Who Pays as Hormuz Sends Tanker Rates Soaring?

As the reimposed blockade sends crude tanker rates surging again, up 92% in a week to the highest since March, owners like Frontline collect and you pay.

⚓ The Gosships Team

Gosships Intelligence Is Published At Gosships.com

For Sponsorship And Partnership Inquiries Contact intelligence@gosships.com

|⚓ About Us | 🛢️ Exclusive Report | 📋 SwiftAction Training |

🏅Black Gold Membership (*53 Slots Left)

A single benchmark crude tanker rate just jumped 92 percent in one week, and for the third time this year, the oil war has made the owners willing to sail Hormuz spectacularly rich.

When the United States reimposed its blockade on Iran on July 13 and Iran declared the strait closed again, the benchmark supertanker rate snapped back to $188,957 a day, its highest since March, and the mid-sized crude carriers behind it jumped more than 40 percent in the same week. None of that steel got faster or safer overnight; what changed is that sailing a laden tanker past the Iranian coast is now a bet on the ship's own survival, and the owners willing to take it can name their price. That premium does not stay at sea: the owner collects it first, the trader who charters him folds it into the delivered price of crude, and it reaches you last, as the extra cents a gallon nobody can quite explain. The owner is paid first. You pay last.

📋 In This Issue:

🛢️ The Story

📊 By The Numbers

🔍 Why It Matters

👀 What To Watch

🚨 Gosships Signal

🔔 Not Subscribed? Gosships Intelligence Delivers Oil Shipping Intelligence. Subscribe Here!

📊 Order Our Exclusive Report

→ Global Tanker Market Outlook Q3 2026 Edition

📋 Competency-Based Maritime Training

→ SwiftAction

Related Coverage

📌 Gosships Data Card

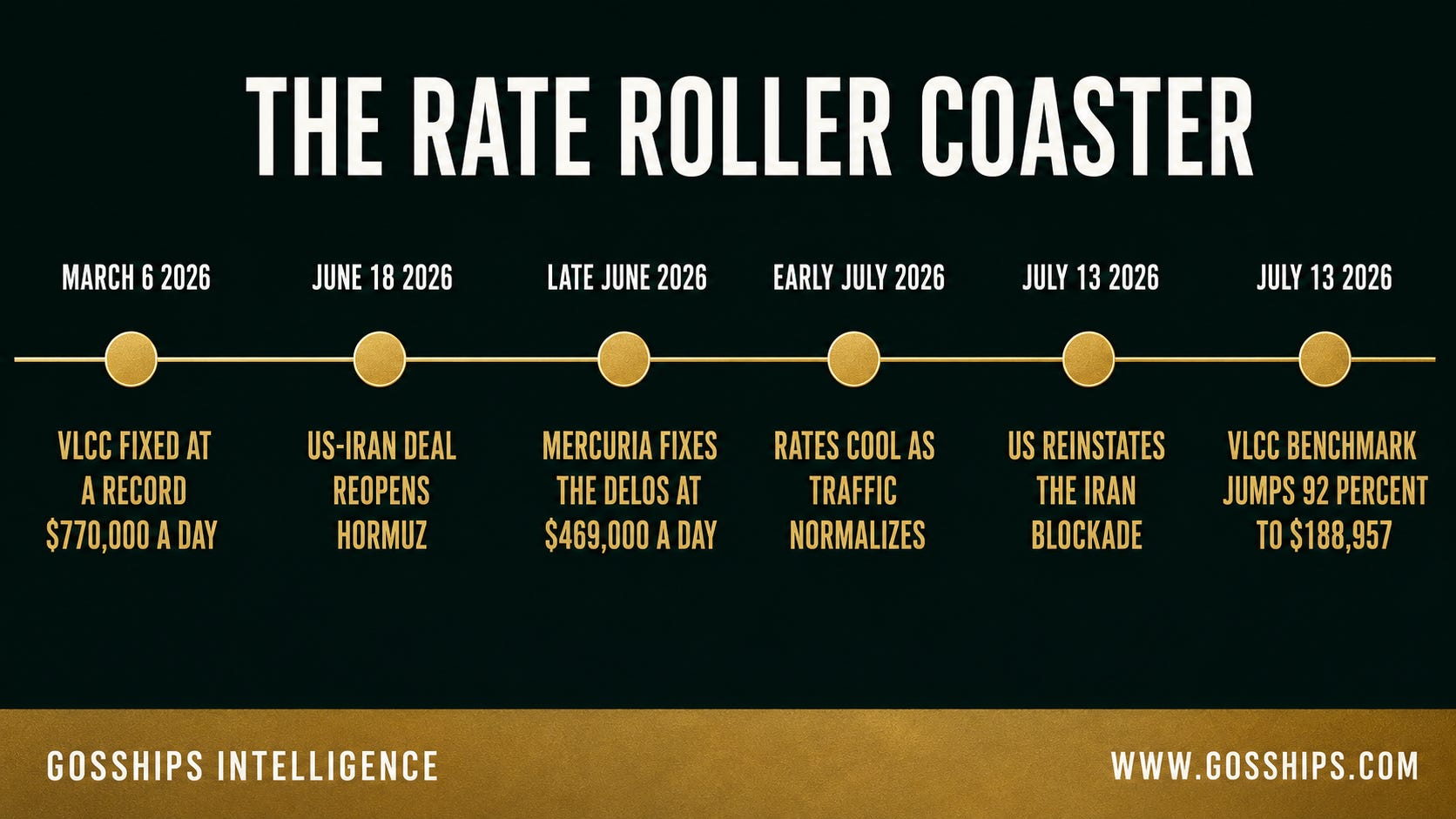

→ March 6, 2026: A VLCC is fixed at a record $770,000 a day as the first Hormuz shock hits

→ June 18, 2026: A US-Iran deal reopens the strait and rates briefly surge

→ Late June 2026: Mercuria fixes the VLCC Delos at $469,000 a day, the reopening peak

→ Early July 2026: Rates cool toward $115,000 to $145,000 a day as traffic normalizes

→ July 13, 2026: The US reinstates its blockade on Iran and briefly floats a 20 percent Hormuz toll, dropped a day later

→ July 13, 2026: A VLCC benchmark jumps 92 percent in a week to $188,957 a day, the highest since March

Sources: TradeWinds; Tankers International; Baltic Exchange; Lloyd’s List; Seoul Economic Daily; Kpler.

🛢️ The Story

Start with this week, because the market just did something it has done twice before this year. When the United States reimposed its blockade on Iranian shipping on July 13 and Iran declared the Strait of Hormuz closed again, crude tanker rates snapped straight back up. The Baltic Exchange’s benchmark very large crude carrier rate on the West Africa to China run jumped 92 percent in a single week to $188,957 a day, its highest level since March 10, during the first crisis. A separate composite VLCC assessment rose 11.7 percent week on week to about $137,248 a day, and the overall tanker rate index climbed 3.3 percent, according to Clarksons. Once again in 2026, a chokepoint war has turned the world’s supertankers into some of the most valuable working objects on earth, and the reason is not steel or engineering. It is nerve.

But the spike is not uniform, and the split inside it is the real intelligence. This is a crude story, not a tanker story: the money is pouring into the ships that carry crude oil and draining out of the ships that carry refined fuel. Every crude class is riding high. On July 13 the very large crude carriers that haul Gulf oil to Asia led the jump, and the mid-sized aframaxes surged 44.7 percent in a week to $60,367 a day, while the suezmaxes that lift a million barrels had held six-figure earnings around $151,000 a day through early July. The scramble for non-Gulf crude and the long way around a closed strait have lifted the whole dirty fleet.

On the clean side, the picture inverts. Product tankers that move gasoline, diesel and jet fuel have gone backwards. By early July the benchmark Medium Range rate on the US Gulf to Europe run had collapsed to roughly $8,500 a day, down 57 percent in a week and 59 percent on the year, the sharpest correction of any class, while the larger LR2 clean tankers sat near $21,900 a day. The clearest proof of the divide is that ships are physically changing sides. Because crude now pays so much more than refined fuel, 68 clean LR2 tankers have been switched to carrying crude so far in 2026, more than the 49 that converted in all of last year. When a tanker built for diesel starts hauling crude instead, that is the freight market voting with steel.

To understand how the crude side doubles in a week, you have to understand what these ships are actually selling now. A VLCC carries about two million barrels of crude. In a normal market its daily rate is a function of supply and demand, a commodity price. In this market it is a bet. When a strait can be open on Monday and blockaded on Tuesday, the owner who agrees to send a laden ship through it is not selling transport, he is selling willingness to take a risk almost no one else will take. That is why rates move in giant steps rather than smooth curves, and why the tanker owners who will sail are, by one blunt industry description, having the best weeks of the entire crisis.

This war has now produced that spectacle again and again, and the numbers from the earlier spikes explain why owners are so quick to point their ships back toward the Gulf. The first shock, in early March, was the most violent. As Iran mined the strait and major marine insurers suspended war-risk cover, a VLCC was fixed at a stunning $770,000 a day, an all-time record, according to TradeWinds. Rates cooled through the spring as the front stabilized. Then came the second act. When Washington and Tehran signed a memorandum of understanding on June 18 that briefly reopened Hormuz, importers scrambled to charter ships and grab Persian Gulf barrels while the window was open, and VLCC earnings jumped 87 percent in days to around $195,000 a day, then kept climbing.

That late-June reopening is where the names come in, because it is when the biggest trading houses in the world showed exactly what they would pay. According to the tanker pool Tankers International, Mercuria, one of the largest independent oil traders, fixed the Delos, a 2019-built VLCC owned by Greece’s Embiricos family and managed by Aeolos Management, on subjects at $469,000 a day for a voyage from the Arabian Gulf to China. TradeWinds logged the figure at $468,900. Days later, Vitol, the largest independent trader of all, fixed the Kyklades Maritime VLCC Nissos Kea at $439,000 a day for an Arabian Gulf to Far East run. These were not the market. They were the tip of it, the price of a specific thing: a ship whose owner would accept a Hormuz transit when most would not. By contrast, VLCCs willing only to load in the Gulf of Oman, outside the strait, were fetching a comparatively modest $220,000 to $230,000 a day, a gap that measured the raw price of the risk itself.

Then the deal fell apart, and the roller coaster turned again. The ceasefire collapsed on July 8. By early July, before the collapse fully hit the freight market, benchmark rates had already cooled back toward $115,000 to $145,000 a day as traffic tentatively normalized. That calm did not last. On July 13, President Trump reinstated the blockade on Iran and, on Truth Social, floated a 20 percent toll on cargo moving through the Strait of Hormuz, declaring the United States “THE GUARDIAN OF THE HORMUZ STRAIT” and demanding reimbursement for “providing safety and security to this very volatile section of the World.” The toll drew immediate opposition, including from the IMO, and Trump abandoned it within a day, saying he would replace the fee with trade and investment deals from the Gulf states. The blockade stayed. On July 14 it took effect and the war reached the shipping lanes directly: after a third consecutive night of US strikes on Iran’s coast, Iran’s Revolutionary Guard struck two Emirati supertankers transiting Hormuz, killing one crew member, and Brent crude spiked to a one-month high above $86 a barrel. The freight market did what it now does on cue. It spiked.

To grasp how expensive nerve has become, follow the tonnage. When Iran first closed the strait on February 28, the fleet did what fleets do in a war zone: it left. By IMF PortWatch data, roughly 90 vessels a day transited Hormuz before the conflict. At the depth of the crisis that collapsed into the low double digits a day, and even after the June deal it clawed back only into the low 30s, roughly a third of the old normal. Months of repositioning pulled most VLCC capacity out of Persian Gulf circulation, so that when cargoes must move, there are few ships in the right place to move them. And the ships that remain will not sail for an ordinary number. With the blockade reimposed and Hormuz declared closed again, transit has thinned back toward a trickle, because an owner will point a laden hull into the strait only when the voyage pays enough to make the danger worth it. That is a second engine under the rate: any barrel that has to cross must first find one of the few owners willing to go, then pay whatever it takes to move them, and the scarcer those willing owners get, the higher the clearing price climbs. Every fresh attack in the strait thins the pool again. The same disruption that cut VLCC volumes through Hormuz by an estimated 36 percent also sent rates to records, because fewer cargoes moved but each one had to outbid the fear. Voyages lengthened as ships took evasive routing, soaking up still more capacity. A market with a fraction of its usual flow and few of its usual ships prices on desperation.

It is worth being precise about what these numbers are and are not, because some of them are more theatrical than they look. The eye-watering Gulf fixtures, the Mercuria and Vitol prints, were reported on subjects, meaning provisionally, and Lloyd’s List has gone so far as to describe some Middle East Gulf rates as “imaginary,” headline numbers that move sentiment even where cargoes do not ultimately trade at them. The $188,957 benchmark is a West Africa to China assessment, a global-market proxy rather than a Hormuz fixture, and voyages actually exposed to the strait carry a further premium on top of it. None of that makes the money unreal. Mercuria and Vitol are serious counterparties, real cargoes are moving at extraordinary cost, and the owners collecting these rates are booking the profits. But the honest picture is a market where the top prints are part transaction and part signal, and where the signal alone is enough to move the price of oil.

The owners on the right side of this are the visible winners. Frontline, the VLCC giant controlled by John Fredriksen, posted a first-quarter net profit of $559.1 million, its strongest quarter by adjusted earnings since 2004, and locked in second-quarter VLCC rates around $181,700 a day, levels set before this week’s spike. Greece’s Okeanis Eco Tankers reported a record quarter and told investors the first half of 2026 could beat any full year in its history. DHT Holdings and other pure-play crude owners rode the same wave, and the Embiricos family, whose Delos commanded Mercuria’s $469,000, is exactly the kind of owner this war rewards. When crude rates jump 92 percent in a week, the owners holding tonnage near the Gulf are the ones who cash the check, while the clean-tanker owners left carrying diesel watch their rates fall.

Now the part that turns a chartering-desk story into something every driver should care about. Freight does not stay at sea. It is embedded in the delivered price of crude, which becomes the input price of gasoline, diesel and jet fuel. When benchmark crude tanker rates double in a week and Hormuz-exposed fixtures run into the hundreds of thousands of dollars a day, the freight bill on a single two-million-barrel cargo can swing by many millions, several dollars a barrel of pure transport cost layered on top of a crude price already inflated by the war. It never appears on a pump as a line item labeled “supertanker.” It appears as the extra few cents to a dollar a gallon that no one can quite explain. So the answer to who pays as Hormuz sends rates soaring is the same as it always is: the owner is paid first, the trader pays him, and you pay last. Who keeps winning if the blockade holds, who gets crushed when it lifts, and why the real money is in the timing rather than the rate, is below.