Why Did Suez Just Tax Oil Tankers Hardest?

From today the Suez Canal charges laden crude and product tankers a 37 percent surcharge, up from 25, on a supertanker transit that runs about $800,000.

⚓ The Gosships Team

Gosships Intelligence Is Published At Gosships.com

For Sponsorship And Partnership Inquiries Contact intelligence@gosships.com

|⚓ About Us | 🛢️ Exclusive Report | 📋 SwiftAction Training |

🏅Black Gold Membership (*53 Slots Left)

The Suez Canal Authority just made oil the most expensive cargo you can float through Egypt.

From today, July 15, 2026, a laden crude or product tanker pays a 37 percent surcharge on its canal dues, up from 25 percent, and that is the steepest levy placed on any class of ship in the convoy. A very large crude carrier transit that already runs about $800,000 all in now carries the heaviest markup on the water, heavier than the container ships Egypt has spent a year coaxing back through the Red Sea. The authority calls the increase temporary. It lands at the precise moment Maersk and Hapag-Lloyd are edging their services back through Bab-el-Mandeb after more than two years of sailing the long way around Africa. Cairo lost more than $6 billion in canal revenue when the ships left. Now it is raising the price of their return. The message to the tanker market is blunt: pay up, or keep taking the Cape.

📋 In This Issue:

🛢️ The Story

📊 By The Numbers

🔍 Why It Matters

👀 What To Watch

🚨 Gosships Signal

🔔 Not Subscribed? Gosships Intelligence Delivers Oil Shipping Intelligence. Subscribe Here!

📊 Order Our Exclusive Report

→ Global Tanker Market Outlook Q3 2026 Edition

📋 Competency-Based Maritime Training

→ SwiftAction

Related Coverage

📌 Gosships Data Card

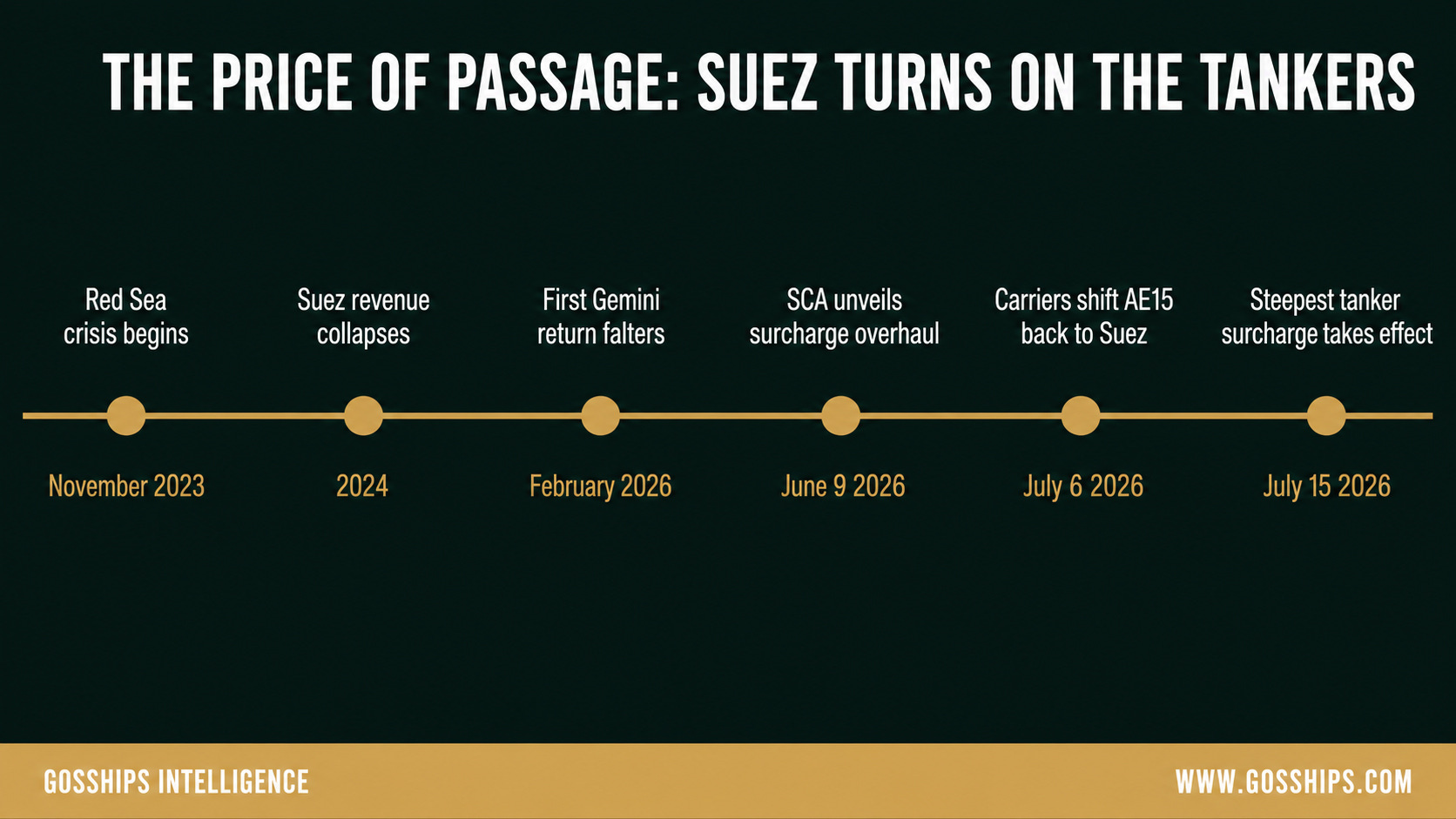

→ November 2023: Houthi forces seize the Galaxy Leader off Yemen, opening the Red Sea crisis that pushes most liner and tanker traffic onto the Cape of Good Hope route.

→ 2024: Suez Canal revenue falls to about $4 billion from a record $10.3 billion in 2023, with only 13,213 ships transiting, roughly half the prior year, per the Suez Canal Authority.

→ February 2026: Maersk and Hapag-Lloyd return the Gemini Cooperation’s ME11 service via Suez, then divert back around the Cape within weeks, per gCaptain.

→ June 9, 2026: The Suez Canal Authority issues navigation circulars for its first broad surcharge overhaul in about three years, effective July 15, per Splash247 and The Maritime Executive.

→ July 6, 2026: Maersk and Hapag-Lloyd announce their AE15 service will shift from the Cape back to the Suez Canal, deepening a cautious return, per gCaptain.

→ July 15, 2026: Laden crude and product tankers begin paying a 37 percent surcharge, up from 25 percent, the steepest levy of any vessel class, per the Suez Canal Authority.

Sources: Suez Canal Authority; Splash247; The Maritime Executive; IndexBox; gCaptain; Ahram Online.

🛢️ The Story

The Suez Canal Authority (SCA) has posted its first wide ranging rate increase in about three years, and it has aimed the heaviest blow squarely at oil. Under a series of navigation circulars first reported by Splash247 and The Maritime Executive on June 9, the Egyptian waterway operator is raising the temporary surcharges it applies on top of standard transit dues for nearly every category of ship. The new regime takes effect for vessels commencing transit on or after July 15, 2026. Passenger ships are the only class exempt from any surcharge at all.

The steepest increase falls on tankers. According to Splash247, IndexBox and The Maritime Executive, laden crude oil carriers and petroleum product tankers now pay a 37 percent surcharge on their normal canal dues, up from 25 percent. Tankers travelling in ballast see their surcharge rise from 15 percent to 27 percent. No other class carries a rate as high as the laden tanker figure. LPG carriers and chemical tankers move to 32 percent from 20 percent. LNG carriers jump to 19 percent from 7 percent. Dry bulk carriers more than double, to 22 percent from 10 percent. General cargo, heavy lift, roll on roll off and similar categories climb to 26 percent from 14 percent, while vehicle carriers pay 26 percent northbound and 12 percent southbound. Container ships, the class Egypt most wants back, face a 12 percent surcharge, and the SCA said the existing tier based surcharge structure for container vessels stays unchanged. In plain terms, most classes went up by roughly twelve percentage points, a framing Lloyd’s List captured in its own headline, but crude and product tankers were left standing at the top of the table with the single highest rate on the water.

It is important to be precise about what this is, because the number will be misread. This is a surcharge on base canal dues, not a flat fee and not a tax on the full cost of a transit. The SCA levies its base toll on a vessel’s Suez Canal Net Tonnage, published in Special Drawing Rights, and that underlying tariff has not been revised since 2024. On top of that base toll sits the temporary surcharge, and it is that surcharge, the percentage, that just moved from 25 to 37 for a laden tanker. The authority described the increase as based on its assessment of maritime market conditions, and said the fees could be amended or cancelled depending on future developments. The word the SCA keeps using is “temporary.” Owners have heard that word before.

So what does it cost. Here the honest answer is a range, not a single clean figure. A laden VLCC transit of the Suez Canal runs roughly $800,000 all in, a figure consistent with April 2026 industry reporting and with the published toll calculators operated by Leth Agencies and Wilhelmsen, whose estimates for a fully loaded supertanker span roughly $400,000 to $900,000 depending on tonnage, draft, direction and cargo. That all in number bundles the base transit dues together with services such as pilotage, tugs, mooring and the transit convoy. Because the 37 percent surcharge is charged only on the base dues rather than on the entire bundle, the exact dollar increment from the twelve point jump varies vessel by vessel. What is not in doubt is the direction. For a laden supertanker, the move from 25 to 37 percent adds materially to a bill that already sits near $800,000, and it does so at a moment when every competing route is being repriced. We are deliberately not inventing a single surcharge dollar here, because the number depends on each ship’s net tonnage. Any broker can run the exact figure through a Leth or Wilhelmsen calculator for a named vessel, and that is precisely the exercise chartering desks are running this week.

Who actually pays is the next question, and the answer travels down the chain. The registered owner pays the canal first. On a spot voyage, the owner prices the higher canal cost into the freight it quotes, so the charterer, an oil major, a trader or a refiner, absorbs it through the fixture. On time charter and contract of affreightment business, the cost tends to surface through bunker adjustment factors and canal cost pass through clauses, a mechanism logistics advisories including Kuehne+Nagel flagged when the circulars landed. In other words, the SCA collects from the shipowner, but the economic weight settles on whoever owns the barrels and, eventually, on the refined product at the other end.

To understand why Egypt is raising prices at all, you have to see how far the canal fell. The Red Sea crisis began on November 19, 2023, when Houthi forces seized the car carrier Galaxy Leader off Yemen, and it emptied the waterway. Suez Canal revenue collapsed to about $4 billion in 2024 from a record $10.3 billion in 2023, according to figures the Suez Canal Authority reported through Ahram Online and Euronews. Only 13,213 ships transited in 2024, roughly half the more than 26,000 that passed in 2023. The International Monetary Fund, cited by Hellenic Shipping News, projected canal revenue of about $3.6 billion for fiscal year 2024 and 2025. gCaptain noted that before the attacks the canal processed roughly 80 container ships per week, and that by mid January 2026 the figure had recovered to just 26. This is a toll road that lost half its traffic and more than half its money, and it is now trying to rebuild the top line.

Here is the tension that makes this story worth your attention. The SCA is raising surcharges with one hand while, with the other, it is doing everything it can to lure ships back. The authority has run special provisions to attract container ships specifically, including incentives for vessels carrying cargo or sailing empty, and it has spent months publicly courting the liner giants. Suez Canal Authority Chairman Osama Rabie, speaking during ceremonies for CMA CGM’s newest ship as reported by The Maritime Executive, said the canal had succeeded in elevating the level of maritime services it provides as it sought to attract more vessels, and acknowledged that the region’s geopolitical challenges had imposed new realities on the maritime transport market and supply chains. Cairo trotted out the evidence: the ultra large container ship CMA CGM Vendome, at 220,553 deadweight tonnes and about 24,000 TEU, made its first southbound transit on CMA CGM's FAL 3 route since January 2026, and the French carrier logged 104 Suez transits in the first five months of 2026, moving 12.5 million tonnes. The pitch to shipping is the shorter voyage and the cost savings versus the Cape. The problem is that the same authority just made that voyage more expensive for the ships that burn the most fuel and carry the most valuable liquid cargo.

The timing collides with a genuine, fragile return by the container lines. In early February 2026, Maersk and Hapag-Lloyd brought their Gemini Cooperation ME11 service back through the Red Sea, only to divert it and other strings back around the Cape within weeks. Maersk attributed the reversal to “unforeseen constraints arising from the wider operating environment in the Red Sea region,” and framed the retreat as "temporary adjustments," per gCaptain. The carrier has argued consistently that the Trans Suez route “is the fastest, most sustainable and most efficient way for us to serve our customers.” Yet the whipsaw has a cost of its own that no toll captures. As Xeneta senior analyst Destine Ozuygur put it when CMA CGM abruptly reversed course, “Unpredictability is toxic for supply chains.” By July 2026 the mood had turned cautiously constructive again. gCaptain reported on July 6 that Maersk and Hapag-Lloyd would shift their AE15 service from the Cape back to the Suez Canal, and on July 9 that the MECL service would follow, with the Triple E class Majestic Maersk scheduled to transit around July 24. Chairman Rabie has forecast a return to normal traffic levels in the second half of 2026. Into that tentative recovery, the SCA has just dropped a price increase.

For the tanker market specifically, the surcharge lands on an already hot deck. Crude tanker spot rates hit multi-year highs in late 2025, according to the US Energy Information Administration, and then the 2026 Strait of Hormuz war drove them to outright records, with Lloyd's List reporting the Baltic VLCC index topping $420,000 a day at the peak. Even off that peak, tanker earnings remain strong enough that a higher canal surcharge is an irritant rather than a deterrent, and many laden VLCCs will simply pay and sail. But the calculus is not universal. For a marginal cargo where the Suez routing and the Cape routing are already close on total voyage economics, a twelve point increase on base dues can be the tie breaker that sends a supertanker south around Africa instead. That is the quiet risk in Cairo’s math: price the passage too aggressively, and the very diversions the canal spent two years trying to reverse become rational again.

Egypt is not alone in reaching for the toll book in 2026. Turkey raised transit fees for the Bosphorus and Dardanelles to $6.70 per net tonne from July 1, an increase of roughly 15 percent under its annual indexation, up from $5.83 last year, according to Daily Sabah, Xinhua and TASS. Two of the world’s critical chokepoints have now repriced within a fortnight of each other. For an owner routing crude from the Gulf to the Mediterranean or the Atlantic basin, the cumulative message is that the fixed geography of the oil trade is getting more expensive to cross, one waterway at a time.

None of this is a war story. There is no attack here, no closure, no missile. This is a commercial decision by a sovereign toll authority to charge more for a scarce piece of geography, and to charge oil the most of all. The question that hangs over it is whether a canal that just clawed its way partway back from a fifty percent traffic collapse can raise prices on its most fuel hungry customers without pushing a share of them back onto the Cape. What this means for VLCC economics desk by desk, which exact catalysts will tell you within weeks whether the tanker surcharge is sticking or backfiring, and how the smartest chartering and compliance teams are already repricing their Suez exposure, is below.