India Just Bought More Russian Oil Than Ever Before. It Is Also Buying Crude From Venezuela and West Africa Now. Every Barrel Is Sailing Farther Than in Years. Who Really Wins?

India’s June crude imports are on track for a historic record, but the real story is the distance every barrel must travel to get there.

⚓ The Gosships Team

Gosships Intelligence Is Published At Gosships.com

For Sponsorship And Partnership Inquiries Contact intelligence@gosships.com

|⚓ About Us | 🛢️ Exclusive Report | 📋 SwiftAction Training |

🏅Black Gold Membership (*53 Slots Left)

India is on track to set an all-time monthly record for Russian crude imports in June 2026, averaging 2.66 million barrels per day in the first nineteen days of the month, according to commodity intelligence firm Kpler, cited by Organiser on June 22, 2026. That figure is already far above the previous monthly record of 2.2 million barrels per day set in May 2023. But the headline number tells only half the story. At the same moment India is absorbing more Russian crude than it ever has, it has also turned to Venezuela, Nigeria, Angola, and Brazil at a scale unseen in years, barrels that have to travel vastly longer distances to reach Indian refiners than the short Middle East hauls that used to dominate. The reason is one of the most consequential disruptions to global crude flows in years: the 2026 Strait of Hormuz crisis, which cut off India’s short-haul Gulf supply and forced its refiners to source from an ocean away. The result is not just a record import figure. It is a structural lengthening of the voyages carrying India’s crude, a tonne-mile windfall that is one of the biggest quiet supports under the crude tanker market right now, and one that the mainstream headlines about Indian oil imports have almost entirely missed.

📋 In This Issue:

🛢️ The Story

📊 By The Numbers

🔍 Why It Matters

👀 What To Watch

🚨 Gosships Signal

🔔 Not Yet Subscribed? Gosships Intelligence Delivers Oil Shipping Intelligence. Subscribe Here!

📊 Order Our Exclusive Report

→ Global Tanker Market Outlook Q3 2026 Edition

📋 Competency-Based Maritime Training

→ SwiftAction

📌 Gosships Data Card

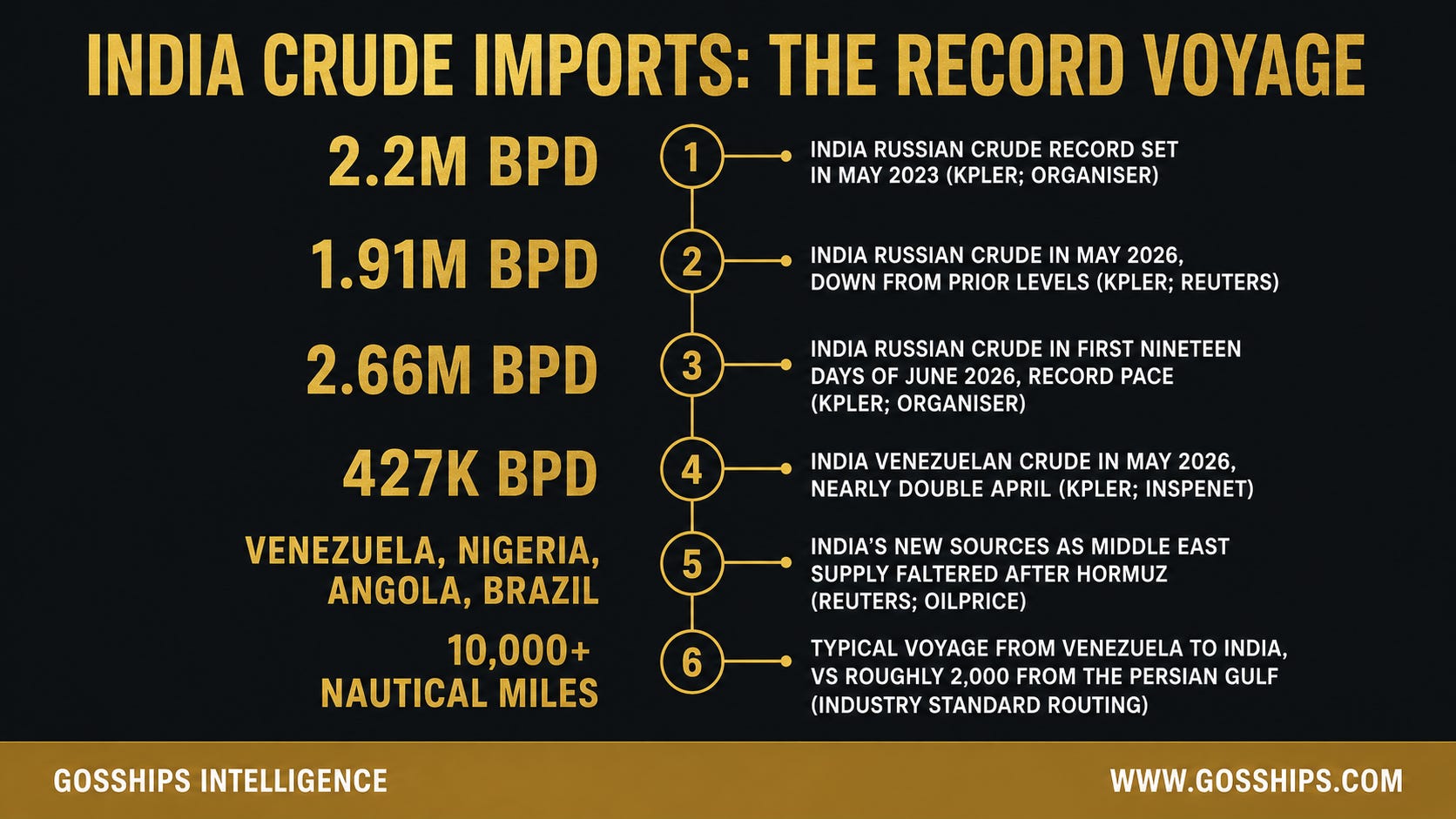

→ 2.2M BPD : India’s prior monthly record for Russian crude imports, set in May 2023 (Kpler; Organiser, June 22, 2026)

→ 1.91M BPD : India’s Russian crude imports in May 2026, the month before the current record run (Kpler via Reuters, May 25, 2026)

→ 2.66M BPD : India’s Russian crude imports in the first nineteen days of June 2026, well above record pace (Kpler; Organiser, June 22, 2026)

→ 427K BPD : India’s Venezuelan crude imports in May 2026, nearly double the roughly 283,000 bpd in April (Kpler; Inspenet, June 4, 2026)

→ Venezuela, Nigeria, Angola, Brazil : The new sources India turned to after the 2026 Hormuz disruption cut Middle East supply (Reuters, May 25, 2026; OilPrice, May 26, 2026)

→ 10,000+ Nautical Miles : Typical voyage length from Venezuela to India, versus roughly 2,000 nautical miles from the Persian Gulf, multiplying tanker demand and time-charter rates (Lloyd’s List; industry routing data)

Sources: Kpler; Organiser, June 22, 2026; Reuters, May 25, 2026; OilPrice, May 26, 2026; Inspenet, June 4, 2026; Lloyd’s List.

🛢️ The Story

The media narrative around India and Russian oil in 2026 has settled into a familiar groove: India is diversifying away from Russia, buying more from alternative sources, reducing its dependence on Russian crude in the wake of Western pressure. That narrative is wrong today, at least measured against the data. India is buying more Russian crude than it ever has at any point in recorded history, and the pace at which it is doing so in June 2026 is not a rounding error. It is a record by a margin.

India imported an average of 2.66 million barrels per day of crude from Russia in June through June 19, 2026, according to data from commodity intelligence firm Kpler, as reported by Organiser on June 22, 2026. That figure represents 53.5 percent of India’s total crude imports during the same period, meaning Russia is not merely India’s top supplier. Russia is supplying more than half of everything India is importing at the current pace. The prior monthly record stood at approximately 2.2 million barrels per day, set in May 2023, Kpler data cited by Organiser confirmed. Kpler estimates that India’s full-month June 2026 imports from Russia will exceed 2.35 million barrels per day, which would comfortably surpass that 2023 peak.

The June surge comes off a relatively soft base. In May 2026, India’s Russian crude imports stood at approximately 1.91 million barrels per day, according to Reuters reporting on May 25, 2026, citing Kpler data. That relative softness in May reflected, in part, the temporary shutdown of the 400,000-barrel-per-day Nayara Energy refinery for maintenance, as Reuters reported. With Nayara back online and Indian refiners actively rebuilding their Russian crude intake, the rebound in June has been dramatic, nearly 750,000 barrels per day above May’s pace in the first nineteen days of the month.

But if the Russia story were all there was, this would be a straightforward record import note. The more consequential tanker story lies beneath it.

The 2026 Strait of Hormuz disruption, triggered by the Israeli-U.S. war on Iran that broke out at the end of February, effectively closed India’s most convenient crude supply corridor. “Indian refiners turned to imports from Latin America and Africa after supplies from the Middle East were disrupted as the Israeli-U.S. war on Iran restricted shipping in the Strait of Hormuz,” Reuters reported on May 25, 2026, in a wire by Nidhi Verma. “Refiners in the world’s third-largest oil importer and consumer bought most of their crude from the nearby Middle East until the war broke out at the end of February.”

The pivot away from the short-haul Middle East trade and toward Russia, Latin America, and West Africa happened fast. “In April and May, Indian refiners raised imports from Venezuela, Brazil, Angola and Nigeria to make up the shortfall, as well as continuing to buy Russian oil,” Reuters reported, citing preliminary Kpler data. OilPrice.com, in a May 26, 2026 article by Tsvetana Paraskova, confirmed the scope of the shift: “As supply from the Middle East crashes, India is buying growing volumes of crude from West African producers Nigeria and Angola, as well as from South American producers Brazil and Venezuela. Brazil and Venezuela moved into the top five of India’s crude oil suppliers in April, according to the Kpler data cited by Reuters.”

Venezuela’s rise in India’s import mix has been particularly sharp. Indian imports of Venezuelan crude averaged approximately 417,000 barrels per day in May 2026, on preliminary Kpler tracking cited by Reuters and OilPrice, and a revised final figure of approximately 427,000 barrels per day by early June, per Inspenet reporting on June 4, 2026. The preliminary figure from OilPrice’s Paraskova described it as “nearly double from the 283,000 bpd shipped in April, and zero imports for the previous nine months.” That last point is important: India had effectively not been buying Venezuelan crude for three-quarters of a year before the Hormuz crisis forced a rapid reassessment of supply chains. Within three months of the disruption, Venezuela had become India’s third-largest crude supplier, behind only Russia and the UAE.

By June, the Venezuelan surge moderated as Russian crude flooded back in. Organiser’s June 22 piece, citing Kpler, placed Venezuela as India’s fourth-largest supplier in June through June 19, at approximately 209,000 barrels per day, behind Russia (2.66 million bpd), the UAE (636,000 bpd), and Saudi Arabia (384,000 bpd). The moderation of Venezuelan volumes in June does not reverse the diversification story. It reflects the sequencing: India used Venezuela, West Africa, and Brazil as emergency replacements in March, April, and May when Middle East supply cratered, and is now layering record Russian volumes on top as those flows normalize. The result in June is a supply mix that looks nothing like what it did a year ago, and the implications for tanker demand are structural.

Here is the tanker-market arithmetic that the import headlines do not capture. A VLCC loading crude in the Persian Gulf and sailing to India’s west coast refinery hub at Jamnagar covers approximately 2,000 nautical miles each way. It is one of the shortest major VLCC trade routes in the world. A VLCC loading at the Venezuelan terminal of Jose and sailing to Jamnagar covers more than 11,000 nautical miles. A West Africa loading from Bonny Light or Cabinda in Angola to India covers roughly 5,000 to 6,000 nautical miles. Russian crude loaded at Primorsk or Ust-Luga in the Baltic and sailing around Africa to India covers distances in excess of 12,000 nautical miles, though a portion of India’s Russian supply arrives from the Eastern Siberia Pacific Ocean pipeline ports closer to 3,000 to 4,500 nautical miles away, depending on destination port.

The metric that matters for tanker earnings is not barrels shipped but tonne-miles, the product of cargo tonnage and voyage distance. When India replaces a 2,000-nautical-mile Persian Gulf cargo with a 6,000-nautical-mile West African cargo, the tonne-mile demand generated by that single cargo triples, even though the barrel volume is identical. The tanker market does not trade barrels. It trades time and distance. When India’s effective voyage distances rise across all of its supply sources simultaneously, the demand for tanker capacity rises sharply without a single additional barrel needing to enter the market.

Lloyd’s List, in a 2026 piece covering Asia’s response to the Hormuz disruption, confirmed the mechanism: “Tanker tonne-mile demand is expected to rise sharply in the near term as Asia-Pacific refiners look for far-flung alternatives as a result of the conflict in the Middle East Gulf.” The research team at Vantage Shipbrokers was quoted in the same Lloyd’s List article noting that Asian refiners were actively considering “Atlantic Basin crude oil” as a Middle East alternative. “West African crude oil is also being heavily considered by Asian refiners,” the same piece noted. “A pivot from the Middle East to Russia would drive up tonne-mile demand for crude oil shipments to India,” Lloyd’s List added directly.

The tonne-mile impact runs across vessel classes. VLCCs benefit most on the long-haul Atlantic Basin routes from Venezuela and Brazil. Suezmax tankers, which dominate the West Africa to Asia trade, capture the Nigeria and Angola volumes. Aframax tankers benefit from shorter-haul Russian Baltic routes. The tanker market reading this situation from a headline of “India’s Russian crude hits record” is looking at the right data but missing the larger picture. The more consequential data point is not the origin of India’s crude. It is the distance every barrel is traveling to get there. And that distance, in June 2026, is longer than at any point in recent history.

For every tanker professional tracking capacity utilization, this structural voyage lengthening is not a temporary spike. It is a function of a supply geography that has been fundamentally rearranged by the Hormuz crisis. As long as India continues sourcing from Russia, Venezuela, and West Africa at current levels, rather than reverting to its pre-crisis Middle East dependency, the tonne-mile windfall is a persistent feature of the market, not a one-month anomaly. The question of how long it persists, and what it means for VLCC and Suezmax time-charter rates through the second half of 2026, is the analysis the mainstream headlines are not providing.