Shipping Oil Out of the Persian Gulf Now Costs Three Times What It Does From West Africa. The Only Question Left Is Whether It Lasts

By late May, Arabian Gulf to China earnings were running about three times West Africa to China, even as rates everywhere else slid toward oversupply.

⚓ The Gosships Team

Gosships Intelligence Is Published At Gosships.com

For Sponsorship And Partnership Inquiries Contact intelligence@gosships.com

|⚓ About Us | 🛢️ Exclusive Report | 📋 SwiftAction Training |

🏅Black Gold Membership (*53 Slots Left)

Shipping a barrel of crude out of the Persian Gulf now costs roughly three times what it costs to move one out of West Africa. That gap did not exist in January. It opened the day the Strait of Hormuz stopped working normally, and it has quietly become the single most important number in the tanker market. Every barrel that still leaves the Gulf carries a war premium stacked on top of the oil itself, and because crude is priced globally, a sliver of that premium reaches the pump whether you fill up in Shanghai or St. Louis.

📋 In this issue:

🛢️ The Story

📊 By The Numbers

🔍 Why It Matters

👀 What to Watch

🚨 Gosships Signal

🔔 Not Yet Subscribed? Gosships Intelligence Delivers Oil Shipping Intelligence. Subscribe For Free!

📊 Order Our Exclusive Report

→ Global Tanker Market Outlook Q3 2026 Edition

📋 Competency-Based Maritime Training

→ SwiftAction

📌 Gosships Data Card

→ Early January 2026: A Middle East To China Supertanker Earned About $29,000 A Day

→ February 26: The Same Route Hit $206,141 A Day, The Highest Since April 2020

→ February 28: The United States And Israel Struck Iran, And Iran Restricted The Strait Of Hormuz

→ Early March: War Risk Cover Was Pulled And The Benchmark Hit A Record $423,736 A Day

→ Late May: Arabian Gulf To China Earnings Ran About Three Times West Africa To China

→ The Seven Days To June 2: Only Three Laden Supertankers Crossed The Strait Of Hormuz

🛢️ The Story

There is one number that explains the entire tanker market right now, and it is not a headline rate. It is a gap.

In its June 2 bi-weekly report, Breakwave Advisors found that by the end of May, earnings for very large crude carriers on the Arabian Gulf to China route were running roughly three times those on the West Africa to China route, and above the US Gulf to China route as well. Breakwave called it a regional dislocation that “remains extraordinary by historical standards.” In the same report, the firm noted that VLCC earnings excluding the Arabian Gulf had fallen below $100,000 a day for the first time in nineteen weeks. The two facts sit side by side: the Atlantic is cooling toward oversupply, and the Gulf is not. The distance between them is the story.

That distance is new. According to Signal Group’s weekly tanker market monitor, a Middle East Gulf to China voyage was earning around $29,000 a day at the start of January, a seasonal low. Then the geopolitics took over. As traders accelerated charters ahead of a possible confrontation between Washington and Tehran, the benchmark Middle East to China rate, known as TD3, climbed to W218.52, or $206,141 a day, on February 26, the highest since April 2020 and nearly quadruple the level at the start of the year, according to LSEG data reported by Reuters and Baird Maritime. South Korean operator Sinokor’s supertanker buying spree, industry sources told Reuters, added further support.

Then came the shock. The United States and Israel struck Iran on February 28, according to Argus, and Iran retaliated by severely restricting navigation through the Strait of Hormuz. More than 700 vessels were caught inside the Gulf. Marine war risk providers began scrapping cover for ships operating in the Persian Gulf, CNBC reported on March 3, and on the same day the Middle East to China benchmark hit a record $423,736 a day, up more than 94 percent in a single session, an all time high at the time according to CNBC citing LSEG data.

To understand why a freight rate can do that, look at what flows through the strait. In a normal year the Strait of Hormuz carries about 20 million barrels a day of crude and refined products, roughly one fifth of the oil the world consumes and somewhere between a quarter and a third of all seaborne oil trade, according to the International Energy Agency and the US Energy Information Administration. There is no alternative seaway out of the Gulf. When it constricts, the effect is immediate. The EIA’s Global Energy Security Data report found that flows through Hormuz fell almost 30 percent year on year in the first quarter of 2026, to 14.6 million barrels a day, down from 20.4 million a year earlier, a loss of close to 6 million barrels a day attributed to the conflict with Iran. Kpler vessel tracking showed transits through the strait down roughly 92 percent from the week before the conflict, with close to 22 percent of the world tanker fleet caught up in the disruption. By early May, Lloyd’s List, citing Vortexa, reported that the strait had been shut in all but name for 71 days running and that global crude volumes carried on VLCCs had fallen about 36 percent versus prewar levels.

Months later, it still has not reopened in any normal sense. Breakwave’s June 2 report counted only three laden VLCCs transiting the strait in the previous seven days, carrying an estimated 6 million barrels, against roughly 105 million in a normal week. Ships are moving, but barely, and only with help. CNBC reported on June 4 that around 40 previously stranded vessels had exited Hormuz over the prior three weeks by quietly coordinating with the US Navy, with owners submitting transit plans to the Naval Cooperation and Guidance for Shipping group in Bahrain, after President Trump abruptly shut down a short lived escort mission the month before. Secretary of State Marco Rubio said the United States was responding to Iranian attacks on commercial ships. Traffic, CNBC noted, remains far below prewar levels.

That is the machinery behind the gap. A supertanker loading in the Atlantic basin sails into a market that is lengthening and softening, with adequate ships and limited fresh demand. A supertanker loading in the Arabian Gulf sails into a war zone with a shrinking pool of willing tonnage, thinner insurance, and a transit that now depends on coordination with one navy or another. The first earns less than $100,000 a day. The second earns about three times more. Same vessel, same cargo, different water.

To see how unusual that is, rewind to before the strike. In the last full week of January, Baltic Exchange data put the Middle East Gulf to China round voyage at about $112,000 a day, West Africa to China at about $101,000, and the US Gulf to China at just under $93,500. The three biggest loading regions were earning within roughly twenty percent of one another. That is what a normal market looks like, because a supertanker is fungible and can sail wherever the cargo is, so rates across regions tend to converge. A threefold gap between the Gulf and West Africa is not an ordinary spread widening. It is the market pricing one region as a war zone and the rest of the world on ordinary supply and demand.

The market has, in effect, split in two. And the freight premium attached to that split is what every broker, trader, and refiner is now trying to price. Whether it holds, where the next dollar of risk gets added, and what it means for the books of the people who charter these ships, is where this gets interesting.

📊 By The Numbers

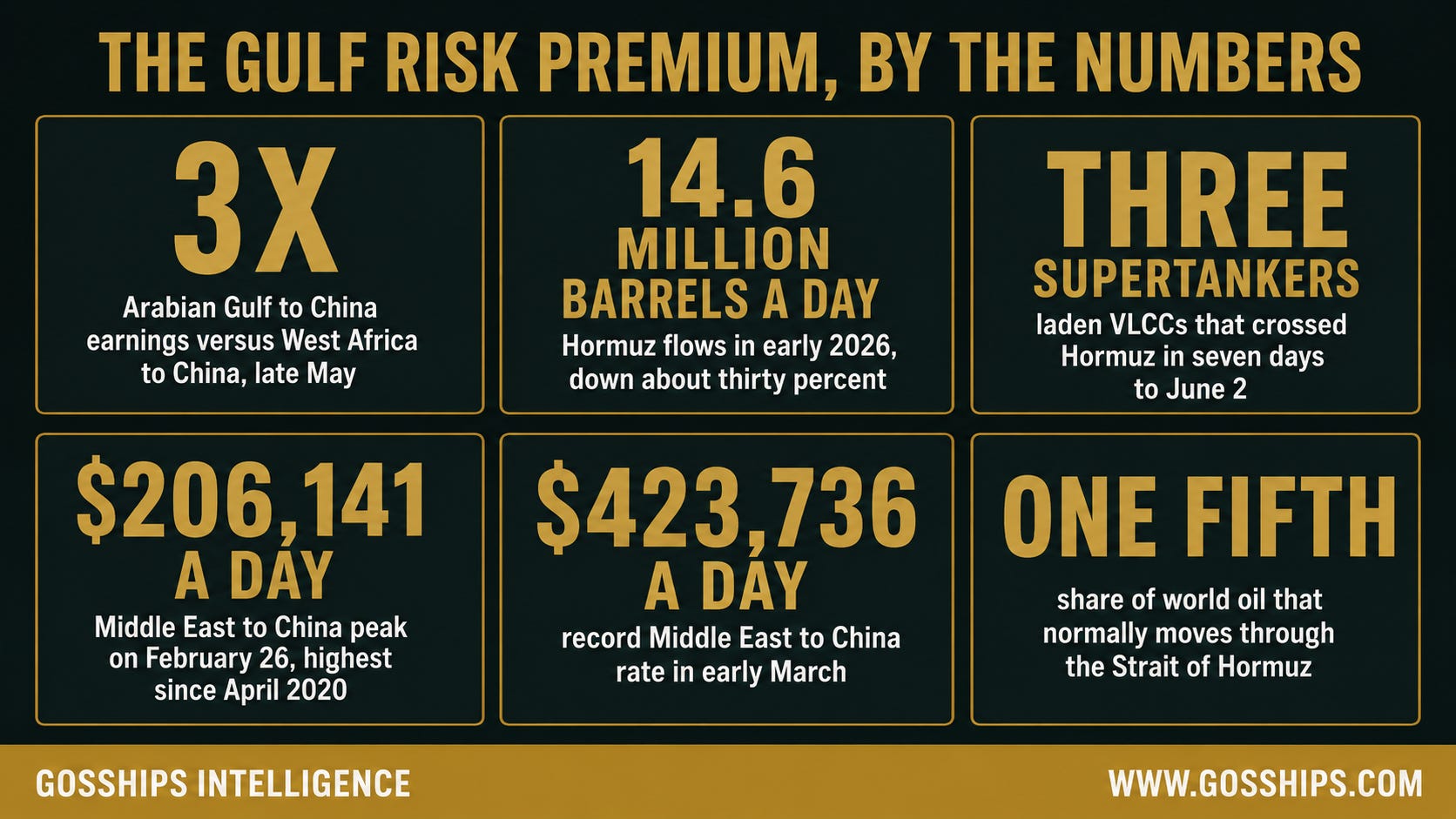

→ Three Times: Arabian Gulf To China VLCC Earnings Versus West Africa To China In Late May (Breakwave Advisors, June 2)

→ 14.6 Million Barrels A Day: Hormuz Flows In Q1 2026, Down About 30 Percent Year On Year (EIA)

→ Three Laden Supertankers: VLCCs That Crossed Hormuz In The Seven Days To June 2 (Breakwave Advisors)

→ $206,141 A Day: The Middle East To China Peak On February 26, Highest Since April 2020 (LSEG Via Reuters)

→ $423,736 A Day: The Record Middle East To China Rate In Early March (CNBC, LSEG Data)

→ About One Fifth: The Share Of World Oil That Normally Moves Through The Strait Of Hormuz (IEA, EIA)

Related Coverage

The Insurance Market Closed The Strait Of Hormuz Before Iran Did. Here Is What VLCC Rates Reveal.

Sinokor Is Charging $20 Per Barrel to Ship Oil. Last Year It Was $2.50. They Control 40% of Available Tankers. Nobody Can Do Anything About It.

MSC, COSCO, HMM and Other Container Giants Are Quietly Building Crude Tanker Fleets. What’s the Strategy?

The gap is the easy part to see. The harder part is what sits underneath it: who is paying the premium, whether the people earning it can keep earning it, and what happens to the whole market the day Hormuz reopens. There is also a quieter signal buried in the same data that suggests this dislocation is more fragile than it looks, and that the next move may not be up. That analysis, and what we are watching to call the turn, is below.

🔍 Why It Matters

The dislocation is not a single market doing something strange. It is two markets that have stopped behaving like one, and each audience that touches tankers is exposed to the split differently.