Strait of Hormuz, effective vessel availability has tightened further. Asian and Indian refiners, cut off from their usual Gulf barrels, have been sourcing crude from the Atlantic basin instead, which means longer voyages and more tonne-miles for every cargo. Fewer available ships, longer trips. That is the textbook recipe for a rate surge, and TEN’s quarter is what it looks like on an income statement.

The company also pointed to a coming second-order effect. As more compliant tankers get pulled onto routes previously served by the sanctioned dark fleet, particularly from Venezuela and to some extent Russia, even more compliant capacity is removed from the open market, supporting rates and asset values further.

The balance sheet tells the same story of a company leaning into the moment. TEN’s cash reserves stood at roughly $321 million at the end of the quarter. It has continued to recycle older tonnage at strong prices, generating about $83 million in free cash from the sale of a ten-year-old VLCC in May, while pressing ahead with a newbuilding program that will deliver modern, scrubber-fitted vessels into what management expects to remain a tight market. The strategy is consistent: sell mature ships into a hot asset market, lock long contracts at high rates, and keep a portion of the fleet exposed to the spot market to capture the upside while it lasts.

For the complete rate forecast, fleet supply analysis, and earnings outlook for the listed tanker owners through 2026, see our Global Tanker Market Outlook.

📊 By The Numbers

→ Fleet Size: 83 Vessels, Crude Tankers, Product Tankers, Shuttle Tankers, And LNG, Totaling Roughly 11 Million DWT Per TEN

→ Newbuilding Program: 22 Vessels On Order Totaling 3 Million DWT, Four Already Delivered Per TEN

→ 2026 Dividend: $1.50 Per Share Total, Up From $1.10 In 2025, A 36% Increase Per TEN

→ Dividend Milestone: Highest In More Than 10 Years, Over $1 Billion Distributed Since The 2002 NYSE Listing Per TEN

→ Contracted Revenue Backlog: Approximately $3.6 Billion Per TEN

→ Cash Reserves: Approximately $321.4 Million As Of March 31, 2026 Per TEN

📰 Related Coverage

Greek Shipowners Just Ordered Nearly Half Of Every New Ship On Earth In 2026. One Man Ordered 12 Supertankers.

In 3 Days, 40,000 People Land In Athens For The Most Important Week In Shipping.

Everyone Said The Hormuz Blockade Would Crush Tanker Rates. They Doubled Instead.

Found this useful? Share Gosships Intelligence with a colleague.

How a fleet turns a crisis into a record quarter. Why the dividend matters more than the profit. What the contracted backlog tells you about the next two years. And the one risk that could end the run. Below.

🔍 Why It Matters

A single tanker company’s earnings report is, on its own, a data point. What makes this one worth reading is that it is a clean window into how the entire 2026 tanker market is converting geopolitical chaos into cash, and who is positioned to keep collecting.