MSC’s Tanker Strategy Is Bigger Than Sinokor. They Have Three More Plays Running In Parallel. Combined Capital: $5 Billion. This Is The Largest Tanker Market Entry In Modern Maritime History.

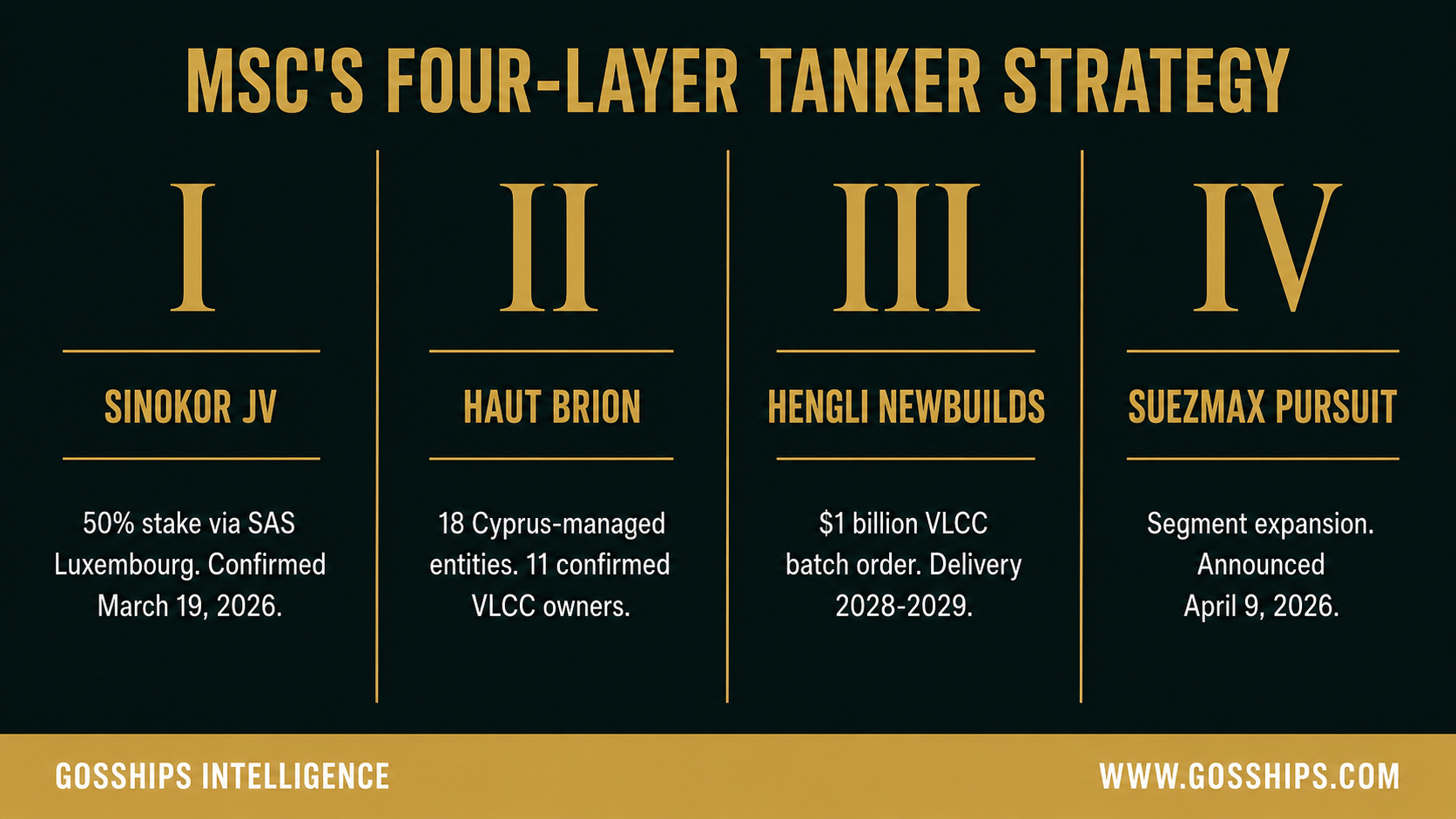

Sinokor JV. Direct VLCC ownership through Cyprus. A $1 billion Hengli newbuild order. A Suezmax pursuit. Aponte is building a tanker major.

⚓ The Gosships Team

Gosships Intelligence Is Published At Gosships.com

For Sponsorship And Partnership Inquiries Contact intelligence@gosships.com

|⚓ About Us | 🛢️ Deep Water Reports | 📋 SwiftAction Training |

🏅 Founding Black Gold Membership (*53 Slots Left)

MSC has committed approximately $5 billion to the tanker market. Most of the industry thinks that money went to Sinokor.

That money went to four parallel destinations. Sinokor is one.

The second is direct VLCC ownership through 18 Cyprus-managed entities incorporated in Panama in late December 2025, of which 11 are confirmed VLCC owners per Forbes. The third is a $1 billion VLCC newbuild order at Hengli Heavy Industry in China, confirmed by TradeWinds on April 9. The fourth is a Suezmax tanker order being set up at the same yard, reported the same day.

The Sinokor joint venture was the only one with a public press release. The other three were assembled in parallel, through different corporate vehicles, across different yards, and have been reported in isolation by the trade press without anyone connecting the four pieces.

Combined fleet position: approximately 150 VLCCs through ownership, charter, and newbuild contracts.

This is not a partnership. This is a strategy. The world’s largest container shipping company has just executed the largest tanker market entry by a container shipping group in modern maritime history, and the four pieces only make sense when viewed together.

Here is the full picture, sourced entirely from public regulatory filings, named shipbroker estimates, and the trade press that has been covering each piece in isolation.

📋 In this issue:

🛢️ The Story

📊 By The Numbers

🔍 Why It Matters

👀 What to Watch

🚨 Gosships Signal

📊 Get The Deep Water Report

→ Global Tanker Market Outlook Q2 2026

📋 Competency-Based Maritime Training

→ SwiftAction

📌 Gosships Data Card

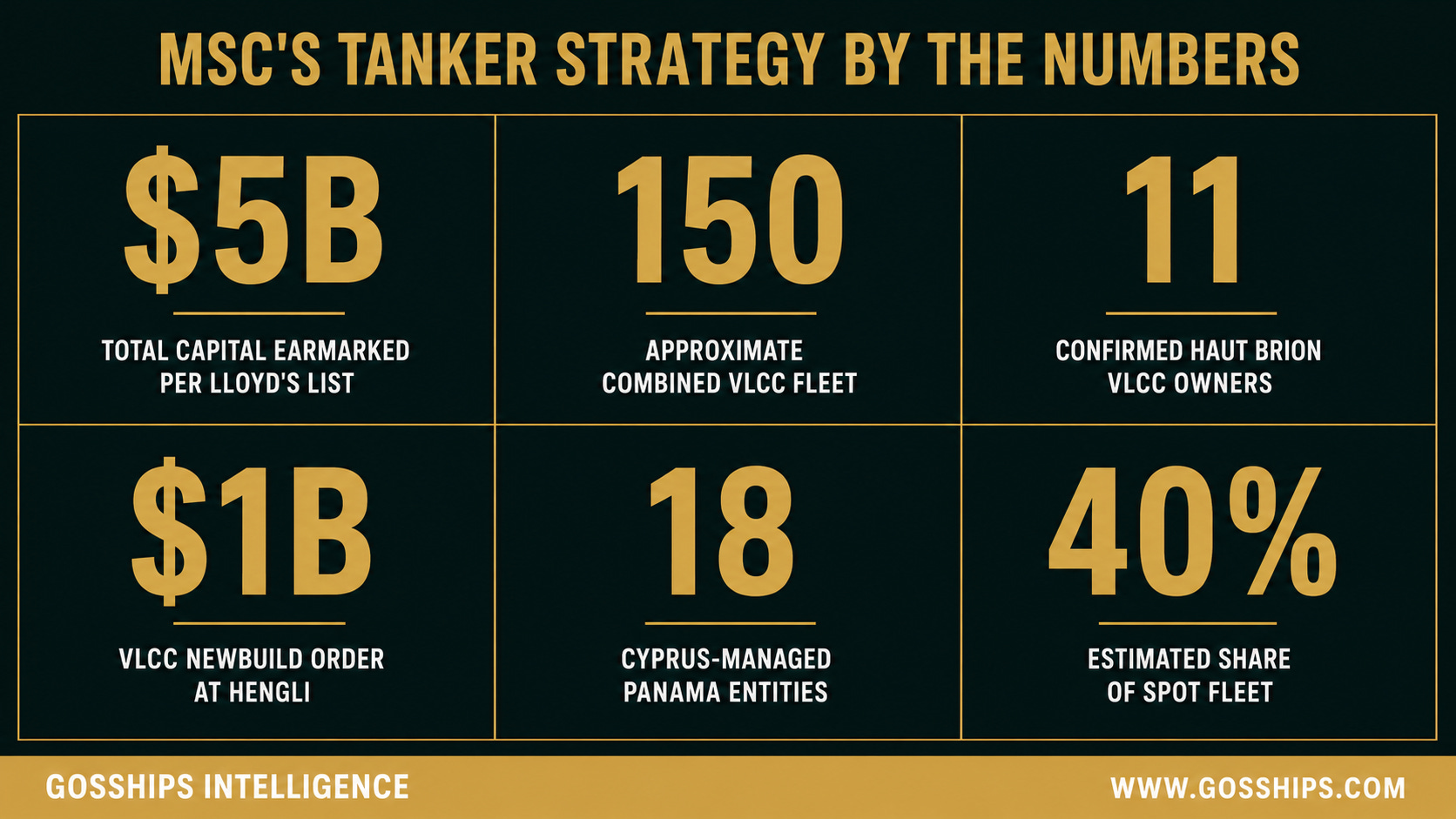

→ Total Capital Earmarked: Approximately $5 Billion Per Lloyd’s List January 28, 2026

→ Layer One: 50% Stake In Sinokor Via SAS Shipping Luxembourg Per Cyprus And Greek Antitrust Filings March 19

→ Sinokor Combined Fleet: Approximately 118 VLCCs Through Ownership And Time Charter Per BRS Shipbrokers Via Riviera Maritime

→ Layer Two: 18 Panama Entities Named Haut Brion 1-18 Incorporated December 24-26, 2025 Per Forbes Investigation

→ Haut Brion Direct VLCC Ownership Confirmed: 11 Vessels Worth Over $900 Million Per Veson Nautical Via Forbes

→ Haut Brion Cyprus Address: MSC Shipmanagement Limited Per Forbes Equasis Records

→ 20 Additional Vessels Registered In Liberia Worth Over $820 Million, Ultimate Ownership Unverifiable Per Forbes

→ Layer Three: VLCC Newbuild Order At Hengli Heavy Industry Worth Approximately $1 Billion Per TradeWinds April 9, 2026

→ Hengli Existing MSC Relationship: At Least 20 LNG-Fuelled Megamax Containerships Contracted 2024-2025 Per Lloyd’s List

→ Layer Four: Suezmax Tanker Order Pursuit At Hengli Per TradeWinds April 9, 2026

→ Capital Deployment Estimate: $900 Million+ Confirmed Haut Brion Plus $820 Million+ Unverified Liberia Plus $1 Billion Hengli Newbuild Plus Forthcoming Suezmax

→ Combined VLCC Fleet Position: 130-150 Vessels Per Bloomberg Via iMarine

→ Combined Fleet Market Share: 14-17% Of Global VLCC Fleet Per Cyprus Shipping News

→ Combined Spot Market Share: Approximately 24-40% Of Compliant VLCC Spot Fleet Per Signal Ocean And Bloomberg

→ Gianluigi Aponte Net Worth: Approximately $44.5 Billion Per Forbes 2026

→ Status: Largest Tanker Market Entry By A Container Shipping Group In Modern Maritime History

🛢️ The Story

MSC’s tanker strategy is the largest horizontal diversification any container shipping group has ever attempted into crude oil transportation.

The strategy has four parts. The trade press has covered each one in isolation. Lloyd’s List broke the funding story on January 28. Forbes mapped the Cyprus-managed entities in March. The Cyprus and Greek competition authorities confirmed the Sinokor joint venture on March 19. TradeWinds confirmed the Hengli newbuild order on April 9. Each piece has been reported. The four pieces have not been put together.

Together, they represent approximately $5 billion in capital, approximately 150 VLCCs through ownership, charter, and newbuild contracts, and the only example in modern maritime history of a container shipping company moving directly into VLCC market leadership.

Layer One: The Sinokor Joint Venture.

On February 2, 2026, MSC signed an investment framework agreement with Ga-Hyun Chung, the founder of South Korea’s Sinokor Maritime, to acquire a 50% stake in Sinokor through MSC’s Luxembourg subsidiary SAS Shipping Agencies Services. The deal was filed with the Cyprus Commission for the Protection of Competition on February 25 and published by the Hellenic Competition Commission on March 13. Public confirmation came March 19, according to Bloomberg, Splash247, and TradeWinds. The filings explicitly refer to “joint control” of Sinokor by MSC and Chung.

Sinokor had already executed the largest single-operator VLCC buying spree in modern history before the JV was formalized. In the opening weeks of 2026, Sinokor acquired 35 of 45 VLCCs sold globally, absorbing 78% of all transaction volume, according to Veson Nautical via Forbes. By March, $3.3 billion had changed hands for at least 60 tankers, according to Veson Nautical. BRS Shipbrokers, the Paris-based broker, calculated that Sinokor controls approximately 118 VLCCs through ownership or time charter, representing 13% of the total active VLCC fleet and 16% of the mainstream non-sanctioned fleet. “There has never previously been a single operator with such a dominant share of the active fleet,” BRS noted via Riviera Maritime. Fearnleys called Sinokor the “kingpin” of the VLCC trades.

Layer Two: Direct Ownership Through Haut Brion.

Running parallel to the Sinokor JV is a direct fleet acquisition track through 18 Panama-incorporated entities named Haut Brion 1 through Haut Brion 18. All 18 entities were incorporated between December 24 and December 26, 2025, in a 72-hour window, according to Forbes corporate records research via Equasis. The named president of all 18 entities is Mario Aponte, cousin of MSC founder Gianluigi Aponte, who has held various roles at MSC over the years. The registered address Mario Aponte provided for the entities in Cyprus matches the address of MSC Shipmanagement Limited, the MSC division responsible for vessel management.

Eleven of the 18 Haut Brion entities are confirmed as owners of VLCCs that collectively cost more than $900 million, according to Veson Nautical via Forbes. The remaining seven entities have not been linked to specific vessels in public records. A further 20 VLCCs purchased during the same spree are registered in Liberia, where corporate records are not public, making confirmation of ultimate ownership impossible through Equasis. The Liberian vessels collectively cost more than $820 million.

This is direct fleet ownership, separate from Sinokor ownership. The vessels are commercially managed by Sinokor in many cases, but the equity sits with MSC-linked Panama entities for the confirmed 11. Forbes summarized the structure: if all Haut Brion entities are MSC-owned, Aponte personally controls more than half of every Sinokor-linked VLCC purchased since December.

A specific example of the pattern was reported by Reuters on April 12, 2026, via gCaptain: the VLCC Mombasa B, formerly Front Forth and previously part of John Fredriksen-controlled Frontline’s January 8 divestiture, is now owned by Haut Brion 8 SA at the Cyprus address shared with Sinokor’s manager.

Layer Three: The Hengli Newbuild Pipeline.

On January 29, 2026, TradeWinds reported that Gianluigi Aponte was setting up “a huge VLCC newbuilding order” at Hengli Heavy Industry, the rapidly expanding Chinese shipyard in Dalian. Lloyd's List also reported on January 28 that MSC was being linked to a new order for eight VLCC newbuildings at the same yard. MSC is already an existing Hengli client. The yard holds contracts for at least 20 LNG-fuelled megamax containerships placed by MSC in 2024 and 2025.

On April 9, 2026, TradeWinds confirmed the order under the headline “Aponte targets suezmax tanker order after booking $1bn VLCC batch.” The $1 billion VLCC batch is now in the Hengli orderbook. Hengli has become the largest shipyard in China by order volume, with 174 orders worth $16 billion received over the past year, according to VesselsValue via Splash247. VLCCs represent 31% of Hengli’s en bloc orders.

This is forward fleet building, separate from the secondhand market activity. Newbuild VLCCs ordered at Hengli today will deliver across 2028 and 2029, extending MSC’s tanker position well beyond the current cycle.

Layer Four: The Suezmax Pursuit.

The same April 9 TradeWinds report disclosed that Aponte is now targeting a Suezmax tanker order at Hengli. The Suezmax pursuit mirrors the segment expansion playbook that Sinokor itself executed on March 24, when Sinokor purchased its first three Suezmaxes after cornering the VLCC market. Splash247 reported that brokers expect “an avalanche of suezmax purchases by the aggressive Korean player.” The same dynamic is now being attempted by MSC directly.

The Suezmax move is the most recent layer, less than six weeks old as of mid-May. It demonstrates that the MSC tanker strategy is not a one-segment play. The capital being deployed across the four layers indicates a multi-segment crude transportation strategy, executed through multiple corporate vehicles, across multiple yards, over multiple delivery windows.

The Capital Picture.

Lloyd’s List reported on January 28 that Aponte had “earmarked up to $5 billion for a massive tanker play.” One executive with direct knowledge of the funding told Lloyd’s List bluntly: “It’s Aponte’s money.” The capital is being deployed across four channels: secondhand VLCC acquisition through Haut Brion (over $900 million confirmed across the 11 verified Panama entities, with another $820 million in Liberian registrations of uncertain ultimate ownership), the Sinokor JV (financial terms not disclosed), the $1 billion VLCC newbuild batch at Hengli, and the Suezmax pursuit.

Bloomberg estimates that the combined MSC-Sinokor entity will ultimately control approximately 150 VLCCs, representing roughly 40% of the available unsanctioned spot fleet. Signal Ocean has projected that Sinokor independently controls at least 24% of the global compliant VLCC spot fleet. The four-layer strategy is what makes those numbers possible.

For the complete rate forecast and fleet supply analysis showing how MSC’s four-layer position affects VLCC and Suezmax rates through 2028, see our Global Tanker Market Outlook.

📊 By The Numbers

→ $5 Billion Capital Earmarked For Tanker Play Per Lloyd’s List

→ $3.3 Billion Spent On Secondhand VLCC Acquisitions By March 2026 Per Veson Nautical Via Forbes

→ $900 Million+ Confirmed Direct Ownership Through 11 Haut Brion Panama Entities Per Veson Nautical Via Forbes

→ $820 Million+ Worth Of 20 Additional Vessels In Liberian Registry, Ultimate Ownership Unverifiable Per Forbes

→ $1 Billion VLCC Newbuild Batch Order At Hengli Heavy Industry Per TradeWinds April 9

→ 18 Panama Entities Named Haut Brion 1-18 Incorporated December 24-26, 2025 Per Forbes

→ 11 Haut Brion Entities Confirmed Headed By Mario Aponte Per Forbes Corporate Records

→ 50% Sinokor Stake Acquired Via SAS Shipping Luxembourg Per Cyprus And Greek Antitrust Filings

→ 130-150 Combined VLCCs Through Ownership And Time Charter Per Bloomberg Via iMarine

→ 24% Of Compliant VLCC Spot Fleet Controlled By Sinokor Alone Per Signal Ocean

→ 40% Of Available Unsanctioned Spot Fleet Estimated For Combined Entity Per Bloomberg

→ 20 LNG-Fuelled Megamax Containerships Already On Order At Hengli By MSC Per Lloyd’s List

→ 174 Total Orders At Hengli Worth $16 Billion Over Past Year Per VesselsValue Via Splash247

→ $44.5 Billion Gianluigi Aponte Net Worth Per Forbes 2026

📰 Related Coverage

Sinokor Is Charging $20 Per Barrel To Ship Oil. Last Year It Was $2.50. They Control 40% of Available Tankers. Nobody Can Do Anything About It.

MSC × Sinokor: 40% of the World’s Available Supertankers. $3.3 Billion. Zero Antitrust Investigations. Now It’s Official.

Sinokor Cornered the VLCC Market. Now They Just Bought Their First Three Suezmaxes. Brokers Expect an Avalanche.

What the four layers add up to for VLCC and Suezmax market structure through 2028. Why MSC’s tanker entry breaks every historical precedent for container shipping diversification. How the Hengli yard relationship makes the strategy possible. And which segment is most likely to be the next layer. Below.

🔍 Why It Matters

No container shipping company in modern maritime history has executed a tanker market entry at this scale, through this many parallel structures, with this concentration of yard relationships and operational platforms.