Vitol’s CEO Said the War Would Erase a Billion Barrels. Trackers Say Iran Just Shipped 50 Million in Two Weeks. Who’s Right?

Russell Hardy put the loss at 600 to 700 million barrels by late April. TankerTrackers.com counts 1.66 million per day in June. Both can be true.

⚓ The Gosships Team

Gosships Intelligence Is Published At Gosships.com

For Sponsorship And Partnership Inquiries Contact intelligence@gosships.com

|⚓ About Us | 🛢️ Exclusive Report | 📋 SwiftAction Training |

🏅Black Gold Membership (*53 Slots Left)

Vitol lost hundreds of millions of dollars in the opening weeks of the war and still told its banks it made roughly $2 billion for the quarter. Then its chief executive spent the spring telling the world how much oil the war had destroyed, and peace arrived before his numbers stopped climbing. The world’s largest independent energy trader now has the most expensive question in the market sitting on its books: how much of the damage was permanent, and how fast does the barrel count heal?

📋 In This Issue:

🛢️ The Story

📊 By The Numbers

🔍 Why It Matters

👀 What To Watch

🚨 Gosships Signal

🔔 Not Subscribed? Gosships Intelligence Delivers Oil Shipping Intelligence. Subscribe Here!

📊 Order Our Exclusive Report

→ Global Tanker Market Outlook Q3 2026 Edition

📋 Competency-Based Maritime Training

→ SwiftAction

📌 Gosships Data Card

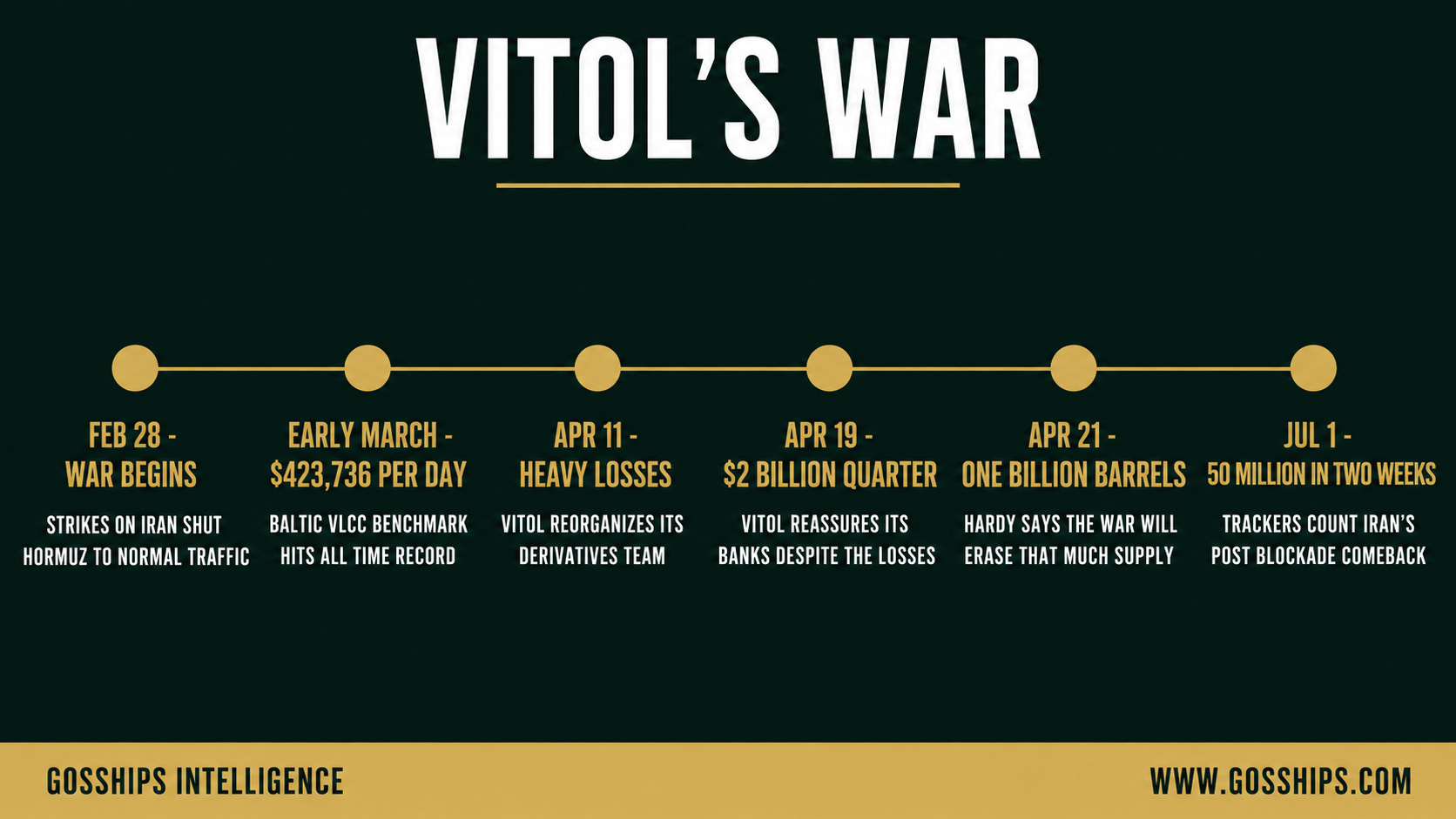

→ Feb 28: US and Israeli strikes on Iran begin, effectively closing the Strait of Hormuz to normal tanker traffic (US Energy Information Administration, Short Term Energy Outlook)

→ Early March: The Baltic Exchange TD3C VLCC benchmark spikes 94 percent from the prior Friday to a record $423,736 per day (Baltic Exchange data, reported by Seatrade Maritime)

→ April 11: Bloomberg reports Vitol is reorganizing its derivatives team after mark to market losses estimated in the hundreds of millions of dollars

→ April 19: Vitol tells its banks it made roughly $2 billion in the first quarter despite the war losses (Bloomberg)

→ April 21: CEO Russell Hardy tells the FT Commodities Global Summit the war will erase at least one billion barrels of supply, with 600 to 700 million already lost (Financial Times summit remarks, reported by Dawn and Investing.com)

→ July 1: TankerTrackers.com estimates Iran has shipped 50 million barrels in the two weeks since the US blockade lifted (CNBC)

🛢️ The Story

Vitol’s war began with its own book bleeding. In the opening days of the conflict, the world’s largest independent energy trader was positioned for a market that no longer existed: its derivatives desk held bets that diesel would outperform jet fuel and that Dubai crude would trade at a discount to Brent, according to Bloomberg’s April 11 reporting. When United States and Israeli strikes on Iran on February 28 triggered the effective closure of the Strait of Hormuz, with the US Energy Information Administration recording shipping traffic as extremely limited from that date, both positions inverted violently. Jet fuel and Middle East crude were suddenly the scarcest molecules on the planet, and the closure sent Dubai crude and jet fuel prices sharply higher, per Bloomberg’s reporting on the episode.

The damage was severe enough that Vitol restructured around it. Bloomberg reported on April 11 that the firm was reorganizing its London based derivatives operation after mark to market losses that people familiar with the matter put in the hundreds of millions of dollars, with star trader Yaoyao Liu caught on the wrong side of the moves, some traders expected to leave, and others folded back into physical desks focused on individual markets. For a firm built on reading dislocation, the message was blunt: the war had beaten the house’s own forecast.

What happened next is why Vitol is Vitol. Eight days later, on April 19, Bloomberg reported that the group had told banks it made roughly $2 billion in profit for the first quarter anyway, a figure communicated in part to reassure lenders watching the derivatives losses. The physical machine, about 8 million barrels per day of traded energy in 2025 on the company’s own numbers, had absorbed a nine figure trading hit and still produced one of the strongest quarters in the industry. For scale: Vitol earned about $4.5 billion for all of 2025, its fourth best year ever, after $15 billion in 2022, $13 billion in 2023 and around $8 billion in 2024, according to Reuters figures compiled by Global Banking and Finance Review.

The quarter was not free money. It was survived money. In the first weeks of the war, Vitol, Trafigura and Gunvor all went to their banks for fresh liquidity as margin calls exploded across energy derivatives, with Bloomberg reporting on March 10 that the top traders lined up around $7 billion in new credit to weather the turmoil. The tanker side of the same dislocation was just as violent: the Baltic Exchange’s TD3C VLCC benchmark hit a record $423,736 per day in early March, per Baltic Exchange data reported by Seatrade Maritime, and every barrel that did move east moved at war prices.

Then Vitol’s chief executive started publishing the war’s invoice. Speaking at the Financial Times Commodities Global Summit in Lausanne on April 21, Russell Hardy said the conflict had already cost the market 600 to 700 million barrels of supply and would erase at least one billion barrels before it was over, remarks reported by the Financial Times, Dawn and Investing.com. He paired it with a structural warning: refining capacity had been damaged in ways that would take months to repair even if the fighting stopped.

The numbers kept growing as the war ground on. In remarks reported by Argus Media, Hardy put global demand destruction at about 4 million barrels per day against supply losses of around 12 million barrels per day, with global refinery output down roughly 6 million barrels per day from pre war levels. And he flagged the quiet crisis inside the loud one: “By the time this is over, we will have lost 300mn-400mn bl of product inventories,” Hardy said, per Argus. Crude gets headlines. The diesel, jet fuel and gasoline that vanished from tanks around the world is the hole that takes longest to refill.

On June 17, the war Hardy was pricing officially began to end. Donald Trump and Iranian president Masoud Pezeshkian signed a 14 point framework, the American signature applied at a Versailles dinner and the Iranian one in Tehran, reopening the strait to commercial traffic without tolls for 60 days and suspending the blockade that had frozen Iranian exports, per NBC News.

What followed was an export sprint. Bloomberg reported on June 20 that Kharg Island loadings had resumed after a halt of about six weeks. By June 30, United Against Nuclear Iran’s shipping update counted 15 laden tankers in the Kharg anchorage and a VLCC loading roughly 2 million barrels at the Azarpad jetty. TankerTrackers.com estimates Iran shipped 50 million barrels of crude in the two weeks after the blockade lifted, a June average of 1.66 million barrels per day, per CNBC’s July 1 reporting. Iran’s parliament speaker Mohammad Bagher Ghalibaf claims the country is now selling at prices roughly 20 percent higher than before the war, a figure from a senior regime official that should be read as such. Brent, meanwhile, changed hands near $73 per barrel on July 1, per CNBC, almost 40 percent below its $118 April peak.

So here is the collision. The CEO of the world’s largest independent energy trader spent April describing a market that had structurally lost a billion barrels, months of refining capacity, and 300 to 400 million barrels of product inventories. Ten weeks later, the country at the center of the war is loading two million barrel cargoes off Kharg Island and flat price has surrendered most of the war premium. A hostile reader would say Hardy overcalled it. A careful reader would notice the two claims do not actually touch: the barrels lost between February 28 and June 17 are gone regardless of how fast Iran loads today, the refining damage does not repair on a signature, and an inventory hole measured in the hundreds of millions of barrels is a restocking program measured in years of tanker voyages, not weeks.

That last point is the forward story, and it is the reason the trader who lost the first round of this war may own the next one. Product inventories do not swim home. They move on LR2s, MRs and clean tankers, chartered by exactly the firms that spent the war building the deepest real time map of where the holes are. Kpler’s July 1 read of Hormuz traffic pointed to what the firm called “continued operational continuity, but not a settled return to normal routing,” per RFE/RL, and the diplomacy whipsawed inside the same day: CNBC reported a breakdown in US and Iran talks in the morning, indirect talks then resumed in Doha with Qatar reporting positive progress, per CNN, and Axios reported Washington is now trying to talk Tehran out of charging tolls once the free window ends. The 60 day toll free window expires in mid August. Every restocking decision in the market is being made against that clock.

Which of Hardy’s numbers survives the peace, what a 300 to 400 million barrel product hole does to clean tanker demand, who funds the refill, and the signals that will show whether Vitol is positioning for the rebound it publicly described: all of it is below.

Related Coverage

Tanker Supercycle 2026: Why Geopolitical Disruption Is Absorbing Global Tonnage

The US Blockade Crushed Iran’s Oil Exports to a Six-Year Low. Then Trump Signed a Deal at Versailles, and the Tankers Are Already Sailing Again. Who Won?

Sinokor Is Charging $20 Per Barrel to Ship Oil. Last Year It Was $2.50. They Control 40% of Available Tankers. Nobody Can Do Anything About It.

📊 By The Numbers