A Greek Shipowner Just Raised Her Cash Bid for a US Rival to $24.80 a Share. The Target's Board Will Not Say Yes or No. Everything Now Hangs on One Vote, on June 18.

Diana Shipping sweetened its all-cash offer for Genco on May 27. Genco's board says only that it will review it. Shareholders decide the board itself on June 18.

⚓ The Gosships Team

Gosships Intelligence Is Published At Gosships.com

For Sponsorship And Partnership Inquiries Contact intelligence@gosships.com

|⚓ About Us | 🛢️ Deep Water Reports | 📋 SwiftAction Training |

🏅 Founding Black Gold Membership (*53 Slots Left)

A six-month takeover fight in dry bulk shipping just reached its sharpest point yet, and the next move belongs to a boardroom that has spent half a year saying nothing.

On May 27, Diana Shipping raised its all-cash offer for Genco Shipping & Trading to $24.80 a share, up from $23.50. It is the third time Diana has lifted its price since November, and this time it came with a deadline extension, a draft merger agreement, and a blunt warning about what happens to Genco’s stock if the deal falls apart. Genco’s board responded the same day with a single, carefully worded sentence: it would review and evaluate the revised offer. Not yes. Not no.

That non-answer is the whole story right now. Diana, led by chief executive Semiramis Paliou, has put a fully financed premium on the table and built a second route to victory that does not require the board’s cooperation at all. Genco’s directors have until a single date to decide whether to engage or to let their shareholders decide for them. Here is exactly where the fight stands, what has actually happened, and what the established facts suggest could come next, sourced entirely from Diana Shipping, Genco Shipping & Trading, their securities filings, and named reporting.

A note on why this sits in an oil-shipping publication: this is a dry bulk fight, not a tanker one. But the names are familiar to anyone who follows shipping, and the playbook on display, a determined buyer using a tender offer and a proxy contest to go around a board that will not engage, is sector-agnostic. With tanker asset values high and ownership just as fragmented, the question this fight is testing, whether a resistant board can be forced to the table, is one crude and product tanker owners are watching just as closely.

📋 In this issue:

🛢️ The Story So Far

📊 By The Numbers

🔍 Why It Matters

👀 What Happens Next

🚨 Gosships Signal

📊 Get The Deep Water Report

→ Global Tanker Market Outlook Q2 2026

📋 Competency-Based Maritime Training

→ SwiftAction

📌 Gosships Data Card

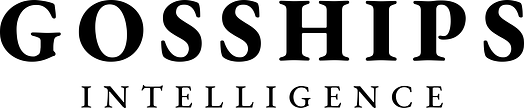

→ The Raised Offer: $24.80 per Share in Cash, Up From $23.50, Announced May 27 per Diana Shipping via GlobeNewswire

→ The Premium: Diana Says the Price is a 39% Premium to Genco’s Undisturbed Pre-Approach Share Price per Diana Shipping

→ The Financing: $1.433 Billion in Fully Committed Financing, Arranged by DNB Carnegie and Nordea per Diana Shipping

→ The Stake: Diana Owns Roughly 14.4% of Genco, Its Largest Shareholder per Diana Shipping via Investing.com

→ The Proxy Fight: Diana Has Nominated Six Independent Directors for Genco’s Board per Diana Shipping

→ The Date: Genco’s Annual Meeting, Where Shareholders Vote on the Board, is June 18 per Diana Shipping

🛢️ The Story So Far

This is a contest between two NYSE-listed dry bulk owners of comparable size, and after six months it has hardened into a test of wills.

The Pursuit.

Diana first approached Genco in November 2025 with a proposal of $20.60 a share. Genco’s board was not interested. Diana raised the offer to $23.50 in March 2026. The board rejected that too, and on May 15 made the rejection formal and unanimous, concluding that the price meaningfully undervalued the company, did not provide an adequate control premium, and was not in shareholders’ interests. Genco pointed to its own net asset value, citing a median analyst estimate of $26.80 a share, well above Diana's price, and said its standalone strategy would deliver more. Its financial advisers, Jefferies and Morgan Stanley, had delivered written opinions on May 13 that the offer was inadequate.

The Raise.

Rather than walk away, Diana escalated. On May 27 it lifted the offer to $24.80 a share, a figure it says represents a 39% premium to Genco’s undisturbed price before the approach and roughly the company’s net asset value at today’s elevated dry bulk asset values. It extended its tender offer deadline to June 26 and delivered a draft merger agreement it said could be finalized in a matter of days if the board would engage. It also issued a warning aimed at shareholders: if the offer is not completed, Diana argued, Genco’s stock could fall back toward roughly $18 as it reverts to its historical trading pattern. Diana’s framing is that the premium exists only because it put it there. Genco’s board sees the same facts differently, arguing the company’s value reflects its own strategy and a strengthening market, not Diana’s presence.

The Board’s Position.

Genco’s board confirmed the same day that it had received the revised offer and would carefully review and evaluate it, consistent with its fiduciary duties. It did not accept, and it did not reject. The board’s case, made repeatedly over the prior six months, is that Diana has been trying to buy Genco at a discount to what the company is worth: it has pointed to a median analyst net asset value estimate of $26.80 a share, above Diana’s price, cited fairness opinions from Jefferies and Morgan Stanley that earlier offers were inadequate, and argued its own strategy will deliver more value to shareholders than a sale. The board has even suggested that, with its balance sheet, Genco would be the more logical acquirer. From the board’s vantage, refusing to engage on what it views as low offers is not entrenchment but fiduciary diligence in a rising market where waiting could be worth more.

The Second Path.

The reason the board’s answer may not be the final word is the structure Diana has built. Over months, Diana acquired roughly 14.4% of Genco’s shares on the open market, stopping just beneath the 15% threshold that would trigger Genco’s shareholder rights plan, the defensive measure known as a poison pill. It took its offer directly to shareholders through a tender offer, letting them sell at $24.80 if they choose, regardless of the board’s recommendation. And it nominated six directors it describes as independent, none affiliated with Diana, to stand for election to Genco’s board. Genco characterizes those same nominees as handpicked and aligned with Diana’s interests rather than shareholders’. Diana also lined up a buyer in advance: a definitive agreement to sell 16 of Genco’s vessels to Star Bulk Carriers for $470.5 million the moment any acquisition closes. The structure gives shareholders, rather than the board alone, a direct say in the outcome.

📊 By The Numbers

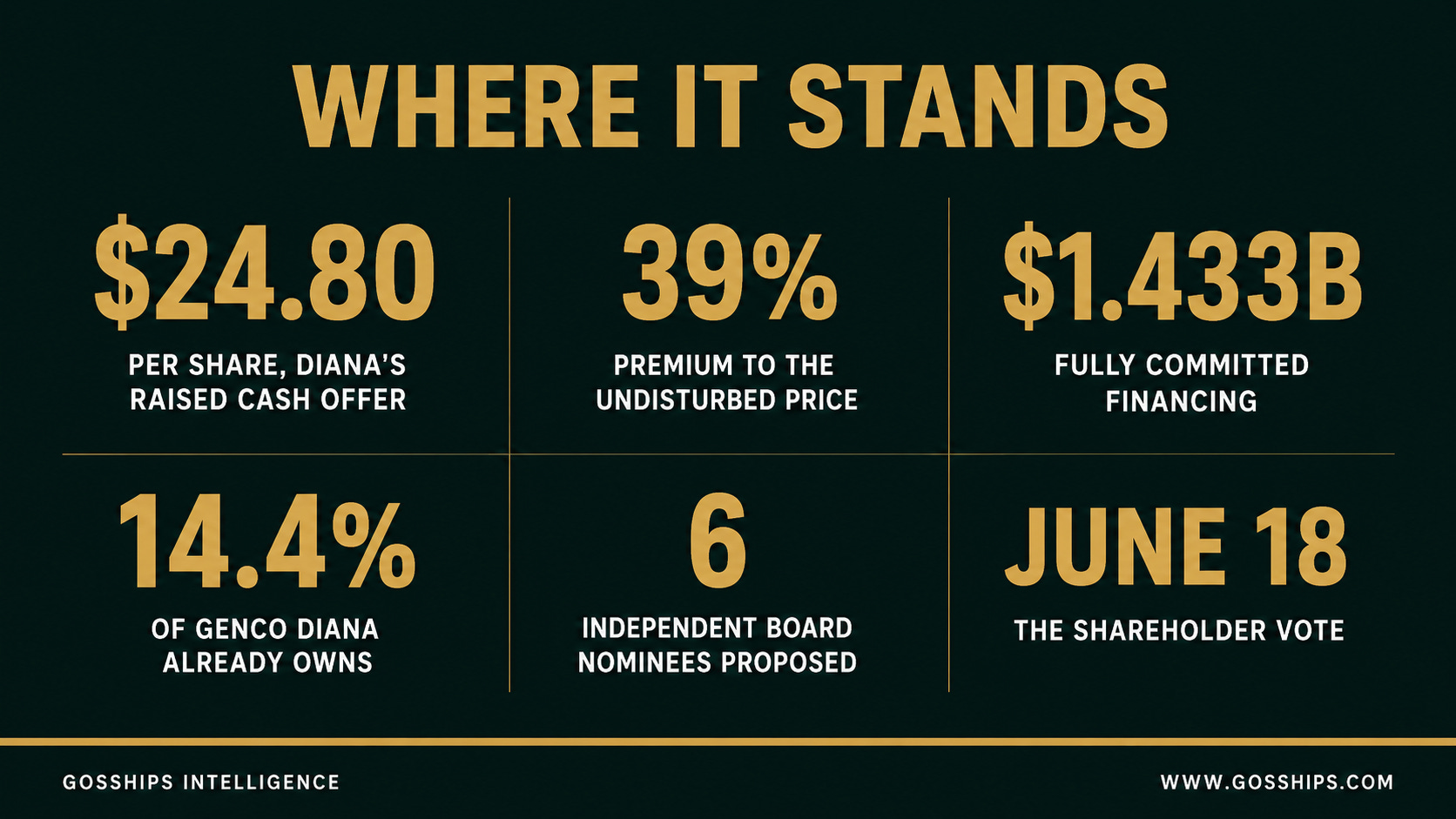

→ First Offer: Diana Proposed $20.60 per Share on November 24, 2025 per Diana Shipping via Quiver Quantitative

→ Genco’s Counterpoint: Genco’s Board Cites a Median Analyst NAV Estimate of $26.80 per IndexBox Citing Genco

→ Tender Deadline: Diana’s Tender Offer Now Expires June 26, Extended From June 2 per Diana Shipping

→ The Side Deal: Diana Agreed to Sell 16 Genco Vessels to Star Bulk for $470.5 Million on Completion per Diana Shipping

→ Diana’s Warning: Diana Says Genco Shares Could Fall Toward $18 if the Deal is Not Completed per Diana Shipping

→ The Combination: A Merger Would Create a Dry Bulk Owner of 80 or More Vessels per IndexBox

📰 Related Coverage

Hormuz Shut Down: Three Tankers Hit, P&I Clubs Pull War Risk Cover as Iran War Escalates

Iran Built a Toll Booth on the Strait of Hormuz

Trump Gave Iran 48 Hours to Open Hormuz

Found this useful? Share Gosships Intelligence with a colleague.

What the board’s silence actually means. Why the 15% line and the June dates decide everything. The three ways this can break from here, each grounded in what has already happened. Below.

🔍 Why It Matters

This is no longer a disagreement about price alone. It has become a governance contest, and the structure Diana has built makes it one of the clearer real-time tests of whether a determined buyer can force a deal on a board that does not want one.