Oil Just Crashed Below $75, on Track for Its Worst Week in Months as Hormuz Reopens. Is the Record Tanker Boom Already Unwinding?

Brent shed nearly 7% this week as Hormuz traffic climbed to its highest level since February. The $468,900-a-day VLCC era is now on the clock.

⚓ The Gosships Team

Gosships Intelligence Is Published At Gosships.com

For Sponsorship And Partnership Inquiries Contact intelligence@gosships.com

|⚓ About Us | 🛢️ Exclusive Report | 📋 SwiftAction Training |

🏅Black Gold Membership (*53 Slots Left)

Oil just did something it has not done since the war began: it fell below $75 a barrel and kept falling, on track for its worst week in months, and the reason is sitting right there on every shipper’s screen. Brent crude dropped to $74.84 on Friday June 26, down nearly 7% on the week, as Strait of Hormuz traffic climbed to its highest level since Iran shut the lane on February 28. The geopolitical risk premium that had driven Brent above $120 at the height of the conflict is unwinding in real time, and the tanker market that feasted on that premium, banking VLCC day rates above $468,000, is now staring down the same unwind. Every barrel of crude that clears the strait on its way to a refinery eventually becomes the fuel you put in your car. Prices spiked at the pump when Hormuz closed. The question the market is wrestling with right now is how fast they fall as it reopens, and whether the tanker rate records of the last four months can possibly survive the answer.

📋 In This Issue:

🛢️ The Story

📊 By The Numbers

🔍 Why It Matters

👀 What To Watch

🚨 Gosships Signal

🔔 Not Yet Subscribed? Gosships Intelligence Delivers Oil Shipping Intelligence. Subscribe Here!

📊 Order Our Exclusive Report

→ Global Tanker Market Outlook Q3 2026 Edition

📋 Competency-Based Maritime Training

→ SwiftAction

📌 Gosships Data Card

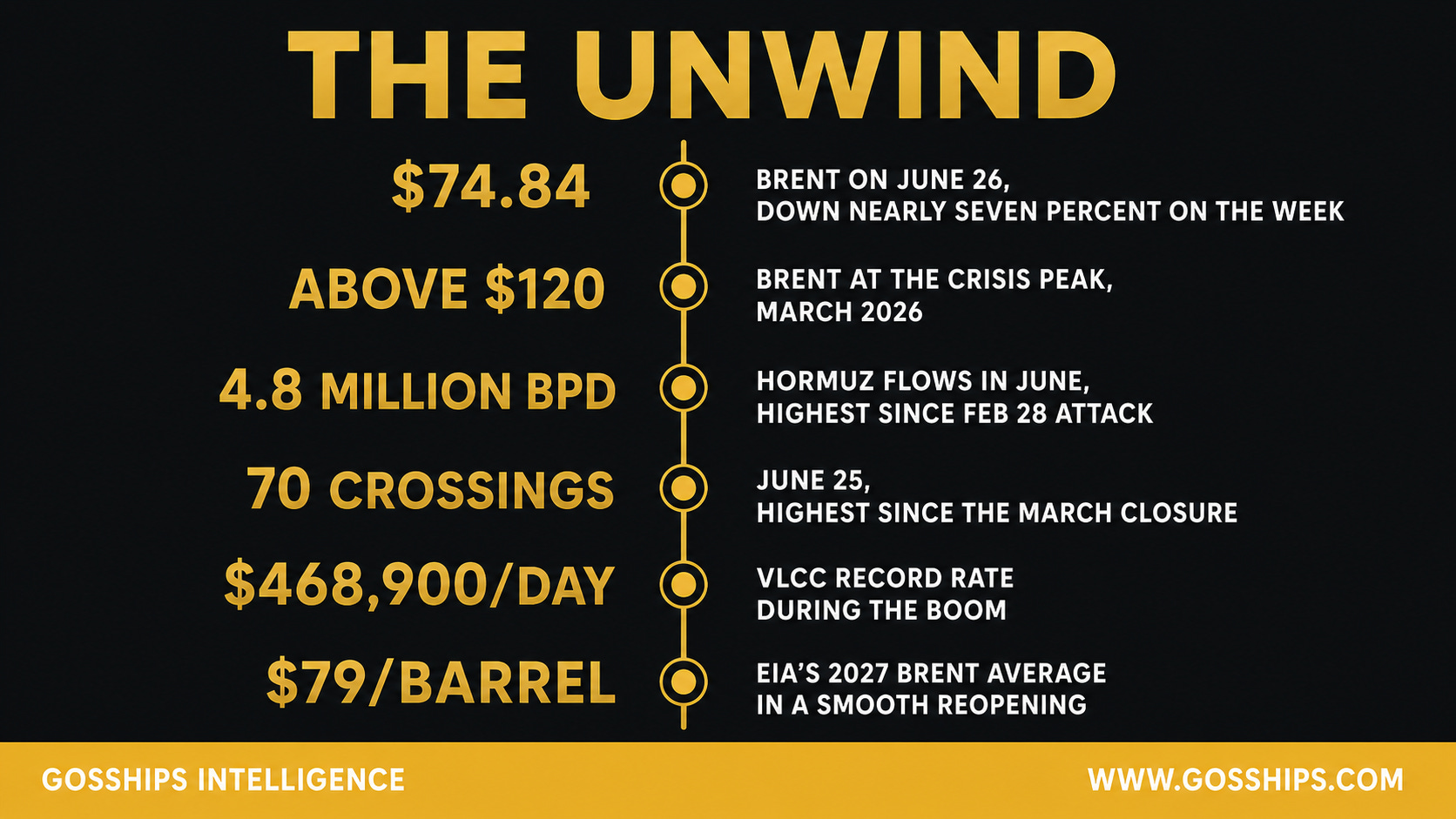

→ $74.84 - Brent on June 26, down nearly 7% on the week (Sunday Guardian / Investing.com)

→ Above $120 - Brent at the crisis peak, March 2026 (CNBC / militaryspend.org)

→ 4.8 million bpd - Hormuz flows in June, highest since the Feb 28 attack (CNBC)

→ 70 crossings - June 25 total, highest since the March closure, still under 60% of baseline (Kpler)

→ $468,900/day - VLCC record rate during the boom (TradeWinds)

→ $79/barrel - EIA’s 2027 Brent average forecast in a smooth reopening (EIA June 2026 STEO)

Sources: Sunday Guardian; CNBC; Kpler; TradeWinds; EIA June 2026 Short-Term Energy Outlook.

🛢️ The Story

At the height of the conflict, Brent crude was above $120 a barrel and VLCC owners were banking day rates that had never been seen in the history of the trade. On Friday June 26, 2026, Brent fell to $74.84, down roughly 0.56% on the day and on pace for a weekly loss of nearly 7%, one of the sharpest single-week drops since the crisis began, according to Sunday Guardian and Investing.com. West Texas Intermediate was trading near $71.50. The driver is no mystery: the Strait of Hormuz, the chokepoint that carries roughly 15 million barrels per day in normal times, is reopening, and traders are cutting the geopolitical risk premium with it.

The reopening is real but it is not complete. Hormuz tanker flows have recovered to approximately 4.8 million barrels per day in June, the highest level since Iran effectively closed the strait on February 28, according to CNBC. That is still less than one-third of the prewar baseline. Kpler counted 70 vessel crossings on June 25, the highest single-day figure since the March closure, yet that total still represents less than 60% of the daily traffic Hormuz was handling before the conflict began. CNBC reports that at least 20 non-Iranian tankers carrying approximately 35 million barrels have exited the strait since the U.S.-Iran deal framework emerged in mid-June, when Washington and Tehran agreed to a 60-day toll-free transit arrangement and the U.S. Navy ended its blockade. The physical reopening is underway. The market, however, is not waiting for it to be complete before pricing in the full unwind.

The oil price story of 2026 has been one of historic swings. Brent was trading near $72 a barrel on February 27. When U.S. and Israeli forces struck Iran on February 28 and the strait went dark, prices began a surge that took Brent above $120 at its peak, a gain of more than 55% in under five weeks, representing one of the largest monthly oil price jumps on record, as CNBC’s crisis timeline reported in April. The risk premium that built up during those weeks is now doing what risk premiums always do when the event that caused them begins to resolve: it is disappearing, fast.

For the tanker market, the implications cut both ways. The freight boom that defined the Hormuz crisis was built entirely on scarcity and danger, and both are now easing simultaneously. During the worst weeks of the blockade, VLCC rates on Hormuz transits surged to levels the market had never seen. Embiricos, one of the oldest names in Greek shipping, fixed a VLCC at $468,900 per day, as TradeWinds reported, as adventurous Greek owners began sailing back into the Persian Gulf while most of the industry stayed clear. Minerva Marine’s Pantanassa was fixed at $436,000 per day and later re-fixed to South Korea’s S-Oil at roughly $554,771 per day after the initial GS Caltex charter collapsed, according to TradeWinds and Tankers International. Seatrade Maritime reported VLCC rates fixing near $470,000 per day for Hormuz transits at the height of the frenzy. Those numbers emerged from a market where, as Lloyd’s List reported, VLCC loadings out of the Gulf had fallen roughly 36%, leaving fewer and fewer ships available to carry cargoes that charterers absolutely had to move.

The Hormuz toll that Iran introduced during the crisis also added to freight costs and insurance burdens. With the 60-day toll-free window now in place under the U.S.-Iran agreement, one layer of that cost is gone. War-risk insurance premiums, which had climbed to extraordinary levels during the blockade, have begun to fall. S&P Global reports that the additional war-risk premium for Gulf transits has come well off its highs, easing from around 2.5% of hull value per seven-day period at the crisis peak toward roughly 1%, which is still many times the pre-war level of about 0.25%. However, the same source notes that London underwriters are not celebrating yet. The Lloyd’s Market Association and the broader London market require sustained, incident-free passage records before they will meaningfully reduce their listed-area designations, and mines remain in portions of the strait. The insurance unwind is real, but it is tracking physical evidence of safe transits, not political agreements on paper.

The price forecasts are now moving in a direction that would have been unthinkable in March. The EIA’s June 2026 Short-Term Energy Outlook projects Brent to average approximately $79 per barrel in 2027, contingent on flows through the Strait of Hormuz resuming incrementally and producers gradually restoring shut-in production. That is a long way from $120, and some banks are even more aggressive on the downside. Citi cut its Brent forecast to $75 per barrel for Q3 2026 and $70 per barrel for Q4, implying further price erosion through the second half of the year as supply returns. Goldman Sachs, citing Middle East output losses, has stayed more bullish with its Q4 2026 Brent target up near $90, according to Reuters. J.P. Morgan has warned of a scenario where Brent resets toward the $30s per barrel if OPEC+ fails to manage the pace of returning supply, a risk the bank ties specifically to the simultaneous production growth ambitions of multiple large non-OPEC and OPEC producers into 2027.

The tanker market is now navigating two separate realities at once. On one hand, the vessels that banked the record rates during the crisis were converting scarcity into cash, and some of those voyages are still completing, still earning elevated freight. On the other hand, every tanker that sails successfully through Hormuz adds one more data point to the argument that the strait is functional again, which compresses rates for every vessel behind it. The question for owners, brokers, and charterers is not whether the unwind is happening. It is happening. Sunday Guardian and Al Jazeera both reported on June 26 that the slide in oil prices reflects exactly the market reading a reopening as a supply-positive event. The question is how far rates fall, how fast, and whether the record asset values that VLCC owners booked during the boom, with some older 310,000-dwt vessels surging to 18-year highs, hold their ground as the freight premium drains away.

War-risk insurance is the gauge that matters most in the near term. LeapRate reported on June 26 that the Hormuz unwind has reached the freight market with insurance costs as the clearest signal. When underwriters formally remove Hormuz from the Joint War Committee’s listed-area designation, the cost of insuring a transit will fall sharply, and with it the rate premium that made $468,900-per-day fixtures possible in the first place. That formal removal requires not a ceasefire paper but a sustained record of incident-free passage, mine clearance progress, and a settled geopolitical picture. None of those three conditions is yet fully in place. The tanker boom is unwinding. The question is whether it collapses quickly or bleeds out slowly, and the insurance market, not the political calendar, will decide the pace.

Five personas are already repositioning their books around the answer to that question. What the drop means for each of them, and the one signal that could flip the direction of the unwind overnight, is below.

Related Coverage

Trump Just Ordered Hormuz Open and the Blockade Lifted. Is the Tanker Boom Over?

Iran’s Revolutionary Guard Says It Just Closed the Strait of Hormuz. Iran’s Own Government Says It’s Open.

The IMO Just Cleared the Path for the Autonomous Tanker. Owners Are Ordering 140 New Supertankers to Match.

📊 By The Numbers