Owners Just Ordered Tankers at the Fastest Pace in History, yet Effective Supply Will Grow Just 1% Over Three Years. Where Did the Fleet Go?

A record orderbook and a near-record aging fleet are colliding in slow motion. The tanker boom everyone is counting on may already be spoken for before the first new hull lands.

⚓ The Gosships Team

Gosships Intelligence Is Published At Gosships.com

For Sponsorship And Partnership Inquiries Contact intelligence@gosships.com

|⚓ About Us | 🛢️ Exclusive Report | 📋 SwiftAction Training |

🏅Black Gold Membership (*53 Slots Left)

The tanker industry just ordered crude tankers faster than in any quarter on record, and somehow the fleet is barely growing. The orderbook has ballooned to a 17-year high, BIMCO reports, and Kpler counts 419 tankers due for delivery in 2026 alone, a record year by number. But VLCC specialist Tankers International looked at the same data and arrived at a number that should stop every shipowner, analyst, and charterer cold: effective vessel supply growth of just 1% over the next three years. The gap between those two facts, a record wave of new orders and a nearly flat effective fleet, is the most important story in the tanker market right now, and it is hiding in plain sight. The reason it matters is straightforward. Freight rates are set by the fleet that can actually sail, not the one on paper, and almost the entire market is watching the wrong number.

📋 In This Issue:

🛢️ The Story

📊 By The Numbers

🔍 Why It Matters

👀 What To Watch

🚨 Gosships Signal

🔔 Not Yet Subscribed? Gosships Intelligence Delivers Oil Shipping Intelligence. Subscribe Here!

📊 Order Our Exclusive Report

→ Global Tanker Market Outlook Q3 2026 Edition

📋 Competency-Based Maritime Training

→ SwiftAction

📌 Gosships Data Card

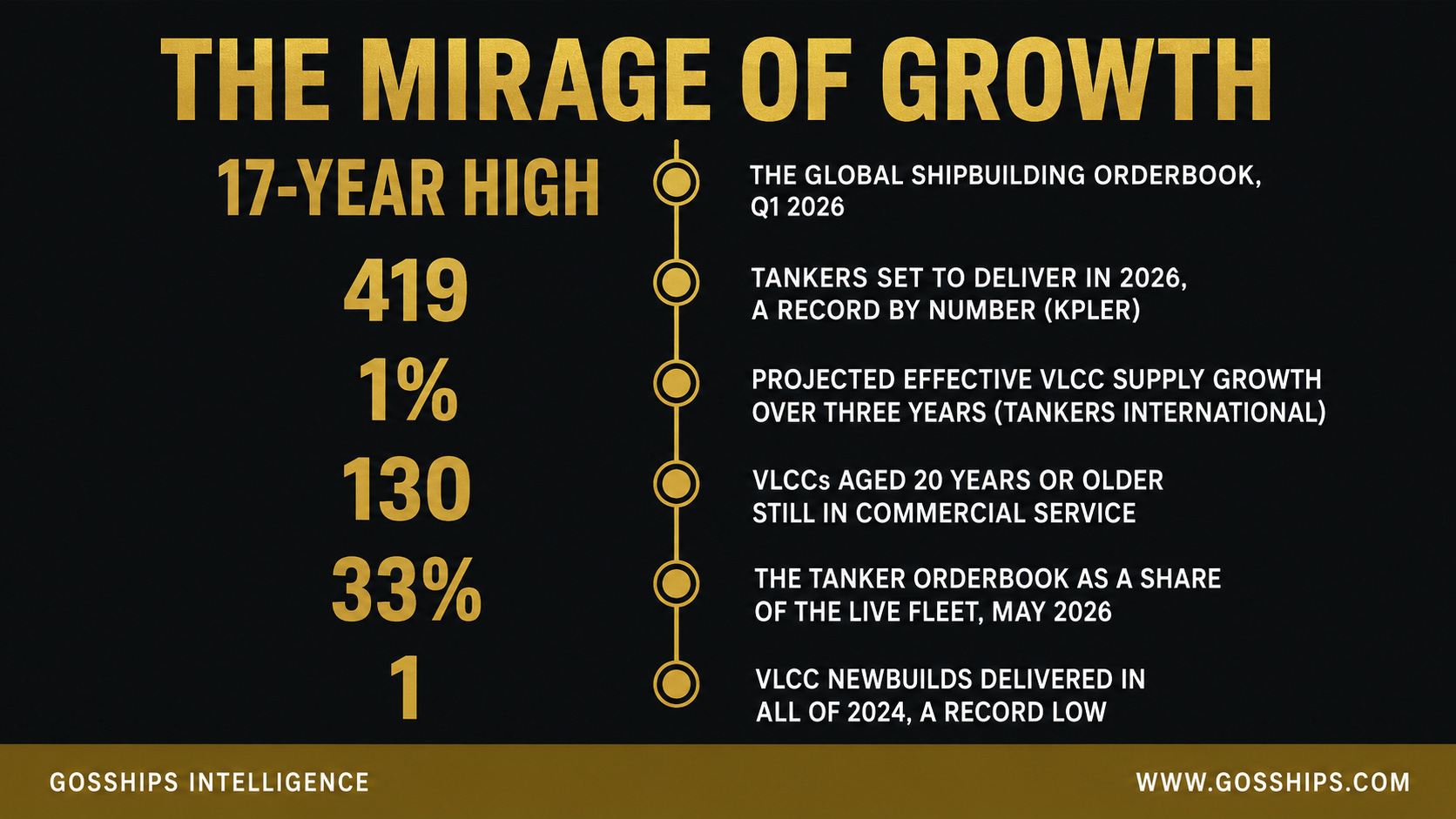

→ 17-YEAR HIGH - The global shipbuilding orderbook as of Q1 2026 (BIMCO)

→ 419 - Tankers set to deliver in 2026, a record by number (Kpler)

→ 1% - Projected effective VLCC supply growth over three years (Tankers International)

→ 130 - VLCCs aged 20 years or older still in commercial service (Tankers International)

→ 33% - The tanker orderbook as a share of the live fleet, May 2026 (VesselsValue / Hellenic Shipping News)

→ 1 - VLCC newbuilds delivered in all of 2024, a record low (Tankers International)

Sources: BIMCO; Kpler; Tankers International; VesselsValue / Hellenic Shipping News.

🛢️ The Story

The tanker industry just set a record. Then it set another one. Then a third. The trouble is that the records are not all pointing in the same direction.

BIMCO reported in April 2026 that the first quarter of the year produced the highest quarterly crude-tanker contracting in recorded history, pushing the global shipbuilding orderbook to a 17-year high, measured as a proportion of the global fleet. Kpler counted 419 tankers from intermediates to VLCCs expected to deliver in 2026 alone, a 52-percent jump from the 247 that delivered in 2025 and a record year for fleet growth in raw numbers. The tanker orderbook as a share of the live fleet climbed from about 15 percent in May 2025 to about 33 percent in May 2026, according to VesselsValue data cited by Hellenic Shipping News. For VLCCs specifically, Clarksons put the orderbook at roughly 30 percent of the existing fleet, a staggering shift for a segment that had been widely described as under-ordered for years.

On the screen those numbers look like a supply flood in the making. Every analyst, every charterer, every shipbroker can read them. The market has been ordering at this pace partly because everyone can see the same aging fleet and the same geopolitical pressure on trade routes, and partly because a run of historically strong freight rates has handed shipowners the cash to act. The orderbook is real. The deliveries are coming.

What Tankers International did was look at the other side of the ledger. The VLCC specialist published its analysis in April 2025, and the headline conclusion, which gCaptain reported under the phrase “mirage of growth,” has not aged out of relevance: Tankers International projects effective vessel supply growth of only 1 percent over the next three years. The nominal fleet, measured by the number of hulls, is projected to grow by about 8 percent as roughly 70 new VLCCs deliver. But 8 percent nominal and 1 percent effective are very different things, and the gap between them is the story.

The reason is the fleet that already exists. Tankers International counts approximately 130 VLCCs aged 20 years or older still in commercial operation, a number that has risen from fewer than 20 just five years ago. Eighteen to 20 years was, for most of the industry’s modern history, the window in which a supertanker was retired. The ship lost its major classification society approvals, its operating costs climbed, its fuel efficiency deteriorated, and the major oil company terminal operators stopped accepting it. That was the lifecycle. Tankers International reports that VLCCs aged up to 25 years are now remaining in commercial operation, a full half-decade beyond the traditional endpoint.

They are staying because the market has needed them. The geopolitical disruptions of the last several years, the shadow fleet that absorbed sanctioned Russian and Iranian cargoes, the long-haul rerouting after the Red Sea crisis, have kept even the oldest, least efficient hulls earning enough to justify their operating costs. The shadow fleet created a new ecosystem for old tankers that would otherwise have been scrapped, and that ecosystem has bent the retirement curve in ways that the nominal orderbook cannot capture.

The result is a fleet that is aging faster than it is renewing. New hulls are arriving, but they are not straightforwardly adding to effective capacity. Each new VLCC that delivers is partly replacing the declining output of the aged vessels already in service. An aging tanker does not simply stop working on its twenty-fifth birthday. It degrades gradually: slower speeds, more unplanned maintenance, more days in port, more frequent inspections, lower cargo utilization. Tankers International’s methodology accounts for these real-world reductions in output, and when it does, the 8 percent nominal growth in hull count becomes 1 percent effective growth in actual capacity to carry crude.

The delivery drought that preceded this order wave made things worse. Tankers International reports that only a single VLCC was delivered in all of 2024, a record-low figure for a segment that has traditionally received about 40 newbuilds per year. A trickle of five VLCCs was expected in 2025, per Tankers International, while Kpler’s January 2026 forecast put 2025 at eight deliveries. In 2026 the flow is set to rise to approximately 30 VLCC deliveries, according to Tankers International, or about 38 by Kpler’s count, but that is still below the historical average of roughly 40 per year that Tankers International cites. Years of under-ordering followed by one historic quarter of over-ordering does not straightforwardly fix a fleet that has been running on borrowed time.

BIMCO, whose analysis of the orderbook is among the most closely watched in the industry, framed the moment precisely. Filipe Gouveia, BIMCO’s Shipping Analysis Manager, was quoted by gCaptain as noting that the surge in contracting had been building across the 2020s and most recently accelerated to the highest quarterly level in history, but that the swelling orderbook across several large shipping sectors could also contribute to a slowdown in contracting as owners absorb the implications of what they have already committed.

That second part of the BIMCO observation is the one fewer people are talking about. The order frenzy of 2026 is also building tomorrow’s delivery pressure. The ships being contracted today at record quarterly volumes will begin arriving in earnest in 2027 and 2028. The Tankers International “mirage” projection is based on the 2025 fleet profile and the delivery schedule then known. As the orderbook has expanded further in the months since, the delivery wave coming later in the decade has grown larger, not smaller. Braemar, the shipbroking firm, told Splash247 in June 2026 that recent tanker ordering, particularly of large crude carriers, is troubling, and that tanker markets could weaken over the next 12 months as delayed demand recovery is outpaced by supply growth. Breakwave Advisors, writing around the same time, projected a meaningful negative supply-demand balance developing longer term, with a potential downcycle as the consequence.

The market is, in other words, ordering its way toward two opposite problems at once. In the near term, a fleet that is aging faster than it is renewing keeps effective supply tight, supports freight rates, and validates the bull case that drove the order wave. In the medium term, if the new hulls arrive in volume at the same time that demand growth disappoints, or at the same time that the shadow fleet contracts, the delivery pressure that is being assembled right now could flip the market into oversupply. The transition between those two states is not a cliff. It is a slope, and the industry has historically struggled to identify exactly where on the slope it is standing.

What makes the current moment genuinely unusual is that both conditions, the aging-fleet drag and the coming delivery wave, are more extreme than at any point in recent memory. The aged fleet is larger, in absolute and proportional terms, than the industry has ever run with. The orderbook, at 33 percent of the live fleet for tankers overall and at roughly 30 percent for VLCCs specifically, is as large as it has been in more than a decade. And the gap between nominal and effective growth that Tankers International identified in 2025 has not narrowed: it has widened, because the aged ships that were already past their traditional end-of-life in 2025 are a year older now, and the new contracts signed in Q1 2026 are not due for delivery in time to close it.

For anyone trying to understand where freight rates go next, this is the load-bearing fact. The tanker market’s effective supply is not growing at the rate the raw orderbook suggests. It is growing at a fraction of that rate, because each new hull arriving at the dock is partly filling the gap left by aging vessels that were never properly retired. The headline number says the fleet is about to expand. The effective number says it is barely keeping pace. The difference between those two readings is where the freight rate lives, and right now the market is reading the wrong one.

Related Coverage

The IMO Just Cleared the Path for the Autonomous Tanker. Owners Are Ordering 140 New Supertankers to Match.

Trump Just Ordered Hormuz Open and the Blockade Lifted. Is the Tanker Boom Over?

Iran’s Revolutionary Guard Says It Just Closed the Strait of Hormuz. Iran’s Own Government Says It’s Open.

📊 By The Numbers