How Did Gunvor Make a Full Year’s Profit in a Single Quarter?

The trading house booked its entire 2025 gross profit, $1.63 billion, in Q1 2026 alone. Behind the number is a masterclass in trading global volatility.

⚓ The Gosships Team

Gosships Intelligence Is Published At Gosships.com

For Sponsorship And Partnership Inquiries Contact intelligence@gosships.com

|⚓ About Us | 🛢️ Exclusive Report | 📋 SwiftAction Training |

🏅Black Gold Membership (*53 Slots Left)

In the first three months of 2026, Gunvor made as much gross profit as it did in the entire previous year. The engine behind that quarter was disorder: war in the Gulf, sanctions on Russia, and the wildest energy price swings in years. The trouble is that the same disorder is exactly what keeps Washington branding the trader a Kremlin puppet. Gunvor is caught between the chaos that pays it and the chaos that taints it, and which one wins will decide what kind of company it becomes.

📋 In This Issue:

🛢️ The Story

📊 By The Numbers

🔍 Why It Matters

👀 What To Watch

🚨 Gosships Signal

🔔 Not Subscribed? Gosships Intelligence Delivers Oil Shipping Intelligence. Subscribe Here!

📊 Order Our Exclusive Report

→ Global Tanker Market Outlook Q3 2026 Edition

📋 Competency-Based Maritime Training

→ SwiftAction

📌 Gosships Data Card

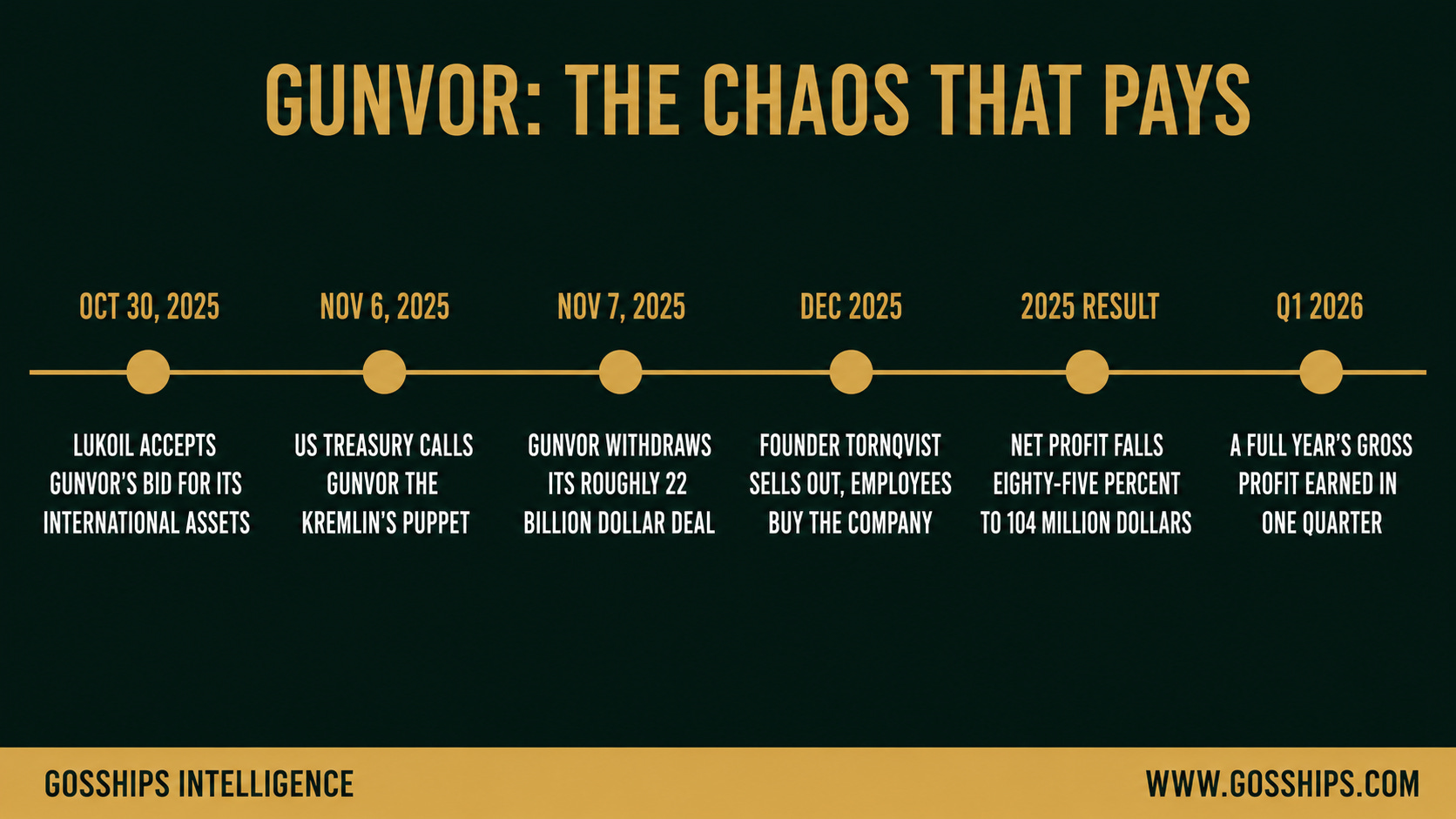

→ Oct 30, 2025: Lukoil accepts Gunvor’s offer for its international assets after the Russian major is hit by US sanctions (The Moscow Times)

→ Nov 6, 2025: the US Treasury posts that Gunvor is “the Kremlin’s puppet” and will “never get a license to operate and profit” (US Treasury; bne IntelliNews)

→ Nov 7, 2025: Gunvor withdraws its bid, a deal reported at around $22 billion (The Moscow Times)

→ Dec 2025: founder Torbjorn Tornqvist, 72, sells his 86.1% stake to about 60 employees and steps down; Gary Pedersen becomes CEO (Gunvor Group)

→ 2025 full year: net profit falls about 85% to $104 million, including $462 million of writedowns booked by new management (Reuters)

→ Q1 2026: CEO Pedersen says Gunvor made the equivalent of its full-year 2025 gross profit, $1.63 billion, in the first quarter alone (Bloomberg; Reuters)

Sources: The Moscow Times; US Treasury; bne IntelliNews; Gunvor Group; Reuters; Bloomberg.

🛢️ The Story

In the first quarter of 2026, Gunvor made as much gross profit as it had in the whole of the previous year. According to CEO Gary Pedersen, speaking to Bloomberg and Reuters, the commodity trading house booked the equivalent of its entire full-year 2025 gross profit, about $1.63 billion, in the first three months of 2026 alone. He credited a pickup in what he called “constructive volatility” that began late in 2025 and ran into the new year, and he singled out the energy segment, natural gas, LNG, and power, as the strongest contributor. In a single quarter, Gunvor did a year’s work.

To understand why that number matters, you have to understand what a trading house actually sells. Firms like Gunvor, and its larger rivals Vitol, Trafigura, and Mercuria, sit between the producers of oil and gas and the refiners and utilities that consume it. They make money on movement, on the spread between where a barrel is cheap and where it is dear, on the timing of when to store a cargo and when to sell it, and on their ability to keep physical energy flowing when everyone else is scrambling. Calm, orderly markets are thin markets for a trader. Dislocation is the product. The wider and more violent the price swings, the more money a house that controls the physical flows can make, which is why the great trading windfalls have always coincided with the great disruptions. The energy crisis that followed Russia’s 2022 invasion of Ukraine produced record profits across the sector, and the turmoil of 2026, a war in the Gulf, a chokepoint closed, sanctions multiplying, has done it again.

The mechanism is worth spelling out, because it is the key to the whole paradox. A trading house makes its money from three things that all get bigger when markets break: the price gap between regions, the value of storing a cargo now to sell it later, and the premium the market pays anyone who can keep physical barrels moving when the normal routes seize up. All three widen with disruption. When the Strait of Hormuz closes, when sanctions scramble who can buy from whom, when freight and insurance costs whipsaw, the spreads a trader lives on blow out, and the firms with the ships, the storage, and the relationships to move oil around the blockage capture the difference. That is why 2022 and 2023, the years of the Ukraine energy shock, produced the largest profits in the history of the independent trading sector, with Vitol, Trafigura, Mercuria, and Gunvor all posting record or near-record numbers. It is also why 2026 has been another bonanza. The Iran war did not just threaten supply; it manufactured exactly the dislocation a physical trader converts into margin. For the shipping market the link is direct: a trader capturing those dislocation margins is also chartering the tankers and gas carriers that move the barrels around the disruption, so a bumper quarter for Gunvor tends to mean more fixtures, more storage plays, and more tonne-miles as cargoes take longer, stranger routes to their buyers.

This is what makes the trading houses so difficult for policymakers to corner. The same crises that governments spend blood and treasure trying to contain are the crises that hand the traders their best years, and the more aggressively the world sanctions, blockades, and reroutes energy, the more valuable the handful of firms that can still make the barrels flow becomes. Gunvor sits inside that contradiction more sharply than any of its peers, because it is both a prime beneficiary of the disorder and, thanks to its Russian lineage, a prime target of the policy trying to impose order on it. The profits and the scrutiny are not two separate stories. They are the same story told from two directions.

So Gunvor’s blockbuster quarter is not a mystery. It is the trading model working exactly as designed, in a year purpose-built for it. And that is precisely where the trouble begins, because the same disorder that filled Gunvor’s coffers is the disorder that keeps its name in the wrong headlines.

Rewind three months from that record quarter, to the end of 2025, and Gunvor was not a company anyone would have called a winner. On October 30, 2025, it had reached the deal of its life: Lukoil, Russia’s second-largest oil producer, freshly hit by US sanctions, accepted Gunvor’s offer to buy its entire international portfolio of refineries, storage, wholesale supply, and retail networks, a transaction The Moscow Times reported at around $22 billion. It would have been the largest acquisition in Gunvor’s history. It lasted about a week. On the evening of November 6, the US Treasury did something it almost never does to a private company: it attacked one by name, in public, on social media, calling Gunvor “the Kremlin’s puppet” and warning that the trader would “never get a license to operate and profit.” The following day, November 7, Gunvor withdrew its proposal. Its corporate affairs director, Seth Pietras, called the Treasury statement “fundamentally misinformed and false,” and in the same breath confirmed that Gunvor was walking away. One sentence from Washington had erased a $22 billion deal.

The label carried that much force because of what it reached back to. Gunvor was co-founded by Gennady Timchenko, a Russian businessman close to Vladimir Putin, who sold his stake in 2014, the day before the US sanctioned him over Russia’s annexation of Crimea. Gunvor has spent the decade since insisting the association ended there. But the geopolitical disorder of 2026 keeps dragging Russia, sanctions, and the machinery of energy warfare back to the center of the story, and every time it does, Gunvor’s Russian past is the thread Washington pulls. This is the paradox in its sharpest form. The volatility that pays Gunvor is manufactured by the same conflicts and sanctions regimes that make a firm with Russian roots politically radioactive. When the world is calm, Gunvor earns less but draws less suspicion. When the world is on fire, it prints money and Washington circles. It cannot have the profits without the environment that produces the scrutiny.

The founder read that trap and got out. In December 2025, Gunvor completed a management buyout in which Torbjorn Tornqvist, the 72-year-old founder and chief executive, sold his entire holding and stepped down on the spot. According to Gunvor and reporting by Reuters and Bloomberg, roughly 60 employees acquired Tornqvist’s 86.1% stake, financed through partners’ equity and a vendor loan from Tornqvist himself, repayable over as long as ten years. Bloomberg reported he took more than $1 billion upfront, and earlier Reuters reporting valued the group at around $5 billion. Gunvor framed the deal, first conceived in 2022, as a “definitive reset,” saying that misperceptions about its past had become “an impossible distraction.” Strip away the corporate language and the shape of the move is stark: the founder took his roughly $1 billion in proceeds and transferred both the ownership and the reputational liability to his own employees, who staked their capital on the bet that the chaos keeps paying. The board then named Gary Pedersen, the American head of Gunvor’s Americas business and a veteran of Koch Industries, as chief executive, a deliberately US-facing choice for a firm whose central liability is its perceived proximity to Moscow.

The timing of that exit rewards a close look, because it cuts against the easy story. Tornqvist did not sell at an obvious peak. He sold at the end of Gunvor’s worst year in recent memory. The 2025 results, reported in April 2026, showed net profit collapsing about 85% to $104 million, dragged down by $462 million of writedowns and impairments that the incoming management team booked, according to Reuters, the classic move of new leadership clearing the decks. On the headline number, Gunvor had almost stopped making money. Then, one quarter later, the war-driven volatility of early 2026 arrived and the operating engine roared back to a full year’s gross profit in three months. The founder took his billion out at the trough; the employees who bought in caught the rebound. Whether that makes Tornqvist unlucky or merely done with the fight, it underlines the same point: Gunvor’s fortunes swing with the disorder in the world, and the disorder had just turned back in its favor.

The cost of the taint, meanwhile, is not abstract. It is the $22 billion deal Gunvor could not do. After it withdrew, Lukoil agreed in late January 2026 to sell its international assets instead to the US private-equity firm Carlyle Group, a transaction that as of mid-2026 still awaits OFAC approval, with US supermajors Chevron and ExxonMobil and Abu Dhabi’s International Holding Company also reported to have expressed interest, according to OilPrice, Lukoil’s own statements, and Interfax. The message is hard to miss. Washington blocked the trader it called a Kremlin puppet and steered the assets toward American and Gulf buyers instead. Gunvor had the cash and the appetite for the largest prize in the post-sanctions energy landscape, and the label alone kept it from the table. That is what the taint costs: not the profits, which are flowing, but the strategic deals that would turn those profits into permanence.

The taint is not only about deals; it is increasingly about the plumbing. A trading house runs on credit, on the letters of credit and revolving facilities that let it finance cargoes many times larger than its own balance sheet, and that makes its banking relationships the true front line. Here the signals point in opposite directions at once. In June 2026 Gunvor’s Singapore arm closed a sustainability-linked revolving credit facility of about $1.366 billion, upsized from an initial $800 million and more than 70% oversubscribed across 32 banks, a resounding vote of confidence from the lenders who joined. Yet in the same period the US Treasury secretary publicly praised Santander for pulling out of a Gunvor financing, a pointed reminder that the pressure campaign is live and that some institutions will step back rather than risk Washington’s displeasure. Gunvor can fund itself, but it must now do so through a banking market Washington is actively trying to split.

That the “Kremlin’s puppet” line landed at all, more than a decade after Gennady Timchenko sold his stake, tells you how durable the association is. Timchenko exited in 2014, the day before US sanctions hit him over Crimea, and by the letter of the ownership record Gunvor’s Russian chapter closed then. But perception does not follow the cap table. In a period when energy has become an instrument of war and sanctions the weapon of choice, a firm founded by a Putin associate is a natural target whenever Washington wants to send a message, regardless of who holds the shares today. That is the deeper reason the reset is so hard: Gunvor is not fighting a fact it can correct, it is fighting a story the world’s disorder keeps making relevant.

So Gunvor is trying to build a business that leans less on the chaos-and-Russia axis and more on something Washington might actually bless. Through June and July 2026 it pushed hard into power and gas rather than oil acquisitions, expanding its Asia-Pacific power platform with a twelve-year electricity supply agreement to Firmus Technologies in South Australia, a linked battery-storage offtake, and a deal to feed 600 megawatts to Firmus data-centre, or AI-factory, campuses, according to Gunvor and its adviser White & Case. It showed it can still raise money at scale, with its Singapore arm closing a sustainability-linked revolving credit facility of about $1.366 billion in June, upsized from an initial $800 million and more than 70% oversubscribed across 32 banks. The counter-signal is that the pressure has not lifted: the US Treasury secretary publicly praised Santander for pulling out of a Gunvor financing, a reminder that some banks are stepping back even as others pile in. And a separate corruption investigation by Swiss prosecutors over an oil deal in Gabon still hangs over the group.

There is a historical rhyme worth noting. The independent traders have weathered reputational storms before and come out larger, because the market’s need for someone to move the physical barrels almost always outlasts the scandal of the moment. What is different for Gunvor is that its problem is not a trading loss, a rogue desk, or a single investigation, the kinds of wounds a firm heals with a good year. It is a geopolitical alignment, a perceived closeness to Moscow that the world’s disorder keeps reactivating, and geopolitics is the one variable a trading house cannot hedge on its own book. A calm decade might let the memory fade. The next crisis would bring it roaring back.

Which sets up the only question that matters for the years ahead, and it is a genuine one. Gunvor’s trading engine feeds on disorder, and disorder is abundant. But every stretch of disorder also refreshes the suspicion that keeps it locked out of the biggest deals and makes its banking relationships a running battle. A calmer world would starve the profits and, eventually, dull the scrutiny. A more chaotic one would swell the profits and sharpen it. The reset, the new American CEO, the pivot to power and AI-linked demand, is an attempt to escape that trap, to build a company that can prosper without depending on the very turmoil that taints it. Whether that works, and what it means for the tanker and gas-carrier trades a house of Gunvor’s size drives, is where the analysis, and the signals that will tell you which side is winning, are laid out below.

Related Coverage

Oil Just Crashed Below $75, on Track for Its Worst Week in Months as Hormuz Reopens. Is the Record Tanker Boom Already Unwinding?

The UAE Just Ended 59 Years in OPEC and Took Much of the World’s Spare Oil Capacity With It. Who Cushions the Next Shock?

Owners Just Ordered Tankers at the Fastest Pace in History, yet Effective Supply Will Grow Just 1% Over Three Years. Where Did the Fleet Go?

📊 By The Numbers