OPEC Wants to Flood the Market. It Cannot Find Enough Tankers to Do It. Can the Gulf Actually Deliver?

Saudi Arabia and the UAE are loading every terminal they can reach outside Hormuz. The barrels are there. After rates touched record highs, the ships are not.

⚓ The Gosships Team

Gosships Intelligence Is Published At Gosships.com

For Sponsorship And Partnership Inquiries Contact intelligence@gosships.com

|⚓ About Us | 🛢️ Exclusive Report | 📋 SwiftAction Training |

🏅Black Gold Membership (*53 Slots Left)

The Strait of Hormuz crisis is no longer primarily about whether oil can pass through the strait. It is about whether the Gulf can find enough ships to carry the extra barrels it has promised to load. Saudi Arabia is ramping tanker operations at Ras Tanura, the UAE is diverting crude through its Fujairah bypass pipeline, and Middle East producers from Kuwait to Qatar are all pressing to lift output, Reuters reported in late June 2026. The IEA’s June Oil Market Report confirmed that oil shipments through Hormuz rose sharply in early June, supported by ship-to-ship transfers in the Gulf of Oman, though a full recovery in flows is not immediate. The bottleneck has moved from the strait to the steel. VLCC earnings reached nearly $470,000 per day at the peak of the crisis, according to Lloyd’s List and Reuters, and the Baltic Exchange’s MEG-China TD3C index set a record near $423,736 per day in March 2026. Even as tensions eased and transits accelerated, freight costs remain substantially elevated. The Gulf simply cannot charter ships fast enough to move the crude it is suddenly free to sell, and after the most disruptive tanker-rate shock in years, the vessels to carry those barrels are not where they need to be. Whether OPEC’s production ambitions can translate into actual delivered barrels depends not on the geopolitics of a strait but on the arithmetic of a stretched global tanker market that is still recovering from the rate records it just set.

📋 In This Issue:

🛢️ The Story

📊 By The Numbers

🔍 Why It Matters

👀 What To Watch

🚨 Gosships Signal

🔔 Not Yet Subscribed? Gosships Intelligence Delivers Oil Shipping Intelligence. Subscribe Here!

📊 Order Our Exclusive Report

→ Global Tanker Market Outlook Q3 2026 Edition

📋 Competency-Based Maritime Training

→ SwiftAction

📌 Gosships Data Card

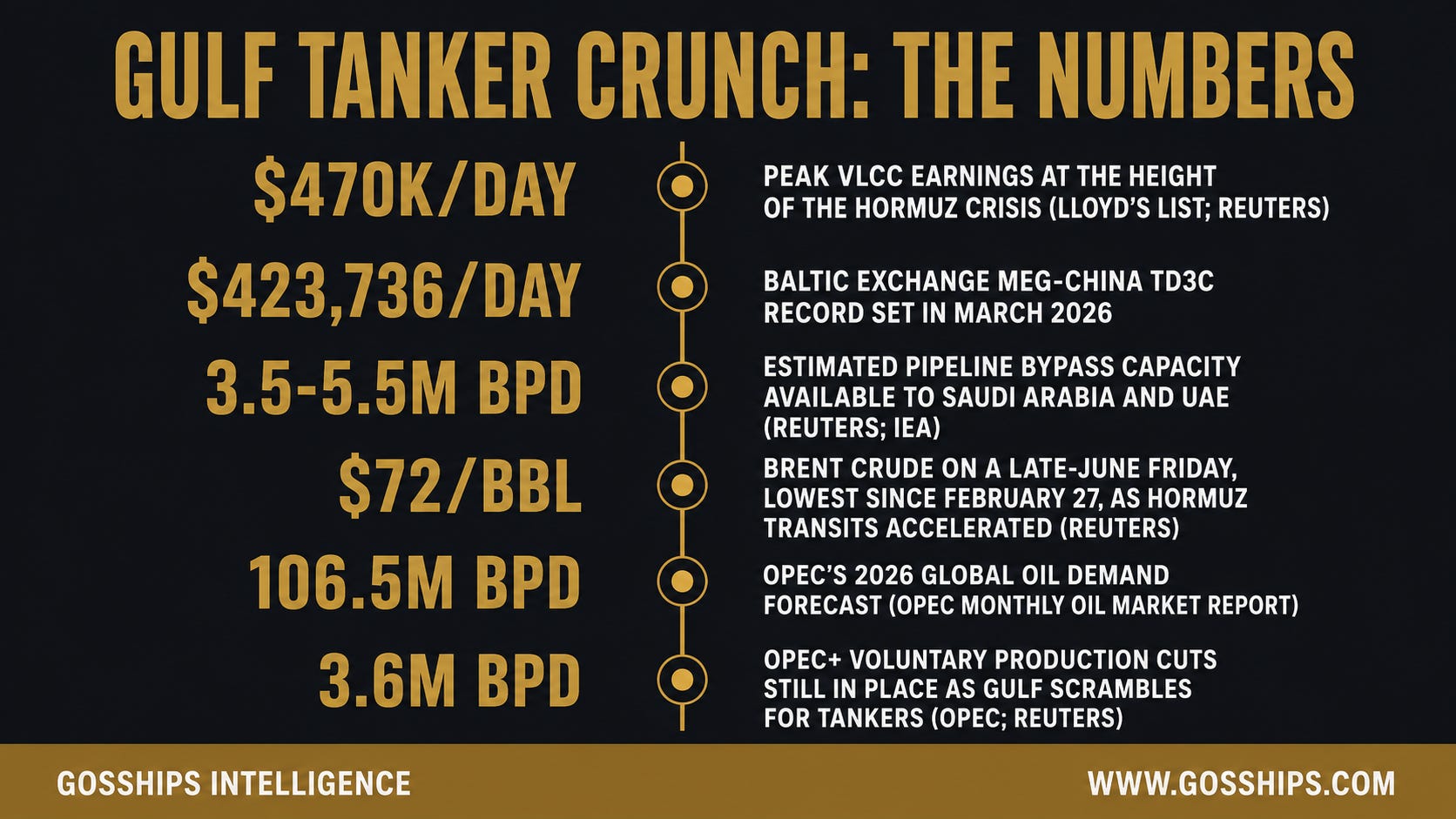

→ $470K/DAY - Peak VLCC earnings at the height of the Hormuz crisis (Lloyd’s List; Reuters)

→ $423,736/DAY - Baltic Exchange MEG-China TD3C record set in March 2026 (Baltic Exchange)

→ 3.5 to 5.5M BPD - Estimated pipeline bypass capacity available to Saudi Arabia and UAE around Hormuz (Reuters; IEA)

→ $72/BBL - Brent crude price on a late-June Friday, lowest since February 27, as Hormuz transits accelerated (Reuters; Trading Economics)

→ 106.5M BPD - OPEC’s 2026 global oil demand forecast, with growth of about 1.4 million bpd (OPEC Monthly Oil Market Report)

→ 3.6M BPD - OPEC+ voluntary production cuts still in place as Gulf producers scramble to secure tankers (OPEC; Reuters)

Sources: Baltic Exchange; Lloyd’s List; Reuters; IEA June Oil Market Report; OPEC Monthly Oil Market Report; Trading Economics.

🛢️ The Story

The crisis that paralysed Gulf oil flows was always framed as a question about the strait. Could tankers pass through Hormuz? Would transits recover? As the IEA’s June Oil Market Report confirmed, the answer has moved toward yes: oil shipments through the Strait of Hormuz rose sharply in early June 2026, with ship-to-ship transfers in the Gulf of Oman supporting the resumption of flows, even though a full recovery is not immediate. The passage problem is easing. The problem that has replaced it is more structural and in some ways more interesting. The Gulf cannot find enough ships.

Saudi Arabia, the UAE, Kuwait, and Qatar are all pressing to boost supply, Reuters reported in late June 2026. Saudi Arabia is loading tankers at Ras Tanura and ramping output. The UAE is diverting crude through its Fujairah pipeline bypass, which routes crude around the strait entirely and feeds directly to export terminals on the Gulf of Oman. Only Saudi Arabia and the UAE possess operational crude pipelines capable of routing flows around Hormuz, the IEA and Reuters confirmed, with an estimated 3.5 million to 5.5 million barrels per day of combined bypass capacity available. The barrels are there. The infrastructure to route them around the worst of the strait’s uncertainty exists. What does not exist in sufficient quantity, right now, in late June 2026, is the fleet of very large crude carriers willing and available to lift them.

To understand how this tanker shortage emerged, the story starts several months back. The Baltic Exchange’s MEG-China TD3C route index, which tracks VLCC freight from the Middle East Gulf to China and is the global benchmark for this trade, set a record near $423,736 per day in March 2026, according to Baltic Exchange data cited by Lloyd’s List and Reuters. That March record itself was not the peak. At the height of the Hormuz crisis, VLCC earnings climbed to nearly $470,000 per day, Lloyd’s List and Reuters reported. To put that figure in context: typical VLCC earnings in a normal freight market run somewhere between $30,000 and $60,000 per day. The crisis-era rate was not a spike of twenty or thirty percent above the norm. It was an order-of-magnitude surge that reflected a market in which demand for tankers to carry Gulf crude was colliding with genuine uncertainty about whether those tankers could safely transit the world’s most important oil chokepoint.

Those extreme rates set off a chain of market responses that are now constraining the Gulf’s ability to ramp up. When freight rates surge to record levels, charterers do not simply absorb the cost and keep booking. Many delay. Some divert. Some substitute. Global tanker scheduling and vessel positioning, which had been calibrated to normal route patterns, was disrupted. Ships that might have been positioned in the Gulf or en route to it were rerouted or held elsewhere as owners and charterers tried to navigate both the commercial and the security calculus. Elevating that baseline disruption is the fact that the broader tanker market heading into the crisis was already stretched, as Reuters noted. The global VLCC fleet is not a reserve army of vessels sitting idle waiting for the next emergency. Ships are on long-term fixtures, on return voyages, in dry dock, or chartered to other routes. Chartering a VLCC and getting it to the Gulf to load requires days to weeks even in a well-functioning market.

By late June 2026, as tensions eased and Hormuz transits accelerated, the Gulf producers’ problem shifted from security to supply chain. Reuters reported that Middle East producers including the UAE, Kuwait, and Qatar are struggling to secure enough tankers to carry the additional crude they are now positioned to export. Saudi Arabia is loading and ramping at Ras Tanura, but the constraint is not the terminal or the crude. It is the ship that is supposed to show up and take it. Even as freight costs have eased from their crisis peaks, they remain substantially elevated, Reuters and the Baltic Exchange confirmed. The market is not back to normal. The ships that were diverted, delayed, or held in reserve during the crisis peak have not all returned to their pre-crisis positions. The vessel-positioning disruption created by months of rate volatility takes time to unwind.

The broader demand context makes the stakes clear. OPEC’s Monthly Oil Market Report forecasts 2026 global oil demand growth of about 1.4 million barrels per day, with total demand near 106.5 million barrels per day. That is a market in which every barrel the Gulf can lift and deliver matters at the margin. OPEC+ maintains roughly 3.6 million barrels per day of voluntary production cuts, according to OPEC and Reuters, and Saudi Arabia has added unilateral cuts on top of that to defend an informal price floor Reuters estimated at $80 to $85 per barrel. Against that backdrop, the Gulf producers are now trying to unwind crisis-era restraint and lift output, and the signal from Brent crude tells part of the story: Reuters and Trading Economics reported that Brent fell to around $72 per barrel on a late-June Friday, the lowest level since February 27, 2026, as Hormuz transits accelerated and the market priced in the prospect of higher Gulf throughput. That is an $8 to $13 discount to the informal Saudi price floor, and it reflects markets getting ahead of the physical barrels. The tanker market has not yet caught up.

The mechanism that connects the tanker shortage to the price is direct and consequential. When the Gulf cannot charter ships fast enough to lift the volumes it wants to export, the crude backs up at terminals or sits in onshore storage rather than reaching refiners. Refiners who need barrels cannot get them on the timing they planned for, which pressures their own production schedules. The pipeline bypass capacity of 3.5 to 5.5 million barrels per day that Saudi Arabia and the UAE can route around Hormuz is only as useful as the tankers waiting at Fujairah and Yanbu to receive it. If those ships are not there, the bypass is a pipe that feeds into a terminal with no one to load. OPEC’s production ambitions, in other words, are currently conditional on a charter market that is still recovering from the rate shock it just experienced.

There is also a structural dimension to this shortage that will not resolve itself in days. Lifting extra volumes requires chartering ships in a stretched global tanker market, Reuters noted, after which those ships must physically sail to the region to load. That voyage time is not zero. A VLCC repositioning from ballast in the Atlantic or redeploying from a Pacific route can take ten days to three weeks to reach the Gulf, depending on where it is and what flag, owner, and fixture constraints apply. The market is liquid enough that vessels will move toward higher earnings, but it moves on a schedule measured in weeks, not hours. What the Gulf needs for its late-June and July loading programs cannot be fully solved by rate incentives posted today. Some of the constraint is simply the physical geography of getting enough steel to the right place at the right time.

This is the moment where the crossover between the freight market and the consumer price becomes visible, not at the pump in the reflex sense, but in the pipeline between a Gulf loading terminal and a refinery in Asia or Europe. Every day of delay in getting tankers to the Gulf to lift Saudi or UAE barrels is a day that extra crude does not reach the market. That extra crude, if it arrived on schedule, would contribute to the supply growth that OPEC is projecting and that the price market has partially discounted. The gap between what the market is pricing and what can actually be delivered in steel and barrels is the central risk in Gulf crude flows right now. The strait is open. The ships are not here yet. When they arrive, and how quickly the charter market normalizes, is the question that determines whether OPEC’s flood reaches the shore.