Is Dubai Building a Port Iran Can’t Close?

DP World is in talks to build a Fujairah port outside Hormuz to bypass the strait Iran blockaded, salvaging trade fleeing its 15.5M-TEU Jebel Ali hub.

⚓ The Gosships Team

Gosships Intelligence Is Published At Gosships.com

For Sponsorship And Partnership Inquiries Contact intelligence@gosships.com

|⚓ About Us | 🛢️ Exclusive Report | 📋 SwiftAction Training |

🏅Black Gold Membership (*53 Slots Left)

For fifty years, Dubai’s fortune rested on a single assumption: that the Strait of Hormuz would stay open. This week, Dubai stopped believing it.

DP World, the state-owned port giant, is in talks to build a new port and container terminal at Fujairah, on the open-ocean side of the strait, where cargo can reach the UAE without ever passing the chokepoint Iran keeps closing. It is the most expensive vote of no confidence in this war yet. Dubai is building a door the war cannot shut.

📋 In This Issue:

🛢️ The Story

📊 By The Numbers

🔍 Why It Matters

👀 What To Watch

🚨 Gosships Signal

🔔 Not Subscribed? Gosships Intelligence Delivers Oil Shipping Intelligence. Subscribe Here!

📊 Order Our Exclusive Report

→ Global Tanker Market Outlook Q3 2026 Edition

📋 Competency-Based Maritime Training

→ SwiftAction

Related Coverage

📌 Gosships Data Card

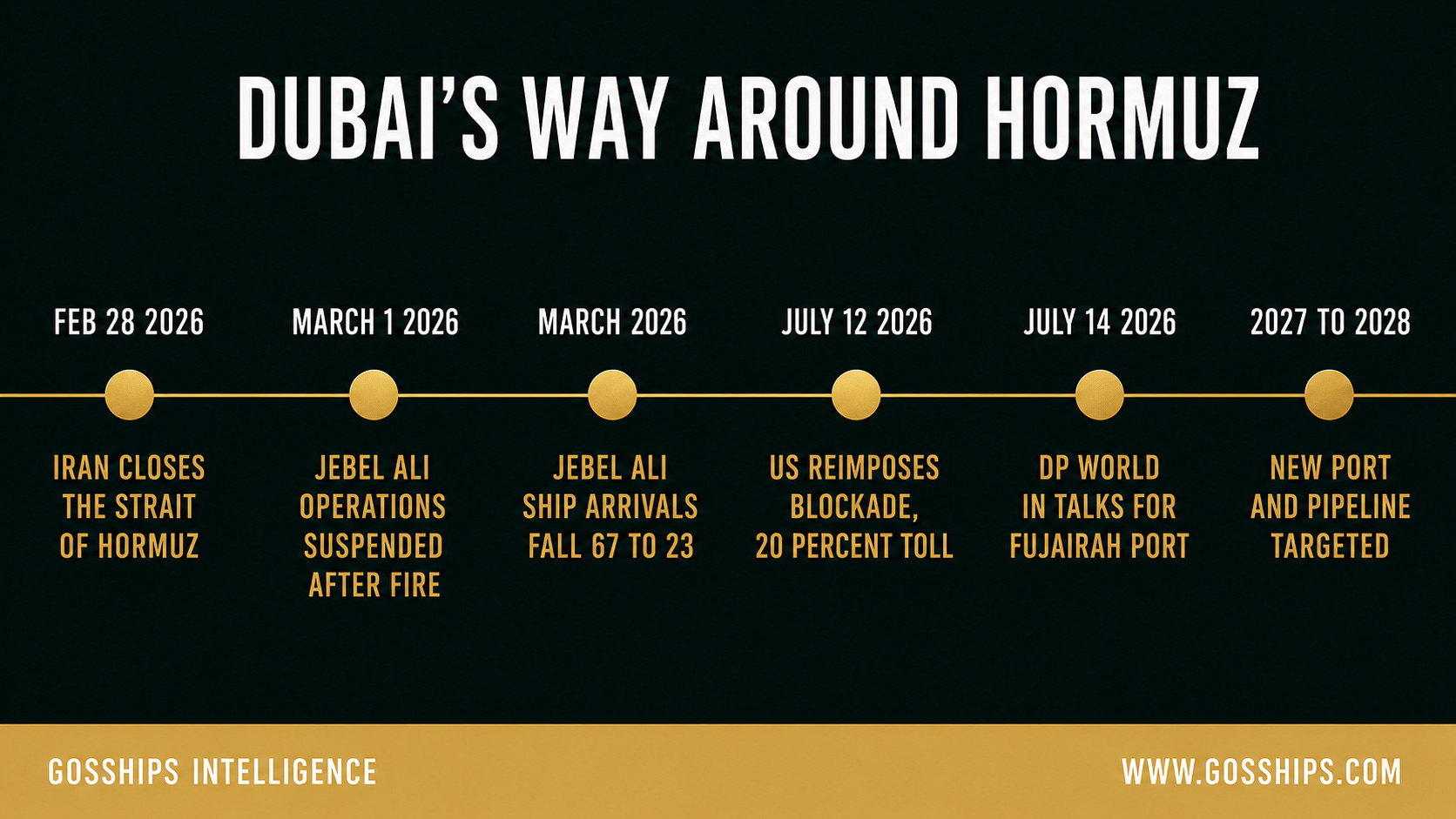

→ February 28, 2026: Iran closes the Strait of Hormuz as the US-Israel air war on Iran begins

→ March 1, 2026: DP World suspends Jebel Ali operations after a fire from falling debris

→ March 2026: Jebel Ali ship arrivals fall from 67 in late January to 23 by March 10

→ July 12, 2026: The US reimposes its Iran blockade and adds a 20 percent Hormuz toll

→ July 14, 2026: The FT reports DP World in talks to build a Fujairah port outside the strait

→ 2027 to 2028: The new container port, and ADNOC’s second Fujairah pipeline, are targeted to come online

Sources: Financial Times; DP World; ADNOC; VIZION; Lloyd’s List; contemporaneous reporting.

🛢️ The Story

For half a century, the logic of Dubai was that geography was destiny. Jebel Ali, the largest container port in the Middle East, sits inside the Persian Gulf, a few hours’ sail from the Strait of Hormuz, and it turned that position into the transshipment heart of a region. Roughly 33 million TEU move through Gulf ports every year, and Jebel Ali alone handles about 15.5 million of them, the primary node through which goods reach Dubai, Abu Dhabi and much of the wider Gulf. The entire model assumed the strait would always be open. In 2026 that assumption broke.

On July 14, the Financial Times reported that DP World, the state-owned operator of Jebel Ali, is in talks to build a new port and container terminal at Fujairah, the emirate on the UAE’s east coast that faces the Gulf of Oman, outside the Strait of Hormuz. The plan, according to the FT, is to give the UAE a gateway that cargo can reach without ever transiting the strait. Containers would land at Fujairah and move overland by road to Dubai, Abu Dhabi and the other Gulf emirates. A senior company official told the paper the port could be operational in about eighteen months. The project is still early stage rather than a final investment decision, a term sheet is being negotiated with UAE government officials, and the structure and financing have not been settled. But the direction is unmistakable: the UAE is building physical insurance against its own front door.

To understand why a port operator would consider spending years and billions to route around its own flagship hub, you have to look at what happened to that hub. When the US-Israel air war on Iran began on February 28 and Iran closed the Strait of Hormuz, the Gulf’s container system seized. On March 1, DP World suspended operations at Jebel Ali after a fire caused by falling debris from an aerial interception. Ship arrivals collapsed. According to vessel-tracking data, arrivals at Jebel Ali fell from 67 in late January to just 23 by March 10, and regional container throughput dropped by as much as 79 percent at the peak of the disruption. Average vessel waiting times at Jebel Ali jumped 178 percent. The busiest container gateway in the Gulf had become a place ships could not reliably reach.

The world’s major container lines reacted the way they always do, by leaving. MSC, the world’s largest container shipping company, along with Maersk, CMA CGM and Hapag-Lloyd, halted new bookings into the Gulf or slapped on emergency surcharges of up to $4,000 per container. At least fifteen container ships reversed course rather than enter or exit the strait. The Cape of Good Hope, the long route around southern Africa, became the main artery for Asia-to-Europe and Asia-to-Gulf cargo, adding weeks to voyages. Some shippers turned to a workaround that is now becoming a permanent strategy: land the containers at a port outside Hormuz, such as Khor Fakkan on the UAE east coast, and truck them inland. DP World’s Fujairah plan is that workaround, industrialized.

Crucially, this is not only a container story. The same geography that traps containers traps oil, and the UAE has been racing to fix that too. ADNOC, the Abu Dhabi national oil company, has been directed to fast-track a second crude pipeline to Fujairah, the terminal that sits on the Gulf of Oman coast beyond the strait. That pipeline was roughly half complete as of May 2026, with a target of 2027, and once online it would roughly double the UAE’s existing pipeline export capacity from around 1.8 million barrels a day. In the meantime, the UAE has been using tankers to shuttle crude from inside the strait to waters outside it, where the oil is transferred to larger ships for the run to Asia. A container port at Fujairah and a second crude pipeline to Fujairah are two halves of the same idea: move the UAE’s economic center of gravity to the safe side of the chokepoint.

The timing is what makes this a turning point rather than a contingency plan. The UAE did not commit to building around Hormuz when the strait briefly reopened. It committed as the strait was closing again. On July 12, President Trump reimposed the US blockade of Iranian shipping and announced that every other country would have to pay a 20 percent toll to move cargo through Hormuz, casting it as reimbursement for the US “providing safety and security to this very volatile section of the World.” On July 14, the day the DP World talks were reported, the blockade took effect and the war reached the shipping lanes directly. After a third consecutive night of US strikes on Iran’s coast, Iran’s Revolutionary Guard struck two Emirati supertankers transiting the strait, the ADNOC vessels Mombasa B and Al Bahyah, killing one crew member, and Brent crude climbed another 4.3 percent to $86.85, a one-month high. A port that skips Hormuz stops looking like a hedge and starts looking like a necessity.

There is a strategic subtext that a broker in Singapore or a trader in Geneva will read instantly. For decades, Iran’s single greatest source of leverage was the map. Roughly a fifth of the world's seaborne oil and a large share of the Gulf's containerized trade have to pass within missile range of the Iranian coast. Every plan to build around Hormuz, whether a Saudi pipeline to the Red Sea, an Emirati pipeline to Fujairah, or now an Emirati container port at Fujairah, chips a little more value off that leverage. It cannot be removed quickly. Fujairah cannot replace Jebel Ali's 15.5 million TEU overnight, and eighteen months is a long time in a war. But the direction of travel matters. The Gulf’s richest states are voting with concrete and steel that the chokepoint is a liability they intend to engineer around, not simply wait out.

The counterpoint deserves a fair hearing. Fujairah’s existing port is a major bunkering and fuel-storage hub, but it was not built to move millions of containers, and the road network from the east coast to Dubai and Abu Dhabi would carry a load it has never carried. Trucking containers over the Hajar Mountains is slower and costlier than sailing them into Jebel Ali, and it cannot match a deepwater container port’s throughput. Skeptics will note that grand Gulf infrastructure announcements do not always become steel, that the financing here is explicitly unsettled, and that if a durable ceasefire returned tomorrow the whole rationale would soften. All true. But the fact that DP World is negotiating a term sheet with the government rather than issuing a press release suggests this is further along than a trial balloon, and the parallel pipeline work shows the UAE is willing to spend real money on the same premise. What happens to the tanker market, the container lines and Iran’s leverage if this bypass actually gets built, and why the next year and a half may reset the map of Gulf trade, is below.