A 10-Year-Old VLCC Just Crossed $100 Million, a Decade High. The Strait of Hormuz Reopened, Then Iran Shut It Again Two Days Later. How Long Can the Record Hold?

The record rests on a wartime freight spike that only holds while Hormuz stays shut. The oldest, least efficient ships rose fastest of all, and a record delivery wave is already on the way.

⚓ The Gosships Team

Gosships Intelligence Is Published At Gosships.com

For Sponsorship And Partnership Inquiries Contact intelligence@gosships.com

|⚓ About Us | 🛢️ Exclusive Report | 📋 SwiftAction Training |

🏅Black Gold Membership (*53 Slots Left)

The secondhand price of a VLCC is the most honest forecast in oil shipping, and for 48 hours in June it nearly broke. A 10-year-old VLCC that sold for about $74 million in 2023 crossed $100 million this spring, a decade high, according to Breakwave Advisors in their March 2, 2026 analysis "VLCC second-hand prices at decade highs." The oldest, least efficient hulls appreciated fastest, and the age discount that separates a 10-year-old VLCC from a 5-year-old one narrowed from 25% in 2023 to closer to 20%. Every dollar of that record was underwritten by one thing: a freight spike that paid VLCCs more than $200,000 a day on the Middle East Gulf-to-China route because the Strait of Hormuz was closed. On June 18, under a United States-Iran agreement, the strait reopened, tankers poured back through, and for two days the entire foundation under those record prices looked like it was about to give way. Then, on June 20, Iran declared Hormuz shut again. By June 27, the strait was effectively closed once more, roughly five ships a day against a normal ninety-plus. Then, on June 28, Iran's foreign minister, Abbas Araghchi, declared that Hormuz would remain under total Iranian control for the next 30 days, its full capacity restored only on Iran's terms. The war premium is back on, and so is the decade-high price of a 10-year-old ship. But every owner holding one just watched the floor disappear and reappear inside a single week, and Iran has now put a 30-day clock on the rest. The question is no longer whether the reckoning comes. It is whether the record can survive the day the strait finally stays open.

📋 In This Issue:

🛢️ The Story

📊 By The Numbers

🔍 Why It Matters

👀 What To Watch

🚨 Gosships Signal

🔔 Not Yet Subscribed? Gosships Intelligence Delivers Oil Shipping Intelligence. Subscribe Here!

📊 Order Our Exclusive Report

→ Global Tanker Market Outlook Q3 2026 Edition

📋 Competency-Based Maritime Training

→ SwiftAction

📌 Gosships Data Card

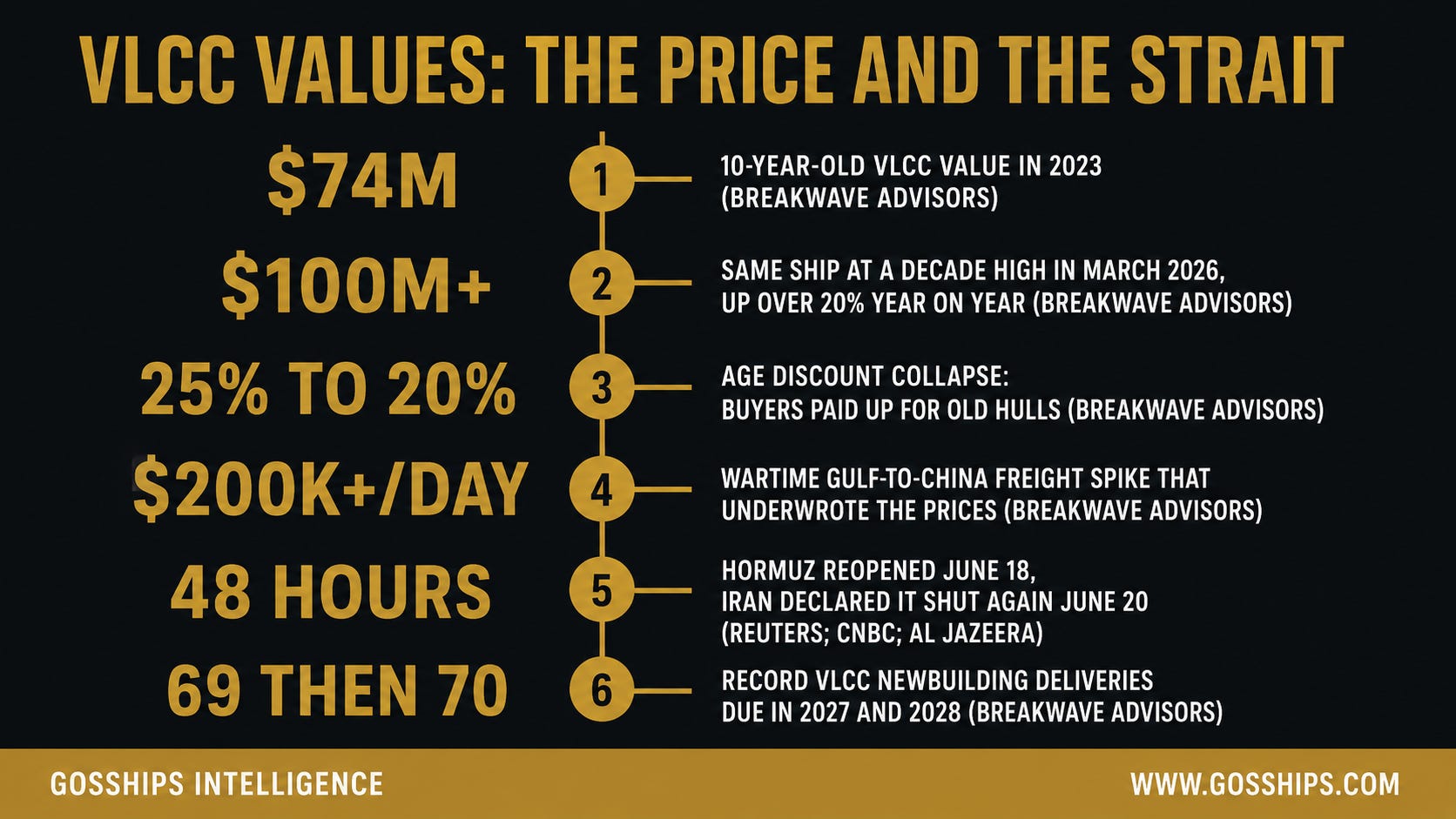

→ $74M - 10-year-old VLCC value in 2023 (Breakwave Advisors)

→ $100M+ - The same ship at a decade high in March 2026, up more than 20% year on year (Breakwave Advisors, March 2, 2026)

→ 25% to 20% - The age discount collapse, as buyers paid up for old hulls and stopped discriminating on age (Breakwave Advisors)

→ $200K+/day - The wartime Gulf-to-China freight spike that underwrote the record values (Breakwave Advisors)

→ 48 hours - How long the Strait of Hormuz stayed reopened on June 18 before Iran declared it shut again on June 20 (Reuters; CNBC; Al Jazeera)

→ 69 then 70 - Record VLCC newbuilding deliveries scheduled for 2027 and 2028, the supply wave behind the prices (Breakwave Advisors)

Sources: Breakwave Advisors, “VLCC second-hand prices at decade highs,” March 2, 2026; Reuters; CNBC; Al Jazeera, June 2026.

🛢️ The Story

In shipping, asset prices tell you what the market believed at the moment money changed hands. When owners bid the secondhand price of a VLCC to a decade high, they were making a levered bet that freight rates would stay high long enough and tight supply would persist long enough to justify what they paid. When they bid up old ships alongside new ones, they made a second and more pointed bet: that scarcity had become so severe that age, efficiency, and cargo flexibility no longer justified the discount they used to command. That is exactly what happened in the VLCC secondhand market through the first half of 2026. The numbers confirmed it with unusual clarity. Then, in a single week of June, the market got a live demonstration of exactly how fragile the bet had become.

Start with how far prices ran. Breakwave Advisors stated on March 2, 2026 that VLCC asset prices had reached decade highs. The firm documented that a 10-year-old VLCC valued at about $74 million in 2023 had risen above $100 million, a year-on-year increase exceeding 20%. The five-year appreciation on that same vessel class was more than 130%. A 5-year-old VLCC that traded at approximately $98 million in February 2023 was fetching above $120 million, a year-on-year rise of around 17% and a five-year gain of nearly 99%. These were not incremental moves. They represented a fundamental repricing of what a VLCC was worth in a world where the fleet was stretched, freight was strong, and available tonnage was increasingly divided between two very different markets.

Those March 2026 figures were the most current broker anchor, but not the only snapshot. Lloyd’s List reported in December 2025, in “Fleet supply and freight rates drive crude tanker values higher,” that average values of 10-year-old VLCCs had reached $88 million while 5-year-old ships were around $118 million, up approximately 4% since the summer of 2025, with 15-year-old vessels up about 8% since August 2025. Those were a separate broker-sourced snapshot from December 2025, and the Breakwave Advisors figures from March 2026 were a later point on the same rising curve. They were not contradictory. They were sequential. The $88 million 10-year-old in December 2025 became the above-$100 million 10-year-old by March 2026 as the market kept climbing.

The engine under that climb was the freight market, and this is the part that the June whipsaw put directly in play. Breakwave Advisors confirmed in their March 2, 2026 analysis that strong cash generation and improved freight visibility had pushed asset values sharply higher, not only for modern units but also for overaged units. The Time Charter Equivalent for VLCCs on the Middle East Gulf-to-China route surged past $200,000 per day in early March 2026, according to Breakwave Advisors, a year-on-year increase of over 440%, with spot earnings at six-year highs. When a vessel is generating $200,000 per day, the calculation on whether to pay $100 million for it changes entirely. At that earnings rate, a buyer could theoretically recover the purchase price in less than two years of full employment, and that arithmetic made almost any price look defensible. But that $200,000 per day was not a normal market. It was a war premium. The Strait of Hormuz had been blocked by Iran since the United States-Israel air campaign began on February 28, 2026, Gulf crude was forced onto longer and more constrained routes, and the resulting scramble for tonnage is what drove rates to six-year highs in the first place.

The second chapter of the run-up was fleet supply, and it is the one that explained the age discount collapsing. Lloyd’s List reported in December 2025 that while headline fleet numbers were rising due to newbuilding deliveries, a growing portion of VLCCs and Suezmaxes were engaged in sanctioned or shadow fleet trades, effectively removing them from mainstream commercial activity. Real supply in the spot market remained constrained, Lloyd’s List concluded. S&P Global similarly confirmed that shadow tanker operators had been actively buying old ships while scrapping the oldest, a pattern of fleet renewal that keeps vintage tonnage circulating rather than going to the breakers. Breakwave Advisors, citing the Signal Ocean Platform, documented that spot supply on the key Arabian Gulf VLCC route had fallen to one of the lowest levels recorded in the first two months of the year, with the vessel count dropping 27% week on week by early March. In a market that tight, owners and charterers could not afford to discriminate by age. The 25% age discount that Breakwave Advisors documented for a 10-year-old versus a 5-year-old in 2023 narrowed to closer to 20%, because the alternative for a charterer who could not find a modern vessel was no vessel at all.

Then came June, and the market saw its own future flash in front of it. On June 17, the United States and Iran signed a memorandum of understanding. On June 18, the United States Navy lifted its blockade and the Strait of Hormuz reopened to commercial traffic, with Iran allowing transits toll-free for an initial period. The response was immediate. According to CNBC, at least 20 oil tankers crossed Hormuz in the first days, traffic that Kpler described as broadly balanced between westbound and eastbound crossings. For 48 hours, the war premium that had carried VLCC earnings to six-year highs and the Gulf-to-China Time Charter Equivalent past $200,000 per day had a credible expiry date. Every owner holding a ship bought at the top was, for two days, staring at the precise scenario that ends the rally: Hormuz open, Gulf crude back on its short routes, the tonnage scramble over.

It did not last. On June 20, Iran declared the Strait of Hormuz closed again and moved to reinstate its toll and clearance regime, even as Iran’s foreign ministry insisted shipping was operating normally, a contradiction that itself tells you how unstable the situation is. Al Jazeera reported on June 22 that shipping had stalled after Iran declared the waterway shut. By June 27, transits had collapsed back to roughly five ships in a day against a normal flow of more than ninety. The strait that had reopened for two days was effectively closed again within a week. The war premium snapped back on, and with it the freight environment that underwrites a decade-high price for a 10-year-old ship.

On June 28, Iran’s foreign minister, Abbas Araghchi, removed any remaining ambiguity. The Strait of Hormuz, he said, would remain under the total oversight and management of Iran for the next 30 days, its full capacity restored only after Iran’s conditions were met, with no other state holding authority over the waterway. For the VLCC market, that single declaration did two things at once. It guaranteed the war premium stays on for at least another month, which supports the decade-high values in the immediate term. And it put Iran’s own clock on the precise event that would end them, the day the strait finally stays open. The buyers who paid the top were always betting that scarcity outlasts a reopening. They are now, whether they intended to or not, also betting on the calendar Tehran set on June 28.

Here is why that 48-hour window matters more than the re-closure that followed it. Secondhand values lag freight. Xclusiv Shipbrokers has noted that a peak in secondhand tanker prices typically lags the peak in time-charter rates, because the sale-and-purchase market reprices slowly and deliberately. The same lag works on the way down. Through 2024 and 2025, the market repeatedly showed that even sharp moves in freight produced only marginal, delayed movement in vessel prices, and that old tonnage in particular proved unusually resilient, propped by shadow-fleet demand for any hull that floats and can load crude. So the decade highs documented in March are almost certainly still close to decade highs today, even after the June scare, because the screen does not move in 48 hours. What the reopening proved is not that the values have fallen. It is that the single event that would make them fall, a durable opening of Hormuz, is now a live, demonstrated possibility rather than a distant tail risk. The market has seen the exit. It just has not been forced to use it yet.

And the exit sits on top of a second pressure that was always coming. Breakwave Advisors documented that 48 VLCC newbuildings were expected to deliver in 2026, rising to 69 in 2027 and peaking at 70 in 2028, before falling to 24 in 2029 and just 6 in 2030. Those 2027 and 2028 numbers, 139 ships in two years, represent roughly 20% of the active, compliant VLCC fleet. Drewry has already flagged that record secondhand tanker prices look stretched and questioned their sustainability. A record delivery wave landing into a market whose freight is hostage to a single contested chokepoint is the textbook setup for a correction in asset values, and the ships most exposed are the ones that rose the most: the old hulls whose appreciation was always the purest expression of scarcity rather than quality.

The sale-and-purchase market split into two distinct tiers during the run-up, and that structure determines who is exposed now. Lloyd’s List, S&P Global, and trade press from early 2026 collectively described a market in which established shipowners competed intensely for modern, scrubber-fitted ECO units, while a parallel and equally active market emerged for older, vintage tonnage that attracted opportunistic buyers and shadow-fleet operators. The two markets run on different calculations. Modern ECO VLCCs fitted with scrubbers can burn cheaper high-sulfur fuel oil while remaining compliant with the International Maritime Organization’s sulfur cap, a fuel-cost advantage worth thousands of dollars per day. At a fuel spread of $200 per tonne between high-sulfur and low-sulfur bunkers, that advantage reaches roughly $15,000 per day, according to Pacific Green Marine Technologies, and at $300 per tonne it can reach approximately $23,000 per day. A modern buyer paying a record price is at least buying a structural earnings edge. A buyer of vintage tonnage is buying something else: a hull that floats, a flag that asks few questions, and a residual-risk price that depended on the freight spike staying high. If Hormuz stays open one day, the modern tier has the fuel-economics floor under it. The vintage tier has the shadow-fleet bid, and little else.

The most dramatic illustration of how far the peak ran is the inversion at the top of the market. By May 2026, trade reporting confirmed that 5-year-old VLCCs were trading above the price of a newbuilding contract. Seatrade Maritime reported that a 5-year-old VLCC then cost about $9 million more than ordering a new vessel, and some brokers put the premium on prompt resales far higher, with near-new resales changing hands around $168 million against a newbuilding price near $128.5 million. That is a market that has lost its normal depreciation logic. A ship that has already consumed years of its useful life was selling at a premium to a vessel that does not yet exist, purely because owners valued prompt availability and trusted that freight would stay strong. That premium is the single cleanest barometer of the peak. If confidence in the freight rally fades, the newbuild premium is the first number that should compress, and watching it erode will tell you the correction has started before the broker valuations catch up.

None of this means the values must fall, and honest analysis has to state the bull case. Asset values are sticky and they lag, so owners have a real window to sell at or near the highs before any correction lands. The compliant, mainstream fleet is genuinely smaller than headline tonnage figures suggest, because sanctions policy and shadow trades have locked up a large slice of it, and that structural scarcity does not reverse the moment one chokepoint reopens. Shadow-fleet operators have shown they will keep buying old ships regardless of the spot market, which puts a floor under the vintage tier that did not exist in prior cycles. And tonne-mile demand from Chinese and Indian crude imports, much of it now sourced from the Atlantic Basin on long-haul routes, could absorb a meaningful share of the 2027 and 2028 deliveries. The bet that the buyers paying above $100 million for a 10-year-old ship are making is that this structural scarcity outlasts any opening of Hormuz. The June reopening tested that bet for 48 hours. Iran’s re-closure handed it back. Whether it survives the next opening is the only question that matters.

The clearest way to read the secondhand VLCC market at the end of June 2026 is as a price suspended over a switch that Iran controls. The decade highs are real and, because values lag, still on the screen. The freight that justifies them is real and, because Hormuz is shut again, still being paid. But the market has now watched that freight nearly evaporate in a single weekend and come back only because a deal fell apart. Every owner holding a ship bought at the top is a forced participant in a question they cannot answer: how durable is a record price built on a strait that opened and closed inside the same week? The age discount, which collapsed fastest on the way up, is the number most likely to move first on the way down, because the scarcity premium on old hulls is the least defensible once tonnage loosens. The buyers made their bet at the peak. Hormuz has shown it can reopen. The secondhand price is the scoreboard, and for the first time in two years it has been forced to look at the exit. The deeper analysis of what that means for each participant in the tanker market is below.

Related Coverage

Oil Just Crashed Below $75, on Track for Its Worst Week in Months as Hormuz Reopens. Is the Record Tanker Boom Already Unwinding?

Iran’s Revolutionary Guard Says It Just Closed the Strait of Hormuz. Iran’s Own Government Says It’s Open.

Owners Just Ordered Tankers at the Fastest Pace in History, yet Effective Supply Will Grow Just 1% Over Three Years. Where Did the Fleet Go?

📊 By The Numbers